tmomoh

112 posts

tmomoh

@ScottArbitrage

90后/IC工程师/地理套利/德州GTO/FIRE运动 Millennial/IC Designer/Geo-arbitrage/Poker GTO/FIRE ON THE WAY

Toronto, Canada Katılım Nisan 2012

243 Takip Edilen135 Takipçiler

我比较蠢~

哪位大神能告诉我:Tao怎么优化布局,都能超越Moore’s law了?

期待哪天你能超越law of gravity

都超越了还说1.4nm干嘛?直接2031年可以用28nm流片更显得你厉害

CN Wire@Sino_Market

🇨🇳Huawei Unveils New Chip Design Approach to Challenge Global Leaders Huawei Technologies said it has developed a new chip design principle called the “Tau Scaling Law,” also referred to internally as “Her’s Law,” aimed at advancing semiconductor performance beyond the limits of Moore’s Law. Speaking at the 2026 IEEE International Symposium on Circuits and Systems in Shanghai, Huawei semiconductor chief He Tingbo said the approach could reduce signal delay and improve transistor density to sustain gains in computing power. Huawei said the first Kirin chip based fully on the new design method will be used in a flagship smartphone launching this year, and that the company could reach 1.4-nanometer chip capabilities by 2031. #CHINA #TECH #AI #HUAWEI (mktnews.com/flashDetail.ht…)

中文

And people think rates sold off because we are overheating.

TonyIsHere4You@TonyIsHere4You

This chart didn't get enough attention today - it shows that foreign holdings of US treasuries are being used in place of oil reserves and being drained as such.

English

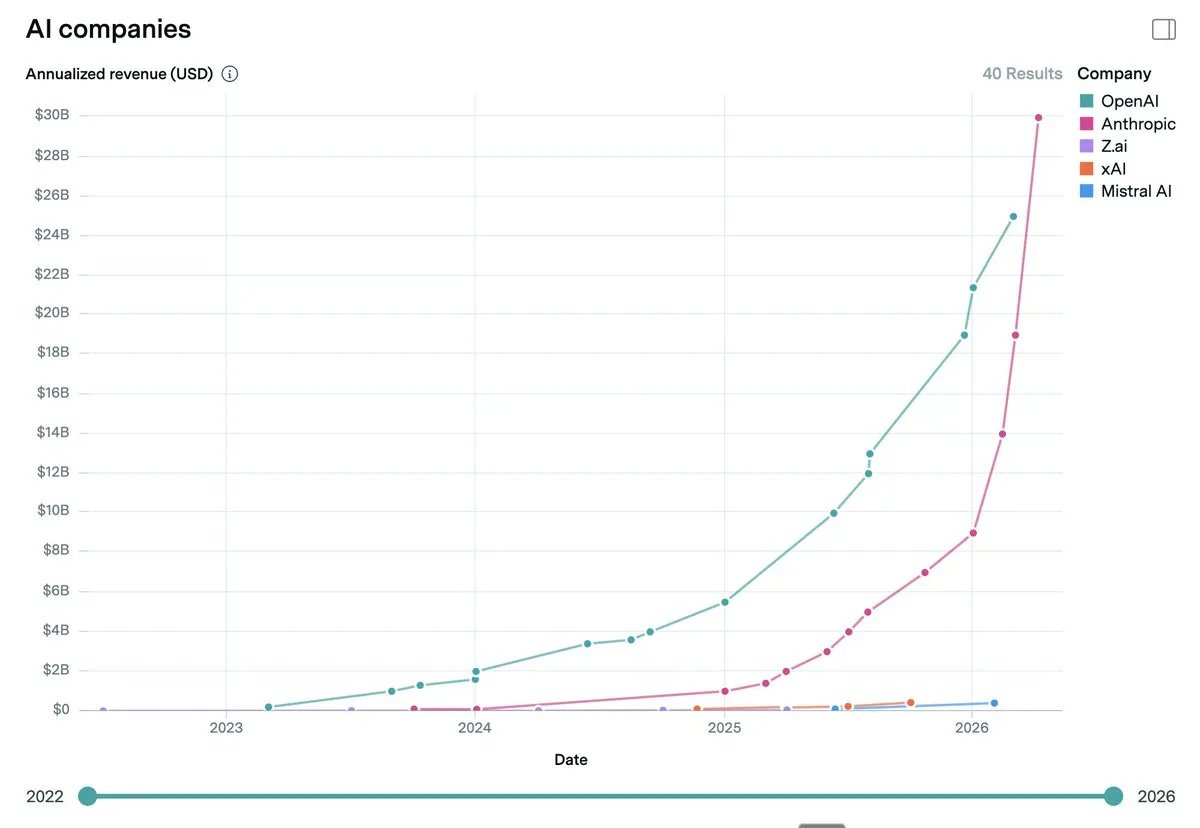

@neha041187 @FirstSquawk Why you are comparing anthropic’s 2Q data with OpenAI’s 1Q data?🤔

English

@FirstSquawk OpenAI still leading Q1 actuals by $1B ($5.7B vs $4.8B), but Anthropic’s run-rate has already blown past them (~$45B vs ~$25B) with insane momentum. Coding/enterprise use cases winning hard. Who wins 2026? Race is on 🔥

English

OPENAI PULLED IN $5.7 BILLION IN Q1 REVENUE, OUTPACING RIVAL ANTHROPIC BY $1 BILLION, PER THE INFORMATION.

English

@ShanghaoJin @jasonnotes0206 @AmberMo79750559 @RYANHINGSHING BIOSECURE的影响怎么量化呢?

毕竟收入7成多靠美国业务,这块没了公司就GG了。

中文

基础模型中国至少落后一代,但医疗方面真不好说鹿死谁手

中国在医疗系统化数据、管理运营上优势太大了。而且降低社会成本的东西,“他们”会不遗余力

Herman Jin@ShanghaoJin

美国顶尖医疗机构的研发确实非常厉害,但是中国正用其效率以惊人的速度追赶 而且因为中国有巨多实操案例,加上三甲医院系统化数据、整体管理优势。几年内,不管新药研发、还是治疗整体能力,中国一线医院都会让你们惊掉下巴 好像是2000年TSMC,良率是一片一片搓出来的

中文

@ShanghaoJin @dmjk001 别人一片它两片,功耗还得大一倍,散热再多一倍,封装还要降低良率,体积也大两倍,续航还少一倍,电池看来要大一倍,手机重量还得大一倍,故障率也得上升一倍。

中文

@dmjk001 邪修好牛逼啊,真有人会去帮任我行洗底裤

要不说下3nm流出来要多久,良率多少,敢用这种片的手机准备卖多少钱?3万?

3万都不够你回本的,不过是多点费片呗?

中文

$GOOGL 持有 Anthropic 14% 的股份、SpaceX 约 7% 的股份,以及 Waymo 100% 的所有权,你居然想在这些公司 IPO 之前卖掉?😂

都怕高,高处不胜寒

Evan | Investments@NotA_Bull

I don’t understand why people are trimming $GOOGL. They own 14% of Anthropic, 7% of SpaceX, and 100% of Waymo and you want to sell before the IPOs? Why?

中文

tmomoh retweetledi

As two of the largest forces in equity markets -- growing index ownership and increasing amounts of capital controlled by extremely short-term-oriented, leveraged, volatility-intolerant investors -- converge, we have found occasional opportunities to acquire some of the most dominant long-term compounding franchises at attractive valuations.

For example, we acquired Alphabet $GOOG when the stock declined substantially on the release of ChatGPT in late 2022, Amazon $AMZN in the weeks following Liberation Day, and $META more recently on the market's response to the company's unexpectedly large cap ex guidance and expenditures.

In our 13F which we will file later today, we will disclose a new position in Microsoft, a company we have followed for many years now offered at a highly compelling valuation. While $PSUS will not be filing a 13F tomorrow, it has also recently made $MFST a core holding.

Microsoft operates two of the most valuable franchises in enterprise technology, which account for approximately 70% of the company's overall profits: M365 and Azure.

M365, the company's productivity suite, is the dominant operating platform for knowledge work, with over 450 million workers using Word, Excel, PowerPoint, Outlook, and Teams on a daily basis.

Azure is the world's second-largest hyperscaler cloud platform and, like AWS in our Amazon investment, is a direct beneficiary of the multi-decade migration of enterprise IT workloads to the cloud, which is now further accelerated by surging demand for AI inference workloads.

Both M365 and Azure are underpinned by Microsoft's unparalleled enterprise distribution and the security, compliance, and identity infrastructure it has built and refined over decades.

Beyond these core franchises, Microsoft also owns a portfolio of other leading businesses, including LinkedIn (the world's largest professional network with 1.3 billion members), its gaming platform (Xbox and Activision Blizzard), and search and news advertising (Bing and the Edge browser).

We began building our position in MSFT in February following a meaningful share price decline after the company reported its fiscal Q2 2026 results. We were able to establish our position at a valuation of 21 times forward earnings, broadly in line with the market multiple and well below Microsoft's trading average over the last few years.

Notably, MSFT's headline multiple does not reflect the value of Microsoft's approximately 27% economic interest in OpenAI, which would represent approximately $200 billion, or 7% of Microsoft's market capitalization, at OpenAI's most recent funding round valuation.

We believe Microsoft's recent share price decline has been principally driven by investor concerns around two key issues: i) the competitive positioning of M365 against increasingly capable AI lab offerings (notably Anthropic's Claude Cowork), and ii) the durability of Azure's growth, especially in light of Microsoft's evolving relationship with OpenAI.

In our view, investors underestimate the resilience of the M365 franchise given its deeply embedded role across enterprises and highly attractive price-value proposition. Unlike point software solutions, which may be vulnerable to disintermediation by better-performing AI alternatives, M365 is tightly integrated into the daily workflow of nearly every large enterprise and is supported by Microsoft's identity, security, compliance, and data governance infrastructure, which would be nearly impossible to replicate.

Attractive bundle economics further reinforce Microsoft's advantage, with monthly average revenue per user on the M365 suite at approximately $20, less than half of what customers would pay to purchase the underlying applications individually from different vendors.

Moreover, we are encouraged to see Microsoft prioritizing its R&D efforts and investment in Copilot, its own AI agent embedded across M365, with direct involvement from CEO Satya Nadella. We believe these efforts will translate into improved product velocity and greater customer adoption over time.

Alongside Copilot's rollout, the company has also begun shifting its pricing model from pure per-seat licensing to a hybrid model of seats plus metered consumption, which helps expand the company’s revenue opportunity as AI agents drive incremental usage that a seat-only structure would not capture. These initiatives should help sustain M365’s strong underlying growth momentum, which was already evident in the business unit’s 15% revenue growth (in constant currency) last quarter.

We believe concerns regarding Azure's growth trajectory are similarly misplaced, particularly in light of the franchise's exceptional recent performance. Azure revenue grew 39% in constant currency last quarter, with company guiding to modest acceleration through the second half of the year.

We view Microsoft's recent decision to restructure its OpenAI partnership not as a concession but as part of a deliberate pivot toward a more open, multi-model architecture that better serves enterprise customers, who increasingly seek optionality across model providers.

Microsoft recently disclosed that over 10,000 enterprise customers have used more than one model on Azure Foundry, the company’s modular AI model marketplace. This model-agnostic approach also strengthens Copilot, which can auto-route queries across multiple models to deliver the optimal output for a given task.

To support Azure's rapid growth amid persistent supply constraints, Microsoft has raised its calendar year 2026 capex budget to approximately $190 billion. Consistent with what we have observed at hyperscaler peers Amazon and Google, we view this spend as growth capex that should drive future revenue generation. This is particularly true for Microsoft, given that roughly two-thirds of its capex budget is allocated to server and networking equipment that correlates directly with near-term revenue.

Like our purchases of $GOOG, $AMZN, and $META, we believe that $MSFT offers analogous and compelling long-term value at today's valuation.

English

@168X_Fortune 没懂这个intc的pb为2是怎么算的,看数据目前也在5以上了。 而且每年capEx投入要增加book value的话,不是借钱就是增发,还得roic比wacc高才行。

中文

@iamtrebuh @kimmonismus Sam Altman, I don’t like him. Something about him just seems very disingenuous.

English

According to recent estimates, Anthropic has already reached $44 billion in ARR, significantly surpassing OpenAI.

It's no secret: the big money is in the enterprise sector.

That explains Sam's post and OpenAI's two-month free codex access for businesses.

Sam Altman@sama

codex is the best AI coding product and we want to make it easy to try. for the next 30 days, we are giving companies that want to try switching over two months of free codex usage.

English

tmomoh retweetledi

Today we’re launching the OpenAI Deployment Company to help businesses build and deploy AI.

It's majority-owned and controlled by OpenAI. It brings together 19 leading investment firms, consultancies, and system integrators to help organizations deploy frontier AI to production for business impact. openai.com/index/openai-l…

English

tmomoh retweetledi

Gerstner seemingly implies that OpenAI is at $35B of ARR, as the as FT and Semi-Analysis have both pinned Anthropic at $45B.

So in the first 4 months of 2026, OpenAI has added ~$4B of ARR a month (as they ended 2025 at $20B) and likely accelerated in recent weeks with 5.5 and Codex momentum.

English

What the SpaceX–Anthropic Deal Means

Two weeks ago, we published a note laying out what GPT-5.5's release implied. The conclusion was simple: whoever secures compute first, in greater volume, and with greater reliability ultimately takes the win. With OpenAI's 30GW roadmap dwarfing Anthropic's 7–8GW, we closed by arguing that the structural advantage on compute sat with OpenAI.

Less than a fortnight later, that conclusion is being tested. On May 6, Anthropic signed a single-tenant lease for the entirety of Colossus 1 with SpaceXAI — the infrastructure subsidiary that consolidates Elon Musk's xAI and SpaceX. The asset carries more than 220,000 GPUs and 300MW of power, and crucially, is scheduled to come online within this month. It served as the capstone of Anthropic's April blitz, which added 13.8GW of cumulative capacity over the span of a single month. On headline numbers alone, OpenAI took more than a year to stack 18GW; Anthropic has put 13.8GW in the ground in thirty days. The takeaways break down into three.

First, the compute pecking order has been redrawn again. Anthropic has now swept up the AWS expansion (5GW, with $100B+ in spend commitments over a decade), Google + Broadcom (3.5GW of TPU), Google Cloud (5GW alongside a $40B investment), and now SpaceXAI's Colossus 1 (0.3GW). Cumulative committed capacity, inclusive of pre-April allocations, sits at 14.8GW. This is still only half of OpenAI's 2030 target of 30GW, but the fact that the SpaceX lease will be live inside a month makes "deliverability" a qualitatively different proposition.

Second, Elon Musk is the plaintiff in an active lawsuit against OpenAI — and at the same time, the supplier handing 220,000+ GPUs and 300MW of power, in one block, to OpenAI's most formidable competitor. The timing matters: the deal was struck in the middle of the Musk–Altman trial. We read this as a deliberate pincer with OpenAI in the middle. In the courtroom, Musk works to dismantle the moral legitimacy of OpenAI's leadership; in the market, he arms Anthropic to absorb OpenAI's revenue and user base.

Third, the structure is financial-engineering perfection — a clean win-win for both sides. xAI can recognize $6B of annual revenue from a single contract, an amount that almost precisely offsets its Q1 2026 annualized net loss of $6B. It also accelerates the cleanup of SpaceXAI's pre-IPO balance sheet, with the entity now being floated at around $1.75T. Anthropic, on the other side, converts roughly $5B of spend into what it expects to be $15B of ARR via the coming inference-revenue surge.

(Mirae Asset Securities, May 8, 2026)

English

@silverfang88 不需要反驳,因为现有知识投喂差不多了,很快会进入能力短暂瓶颈期,等待前沿理论知识沉淀

加上国模能力迅速覆盖95%人类的应用上限

今年下半年打价格战是一定发生的,谁也跑不了

超过一定阈值,为5%能力付几十倍费用已经不成立了

中文

刚刚,一位博主对最近很火的“估算GPT-5.5和Opus-4.7参数量”的帖子提出了数值方面的质疑,该博主的结论为:

GPT-5.5 ~1.5T, Opus-4.7 ~ 1.1T。值得注意的是该博主对“不可压缩探针”方法是认可的,仅修正了数值。

个人看法:即使数值下修,GPT-5.5参数量仍然远大于Opus的参数量。在此基础上,OpenAI仍然能稳定服务几乎所有C端用户。个人觉得Anthropic预留给普通C端用户(非Mythos模型)的算力远小于OpenAI预留给GPT-5.5的算力。

此外,我个人觉得OpenAI极有可能在“推理Infra”和“与Cerebras的合作”上有了显著的突破,从而实现高效复用KV Cache与算力资源,达到快速且稳定的服务质量。

Lawrence Chan@justanotherlaw

A recent viral paper claims to reverse-engineer the parameter counts of frontier models: GPT-5.5 = 9.7T, Opus 4.7 = 4.0T, o1 = 3.5T, etc. @ben_sturgeon and I investigated and found serious issues in the paper; fixing them gives GPT-5.5 as ~1.5T (90% CI: 256B-8.3T).

中文