Sabitlenmiş Tweet

1/ Introducing the Crypto Banking System, a roadmap to bring DeFi to be a challenger to TradFi

cryptobanking.network/the-crypto-ban…

English

SebVentures

5.3K posts

@SebVentures

interest rate scholar Founding Chef at @SteakhouseFi Too boring for #DeFi, too punk for #TradFi

new plumbing notes just dropped a schizo primer on "equity repo" conks.plumbing/p/plumbing-not…

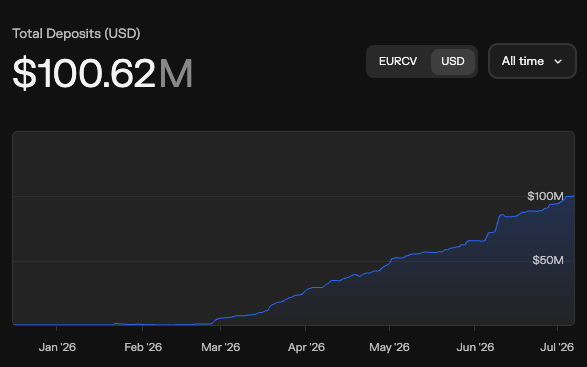

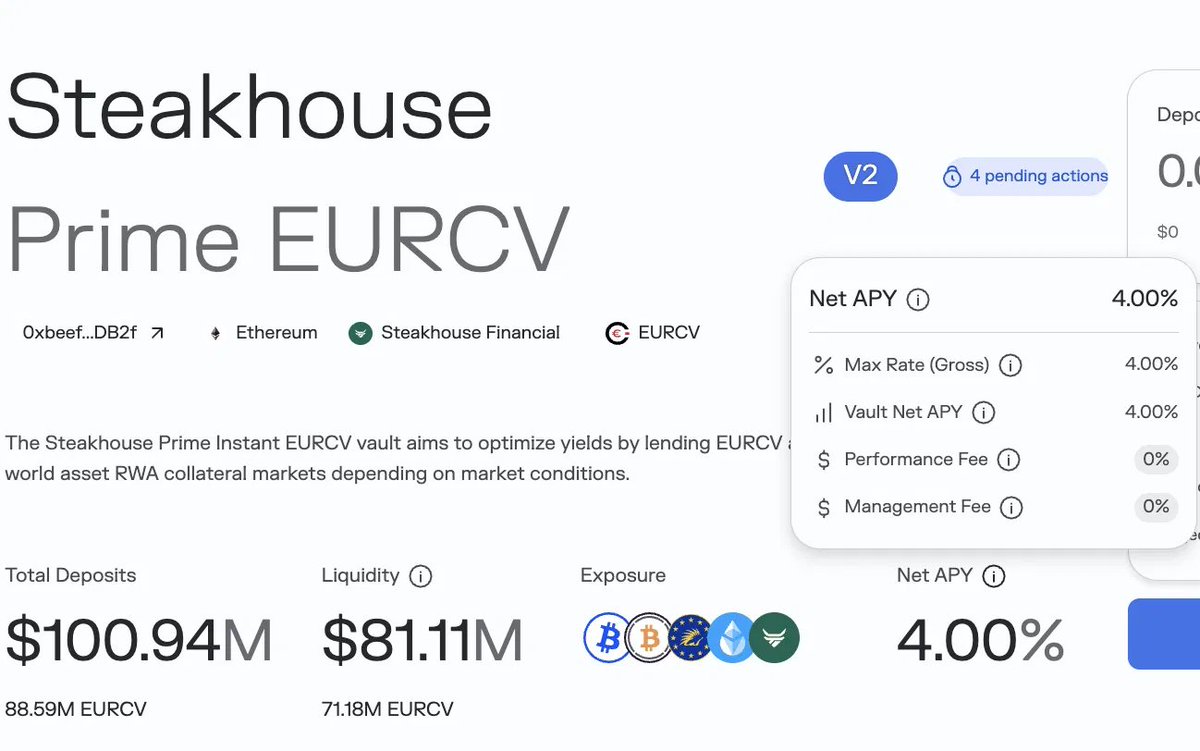

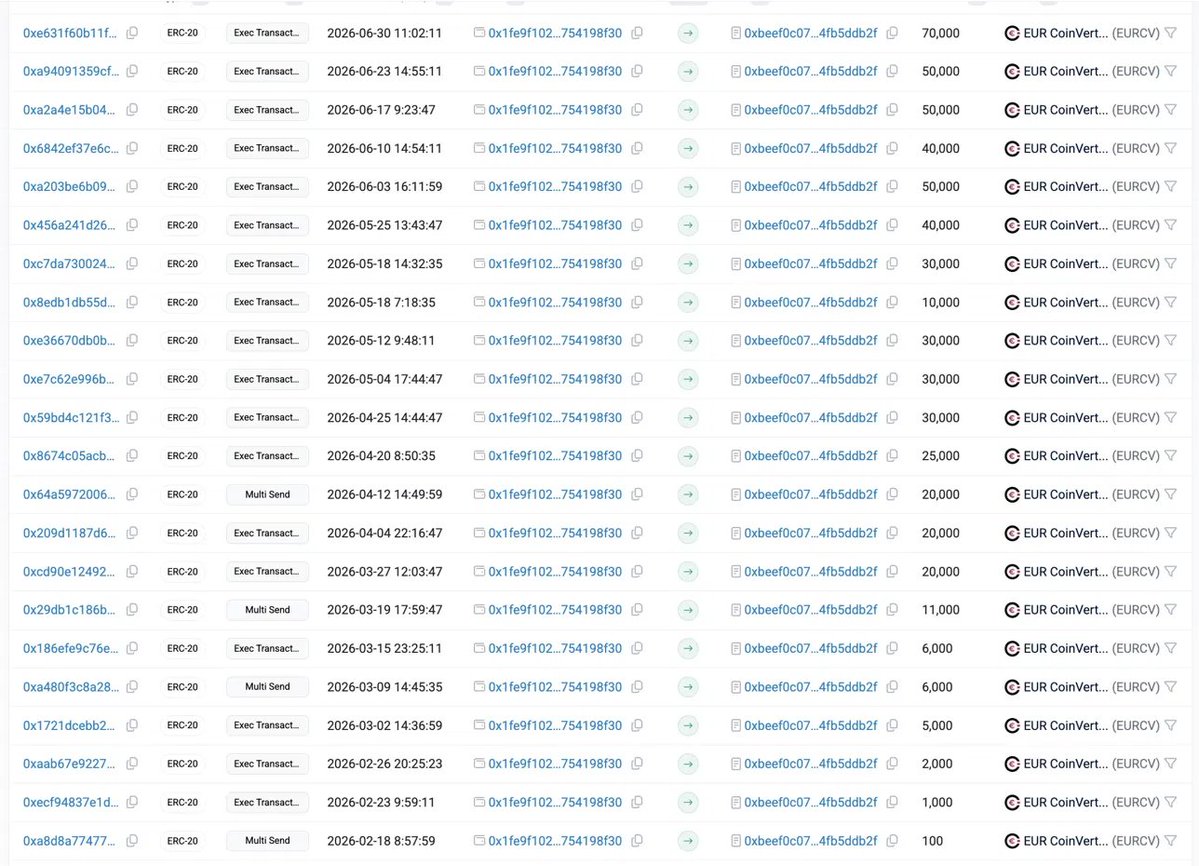

The @SteakhouseFi EURCV vault is crossing $100M . Borrow rate is consistently at 1.5% due to the supply/demand imbalance.

. @RobinhoodApp Earn product crossed 1000 users.

Because the buckets separate risk, whereas isolation separates liquidity and you only wanted the first one. The non-borrowable flag already gets you everything isolation gets you on the risk side: pledged collateral can't be lent out, borrowable float is bounded by opt-in supply. In addition, you have the flexibility to manage the parameterization around this rather than just 0 or 1, which is more akin to the tools a PB needs to manage risk.

Isolated lending markets are poorly suited for tokenized stocks and securities lending. The problem is that you want the stock itself to function as borrowable collateral, without needing to spin up multiple separate markets just to support both margin lending and stock borrow use cases.