shady_sci

184 posts

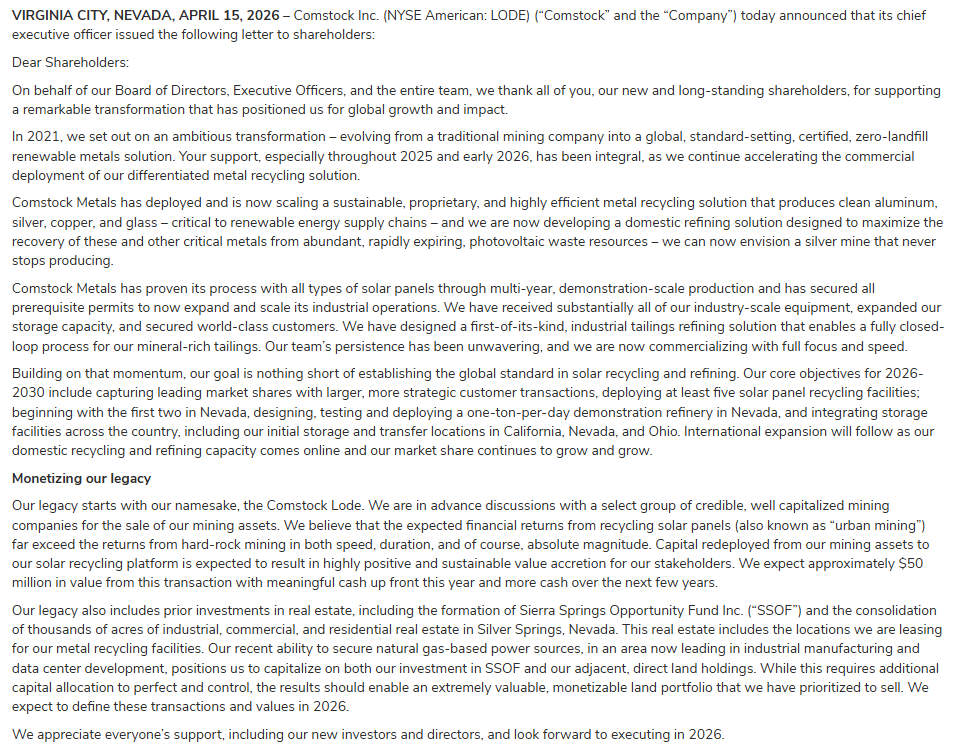

$lode new shareholder letter. Nothing new about Metals. No mention on Bioleum. The most notable parts are about monetisation.

Advanced discussion with well-capitalised mining companies about selling the mining asset for apprx $50 million with significant cash upfront in 2026. Which would all be deployed to metals.

SSOF+other real estate monetisation is signalled to take a bit longer, but to be a much higher amount. As the CEO said in the last call about SSOF, they are targetting +50% ownership in something worth hundreds of millions.

"While this requires additional capital allocation to perfect and control, the results should enable an extremely valuable, monetizable land pothey willrtfolio that we have prioritized to sell. We expect to define these transactions and values in 2026."

While the massivelly increased monetisation amount expectation is exciting. Questions that remain are how much additional cash they will spend on this, and how much longer it will take to make the transaction happen that few months ago was signalled to be taking place in february.

Still, I didn't expect anything above 8 figures from SSOF monetisation when I first invested, so if they can get 9 figures from it, I don't mind waiting for it longer.

English

@AlmostMongolian SSOF, Mining, Refining. All are plausible risk buffers and/or multipliers on the Metals thesis. All are capital drags for now, with unclear timelines.

Ultimately, still nothing matters except for panel supply.

English

@AlmostMongolian 1t fines/day refiner demo. Assuming 75% uptime (its a demo...), thats 273 t fines/year.

Fines are ~12.5% of panels.

Each 100kta recycler at ~75% outputs 9k t fines/year.

So the demo will refine max ~3% of a single recycler.

Expect refining to be a drag for awhile.

English

@AlmostMongolian Mining: We expect cash up front this year.

SSOF: We expect to define the transcations and values in 2026.

Important wording distinction. SSOF may not sell this year. Compare that to last year's wording around land sale being more imminent than mining.

English

@SneakyFrenchSpy @DonDurrett @SOLASTRO3 @CDe_Gasperis Don, see if you can get a clear answer from them as to how much silver THEY extract per panel. Not the theoretical amount that exists in them. They'd previously alluded to doing bench testing of extraction too. They should be able to give yield estimates.

English

@DonDurrett @SOLASTRO3 It's all in the article Don. They are recycling silver from solar panels. They are cornering the market in the Southwest US. $LODE @CDe_Gasperis finance.yahoo.com/sectors/energy…

English

$LODE Comstock says it has undergone an “almost complete transformation” from legacy gold and silver mining into “urban mining”, focusing on recycling end‑of‑life solar panels to recover silver, silicon, aluminum, glass and other critical minerals.

finance.yahoo.com/sectors/energy…

English

@outsanest @planert41 I contest that they know a minimum number of panels they'll get this year. They've been open (to my listening) that they don't know. They've set a goal to be profitable (at an annualised runrate), which they've told us is around 20-25-30 kt depending on silver $.

English

@ShadySci @planert41 I meant they know the minimum number. Which the CEO conveyed several times.

What they don't is maximum amount since many customers won't discuss the numbers until they see the plant working as supposed.

So I think the numbers Corrado provided are doable.

English

@whirlybard @claudedwalker Deleting def the right thing to do. All g!

English

@claudedwalker @ShadySci I *hate* deleting tweets - I want to own my mistakes.

But I know folks will see and RT my original gaff, but not the corrective reply, so best to remove it, especially since it was very young.

English

@whirlybard Are you sure this is contemporary?

Wendy's post from years ago links to this.

linkedin.com/posts/hexas-bi…

English

@outsanest @planert41 They're literally said panel supply is the thing they have least visibility over.

They can't promise. I'm bullish but be critical

English

@ShadySci @planert41 The plant will be profitable at 25% capacity. Which they promise to reach in Q4.

I would think they know pretty well how many panels they will be getting.

And they have enough cash to open several more aggregation sites in addition to those in CA and OH.

English

@planert41 If this happens (<20kt panels/year), they'll dilute to stay afloat in hope of the panels thesis playing out in 2028+. SP will tank.

SSOF and Mining sales derisk this outcome massively.

English

@planert41 Commissioning of (prospectively) the highest throughput recycling workflow for solar panels, which valorises aluminium and silver at very high margins. *If* he next 1-2 qtrs shows the market is ready , it'll derisk 95%+ of concerns, and will rocket for years.

English

@SultanAmeerali @george5289 You're a mining guy. In the notable absence of a PEA for the Dayton, how do you rate the mine economics , and the likelihood of a sale?

English

$LODE is an executional story now. Metals is fully funded, so we need to see progress on the ramp up. Corrado has also promised imminent sales of the mining assets and some of the land. If he can close those sales at prices above the carrying values, the cash proceeds would exceed the current market cap.

English

Recent Nevada land sales value the real estate inside $LODE at $1-billion. There’s also a large fund with an 8.1% stake.

I added to my position today.

Uzo@Uzocapital

$LODE - 2 positive signals 1) CFO small ($11.5k) inside buy 2) Note amendment true up date April => July (if stock is higher by then LODE pays less) Reminder Q2 is when management guided to: 1) mining asset sale (CFO running process) 2) metals production starting

English

@outsanest @broheim777 Hope so. It's not the only mine in existence though and doesn't have a published PEA, so it's not necessarily the case that it's on the cusp of a deal.

English

@ShadySci @broheim777 Gold and silver are now 3x since 2023.

Which means there must be real interest now from potential buyers.

English

@broheim777 Agree on paper, and agree that there's been no better time to sell mining/land. BUT he's also said sales were imminent for yearssss. Makes it hard to "read between the lines" with him. In 2023 he said he'd publish Dayton PEA. In 2025 Oct he said it was weeks away. 🦗🦗🦗

English

@whirlybard It’s not just the short paragraphs — it’s the symmetry. Uncommon in real writing, everywhere in AI.

Now people are starting to write like that too. Not a hot take — just if you’re paying attention..

English

After identifying a divergence, the trick is to predict if, how, and when that closes.

I assumed the AI/human writing style difference would resolve by AI learning to write like humans.

But sadly humans are adopting a ridiculous short single sentence paragraphs style. Ughh.

English