@DiaTSLAPLTR @akaApoligix Waiting for your post on the $Tem 1Q results and your opinion on the $400m convertible bonds. It seems like a good refinancing at 0% and a long term, but I'd like to read your thoughts.

English

Slp🦇

85 posts

$RZLV — UPDATED ANALYSIS: Q1 Revenue, SQD on Revolut, Reward Leadership Three updates dropped over past two week. Here's what each update actually means, what the numbers are really saying, and what everyone else is missing. 1. Q1 2026 REVENUE: $60M (Unaudited) The headline: $60M in 90 days exceeds the entire $46.8M audited FY2025. That's 128% of last year in one quarter. Sounds extraordinary. Now here's the math nobody is running. December 2025 MRR was $19.4M. Multiply by 3 months and you get $58.2M. Q1 came in at $60M. That means the actual sequential acceleration from December's run rate is $1.8M or 3.1%. The monthly average in Q1 was $20.0M vs $19.4M in December. The trajectory is positive but the acceleration is modest, not explosive. Now the harder math. $60M is 17% of the $360M annual guide. To hit $360M, the remaining 9 months need to deliver $300M — that's $33.3M per month, or 1.7x the current pace. Q1 annualized is $240M, not $360M. The gap is $120M. What this means: the $360M guide still requires a significant H2 ramp. This is consistent with the 2025 pattern where H2 delivered 543% above H1. But investors should understand that Q1 confirmed the floor, not the ceiling. The real test is whether Q2 and Q3 show the monthly ramp from $20M toward $33M+ Critical caveat: this is UNAUDITED management accounts. Rezolve doesn't normally report quarterly, this was a voluntary disclosure. The timing, during an active CMRC proxy fight ahead of the May 14 vote, is not a coincidence. The number needs H1 audited confirmation. Verdict: Bullish on confirmation of the revenue base. Cautious on the pace vs the $360M guide. Still need to see acceleration. 2. SQD TOKEN LIVE ON REVOLUT Context most people missed: Rezolve took a $63.3M impairment on SQD tokens in the 2025 20-F because the token price declined significantly after the Subsquid acquisition. That was the single largest non-cash charge on the P&L. Now SQD is listed on Revolut alongside existing listings on Coinbase, Binance, and Bybit. Revolut gives access to 70M+ users across 160+ countries. SQD operates 2,500+ active nodes indexing data across 200+ blockchain networks. What this actually does for the business: it's a two track play. Track 1: Token recovery. Broader distribution through Revolut's mainstream user base could support SQD token demand and potentially reduce the impairment overhang. If token price recovers, the $63.3M writedown partially reverses through the P&L. That's a hidden earnings tailwind nobody is modeling. Track 2: AWS playbook validation. Dan has been pitching Subsquid as Rezolve's "AWS moment", build the database internally, then commercialize it externally. The Revolut listing is the first visible step toward external commercialization of the SQD ecosystem. It moves the token from crypto-native audience to mainstream fintech audience. Honest assessment: the Revolut listing is distribution infrastructure for the token, not revenue infrastructure for the company. SQD remains pre-revenue as a commercial database product. The "AWS playbook" thesis is still speculative until named enterprise customers are paying for SQD database services outside of Rezolve's own internal use. Treat this as option value, meaningful if it works, immaterial if it doesn't. 3. JAMES HOUSE APPOINTED CEO OF REWARD This is the update most investors will skip. They shouldn't. Reward was the $230M all-cash acquisition that closed in February 2026. It's the single most important integration on Rezolve's plate because it bridges the entire RezolvePay stablecoin payment thesis to real-world bank and merchant distribution. Without Reward, RezolvePay is a payment rail with no on-ramp. With Reward, it plugs into NatWest, Visa, Barclays, Amazon, McDonald's, and Asda relationships reaching 10M+ active cardholders. James House was already Chief Commercial Officer at Reward before the acquisition. He brings 25+ years across Mastercard and BNP Paribas with operating experience spanning North America, Europe, Africa, and Asia. Outgoing CEO Jamie Samaha steps down May 31 with a clean handoff. Why this matters: internal promotion signals continuity, not disruption. A Mastercard veteran running the payments and loyalty arm is the right profile for a unit that needs to earn trust from banks and card networks. Integration risk on Reward is the single biggest execution variable for 2026 — and putting an operator who already knows the business in the CEO seat de-risks it meaningfully. UPDATED SCORECARD (May 2026): 1- Q1 revenue confirmed $60M — floor established, FY2025 exceeded in 90 days 2- SQD on Revolut — token distribution expanded to 70M+ mainstream users 3- Reward leadership — internal promotion, Mastercard veteran, clean transition 4- Microsoft Foundry — brainpowa live alongside OpenAI, Anthropic, Meta 5- Estee Lauder — 70 EMEA markets in production deployment 6- No equity dilution for operations — reconfirmed in Q1 release 7- Q1 is unaudited management accounts — needs H1 confirmation 8- $360M guide requires 1.7x current monthly pace — H2 ramp is essential 9- Material weaknesses in internal controls — remediation timeline still unclear 10- $102M short-term Crownpeak debt — refinancing not yet disclosed 11- CMRC proxy fight — outcome uncertain, board adopted poison pill 12-❌ SQD commercial revenue — still zero, AWS playbook unproven 13- ❌ Chairman/CEO separation — no movement THE MATH THAT MATTERS: At ~$2.85 and ~399M shares: • Market Cap: ~$1.14B • P/S on Q1 annualized ($240M): 4.7x • P/S on $360M guide: 3.2x • P/S if guide is hit + Reward contribution (~$450M combined): 2.5x For a company with 90%+ core software margins, Microsoft/Google hyperscaler distribution, 950+ enterprise clients including Estee Lauder, and a CEO who just bought 9M more shares through his personal entity — 3.2x forward revenue is either a screaming buy or a reflection of legitimate execution risk that the market hasn't resolved. Both can be true simultaneously. I'll keep reading the filings. I'll keep running the math. And I'll keep posting what I find. Still long. Eyes wide open. $RZLV

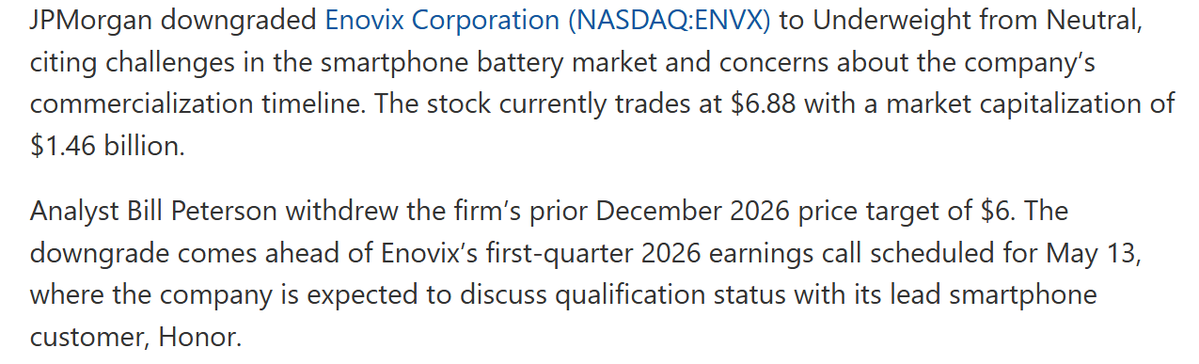

$ENVX Attached is page 1 of a Cantor analyst report regarding ENVX issued yesterday. Lead Smartphone Customer Aligns on New Silicon-Specific Qualification Framework; Co. Names New SVP of Worldwide Sales. Reit OW, $25 PT.

$ENVX They might be ready 👍