Goblin Capital

1.6K posts

Goblin Capital

@StackedGoblin

26 | Chasing alpha, stacking conviction mostly Nano, Micro, Small-Caps Personal opinions, not financial advice.

Katılım Haziran 2018

179 Takip Edilen368 Takipçiler

$KOSPI is GREEN

ARE WE BACK GUYS??

THE BOTTLENECK BROS ARE BACK!

English

Bro, Maybe just tell me the Price of these Stocks in 2035

$AAOI $MX $AXTI $SIVE $SIVEF

dilemma@actuallyimthe

Argentina just beat Spain at the 2026 World Cup final, 3-2.

English

The key may be earnings sensitivity rather than absolute market share.

A 120–170% SLC NAND price increase barely moves the needle for a company the size of $MU.

But for Winbond, Macronix and Puya, fixed legacy capacity plus long industrial and automotive qualification cycles could translate pricing directly into gross-margin expansion.

Small TAM.

Potentially massive P&L impact for the more concentrated suppliers.

The main risk is whether customers redesign products or reduce volumes once pricing becomes this extreme

English

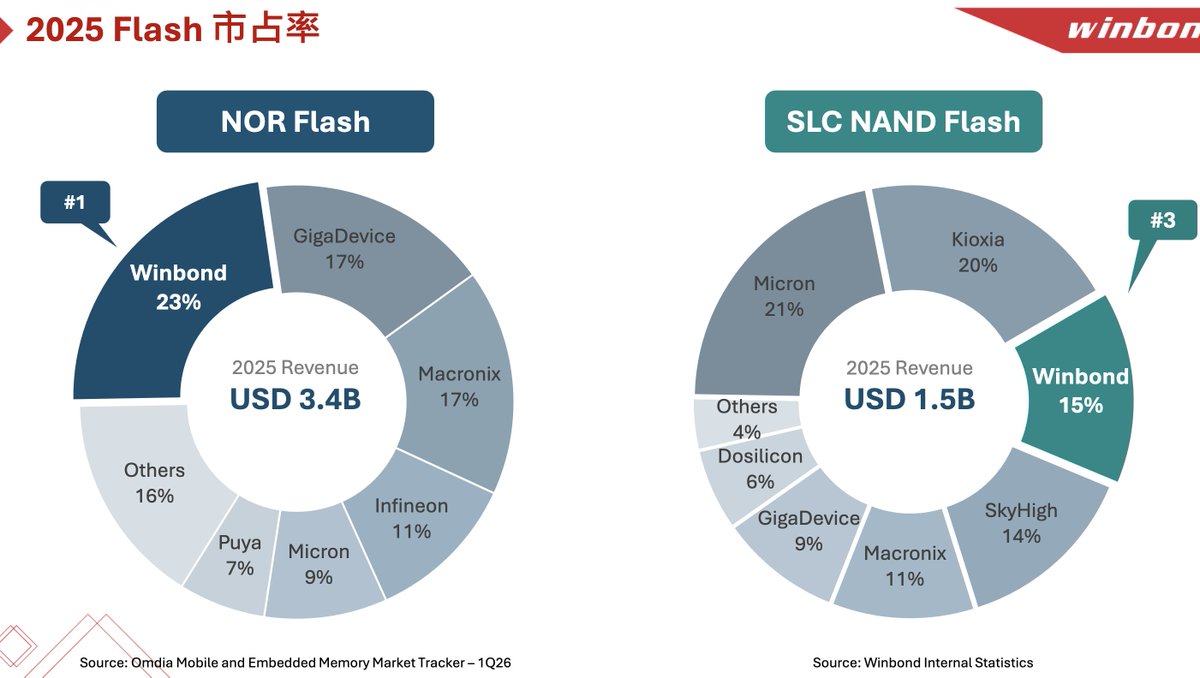

Well, looks like SLC NAND is forcasted to rise up 120-170% for H2 2026 per Trendforce.

There's $MU (21%), Kioxia (20%) as largest share, but clearer beneficiaries appears to be:

1. Winbond (2344): ~15% of the SLC NAND market

2. Macronix (2337): ~11% market share

3. SkyHigh Memory via Puya Semi: ~14% market share

Given Micron at $1T and others are a bit large relative to SLC NAND TAM.

(source: Q1 2026 Winbond presentation/Trendforce).

English

$AEHR back up +36.4% today off earnings!

2027 guide: $130-$150m (160-200% growth) from 2026 revenue. Sees opportunity to guide higher (assumes no memory revenue or little to none from newly benchmarked AI customer).

Q4 bookings: $60.7M, effective backlog is $100.6M.

- Lead AI processor wafer-level burn-in customer is significantly ramping their products.

- Engaged with additional AI processor customers who are evaluating wafer-level burn-in.

- Benchmark customer, which was a “major supplier of AI accelerators, CPUs and network processors” “exceeded their expectations.

From management: The potential revenue opportunity from one of these devices is "significant to Aehr". So another benchmark win for potential HVM in the future.

- Wafer level burn-in benchmark with a "global leader in NAND flash completed". Now evaluating a development agreement for HBM/NAND

Seems like $SNDK since there was HBF related discussions from last quarter I think.

- "Our package level burn-in business for AI processors also gained momentum over the year … from our lead hyperscale customer for Sonoma systems"

- Silicon photonics customer already ramping, newer networking customers has forecast additional systems

Basically the amount of global semi companies that map to $AEHR is pretty ridiculous across silicon photonics, memory, AI processors, and others.

I don’t quite think that $130-$150m guidance is representative of actualized revenue for 2027 if these hyperscalers/semi companies convert to HVM.

Typically with these types of qualification into HVM players, markets don’t really judge it by current quarter, but what’s to come.

And it looks very positive so far in terms of reactions...

$116 -> $60 -> $94 all in the span of a month is pretty insane volatility tho, so good to know what you're holding.

Serenity@aleabitoreddit

$AEHR looks extremely promising at ~$1.1B MC. Aehr is starting to remind me of an early $TER, mixed with pre-earnings $AAOI. If we look at the timeline and speculated customers: Feb 11th: Sonoma production win for Hyperscaler's AI ASIC processors. (likely $GOOGL, $AMZN, $META). - Probably Google? Aehr bought Incal, who was speculated to be used by Google for their TPUs. Feb 26th: $14 million from AI lead customer (likely $AMD, $NVDA) - Probably $AMD here for Instinct MI300/MI400. March 3rd: Lead silicon photonics customer for one FOX-XP system (likely $INTC siph) - Very likely $INTC has been their lead customer. March 31st: Initial order from major new silicon photonics customer (likely $AVGO, $MRVL, $CSCO ) - New customer (rules out Intel), prob one of these transitioning to 800G/1.6T silicon photonics transceivers (All speculative, very confidential BOM) Regardless. This timeline is just bottling up for $AEHR. Could be next earnings. Or two quarters from now. But feels like a matter of time before we see mass orders.

English

Same with Magnachip Semiconductor $MX.

The stock nearly broke $10 in Jun and now it feels like the market has completely forgotten about it.

But the balance sheet, valuation, product roadmap and turnaround potential are still there.

One strong earnings report or meaningful customer announcement could trigger a major re-rating very quickly. 👀

English

Classic FinX

It's always the same story here

Buy when it's at ATH and sell when it's dropping a larger amount

Let's see what they will say the next time $NBIS is at $300

The Fundamentalist@Funmentalist

$NBIS $300 - WHAT A COMPANY!!! $NBIS under $200 - WHAT A SHIT!!!

English

$AXTI earnings on July 30 could be one of the most important small-cap semiconductor reports of the month.

But expectations are already VERY high.

The market already knows:

• ~$34M of Q2 revenue was considered realizable

• Q2 should set a new InP revenue record above $17M

• InP backlog exceeded $100M

• Non-GAAP EPS guidance was $0.06–$0.08

• InP capacity is being doubled in 2026—and targeted to double again in 2027

So simply meeting guidance may not be enough.

What could create another major re-rating?

• Revenue closer to $37M–$40M

• InP revenue meaningfully above the previous record

• Gross margins moving decisively above 30%

• EPS reaching double digits

• A much stronger Q3 outlook

• Backlog continuing to grow despite higher shipments

• Faster export-permit approvals

• Long-term supply agreements, prepayments or major customer commitments

• New details on 6-inch wafers and CPO demand

The most important number may not even be Q2 revenue.

It will be how much revenue and capacity customers are already trying to secure for 2027 and beyond.

The bull case:

InP becomes one of the least replaceable materials behind the AI optical buildout and $AXTI proves demand is growing faster than capacity.

The bear case:

Results meet guidance, but the forward outlook fails to justify the expectations already priced into the stock.

A good quarter is possible.

But for another explosive move, $AXTI needs more than a beat.

It needs to prove this is a multi-year supply shortage not just one record quarter. 👀

English

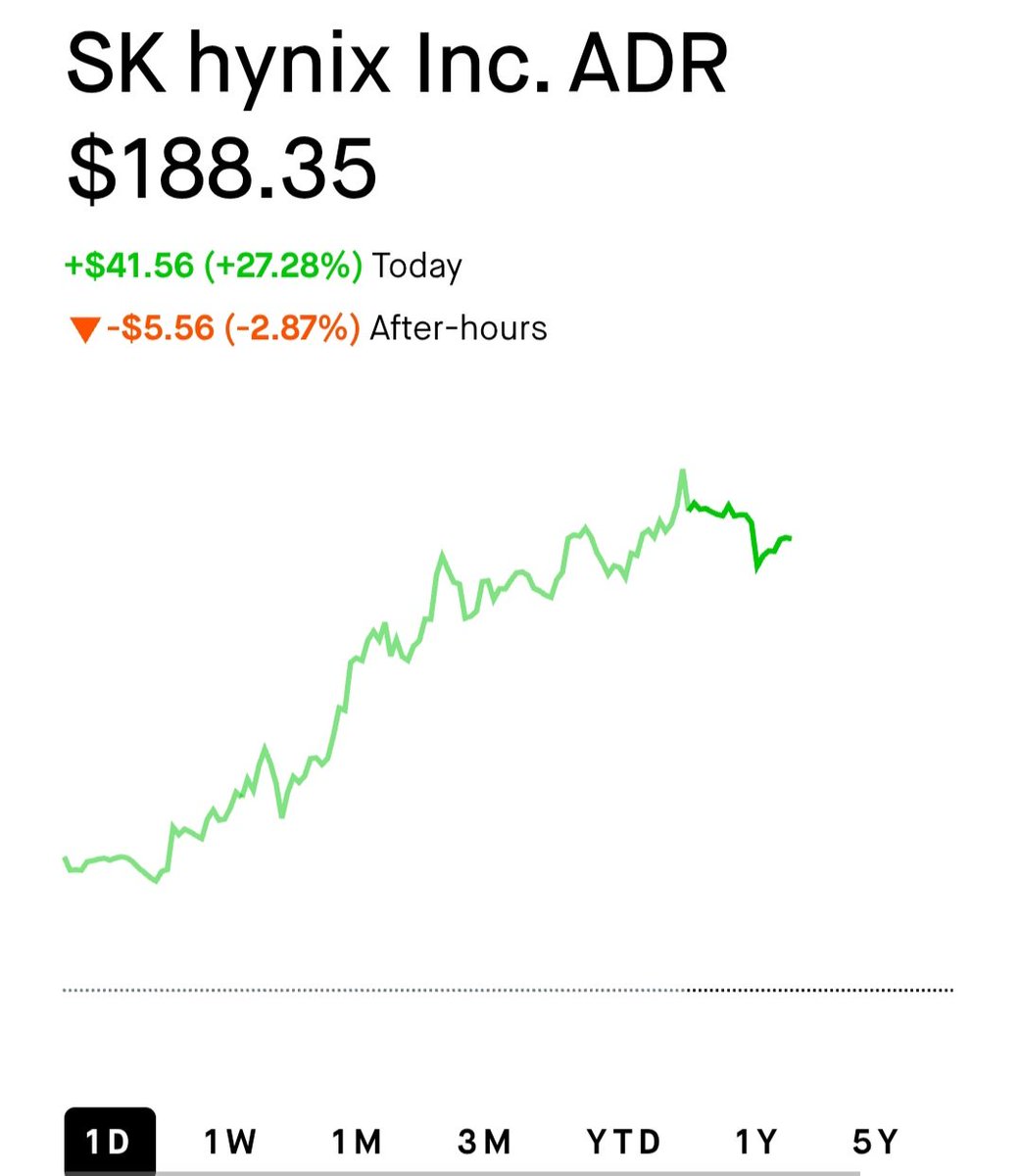

$SKHY is up roughly 27% TODAY.

That is not a typo.

But here is the crazy part:

SK Hynix gained only ~3.7% in South Korea, while its U.S. ADRs are now trading at an enormous premium to the local shares.

Today’s move appears to be driven by:

• Another bullish memory-demand signal from $IBM

• Massive U.S. demand for direct HBM exposure

• Limited ADR conversion/arbitrage

• Growing retail and ETF interest

The memory bull case is clearly getting stronger.

But a ~44% ADR premium is no longer just fundamentals.

It is scarcity, momentum and AI euphoria colliding at once.

$SKHY $MU $SNDK

HBM may be scarce.

Apparently, U.S.-listed HBM exposure is even scarcer.

English

This is exactly what COULD happen to Magnachip Semiconductor $MX if it delivers:

• A clean revenue + earnings beat

• Better-than-expected guidance

• And potentially a meaningful partnership or customer announcement 👀

Small-cap semis can re-rate VERY quickly when improving fundamentals finally meet a real catalyst.

Expectations for $MX are still low.

Now management has to prove the turnaround is real.

Q2 earnings: July 29 after the close.

Goblin Capital@StackedGoblin

$AEHR just reported one of the strongest outlooks I’ve seen from a small-cap semiconductor company: • Q4 revenue: $18.8M • Non-GAAP EPS: $0.11 • Record bookings: $60.7M • Effective backlog: $100.6M But the real shock is FY2027 guidance: Revenue: $130M–$150M That represents 160%–200% YoY growth after generating just $50M in FY2026. Aehr also expects non-GAAP net income of 18%–22% of revenue. And it gets even more interesting: A top-tier supplier of AI accelerators, CPUs and network processors completed benchmark testing of Aehr’s wafer-level burn-in solution. The results reportedly exceeded expectations. The customer now wants to move toward pilot production validation—and has already requested testing of a second device. AI processors. Silicon photonics. Silicon carbide. Potential HBM exposure. $AEHR is no longer just promising diversification. The backlog and guidance are finally proving it.

English

$AEHR just reported one of the strongest outlooks I’ve seen from a small-cap semiconductor company:

• Q4 revenue: $18.8M

• Non-GAAP EPS: $0.11

• Record bookings: $60.7M

• Effective backlog: $100.6M

But the real shock is FY2027 guidance:

Revenue: $130M–$150M

That represents 160%–200% YoY growth after generating just $50M in FY2026.

Aehr also expects non-GAAP net income of 18%–22% of revenue.

And it gets even more interesting:

A top-tier supplier of AI accelerators, CPUs and network processors completed benchmark testing of Aehr’s wafer-level burn-in solution.

The results reportedly exceeded expectations.

The customer now wants to move toward pilot production validation—and has already requested testing of a second device.

AI processors.

Silicon photonics.

Silicon carbide.

Potential HBM exposure.

$AEHR is no longer just promising diversification.

The backlog and guidance are finally proving it.

English

The key point is that the expansion itself isn’t new. The commencement de-risks the timeline.

If hyperscaler volumes are already underwriting a meaningful portion of this capacity, then the real debate shifts from demand to execution:

• Customer qualifications

• Yields

• Laser availability

• Utilization

• Gross margins

$471M in monthly transceiver revenue would annualize to more than $5.6B.

That is an enormous opportunity for $AAOI but management now has to prove it can scale without repeating the mistakes investors still remember.

English

Really positive to see $AAOI announcing their Texas capacity expansion earlier today.

We've known about their expansion plans for a while now.

But it overall supports their proposed 800G/1.6T expansion timelines:

- Q1 2026: 100k monthly capacity

- End 2026: 650k+

- End 2027: 930k+

With $471M of monthly transceiver revenue by mid-2027 forecasted if all goes to plan.

Personally have high confidence that their expansion is underwritted by hyperscaler volumes e.g. $AMZN achoring.

Also, people rightly have PTSD with AAOI management, but seems like they're progressing along the timeline we all expected a few quarters ago.

English

This might be the most important shift in the entire AI trade.

Bank of America calls it a “generational transfer” of free cash flow from hyperscalers to semiconductor companies.

The Magnificent Seven have already spent roughly $234 BILLION on capex this year.

They take the balance-sheet risk.

They build the data centers.

They wait years for AI monetization.

Meanwhile, the semiconductor supply chain gets paid NOW for:

• GPUs

• Memory

• Networking

• Advanced packaging

• Manufacturing equipment

The real AI debate may not be whether value is being created.

It is who captures that value first.

Big Tech is financing the AI buildout.

Semiconductor companies are monetizing it.

$NVDA $MU $TSM $LRCX $AMAT

English

@Brownmoose Insiders always know more and way earlier, i think that's also a reason why TA works

English

$AAOI Shsss one hell of a scoop , got front runned here!

There was good sign pointing a reversal soon like that massive drop in the selling volume.

Now lets be careful , this is right at the EMA50 resistance and most likely get rejected at first

Update in discord

Moose@Brownmoose

$AAOI -25.82% since this post. Now what to look for ? EMA200 Daily which is the support sit at $101 Fib61 retracement sit at $101 Volume going down on the selling. Earning volatility about to hit. This might be one hell of a scoop very soon.

English

Tomorrow is PACKED:

Before the U.S. open:

• $ASML Q2 earnings

• $MS earnings

• $BLK earnings

• $JNJ earnings

8:30 AM ET:

• June Producer Price Index

• Another major inflation test for rates and growth stocks

2:00 PM ET:

• Federal Reserve Beige Book

After the close:

• $UAL earnings

• $JBHT earnings

For semiconductor investors, $ASML is easily the most important.

Watch:

• New bookings and backlog

• EUV and High-NA demand

• Memory and foundry capex

• China exposure

• 2027–2028 capacity visibility

Its commentary could move the entire equipment and semiconductor space:

$AMAT $LRCX $KLAC $TSM $MU

Tomorrow should be interesting. 👀

English

The 700K units/month target gets the attention.

But the planned 350% expansion in laser fabrication capacity may be the more important number.

If lasers remain one of the scarce layers in the optical stack, vertical integration could improve both supply security and margins as 1.6T ramps.

The bull case now depends on qualifications, yields and utilization catching up with the footprint.

Huge opportunity, but execution still decides

English

With the $AAOI expansion announced today, here’s what it actually means for the company.

Their bottleneck was never demand. It was capacity. $AAOI has order visibility stretching well over a year out, and $1B+ guided for 2026.

The demand is already sitting there. They just physically can’t build fast enough to ship it all.

That’s what 400,000 sq ft in Pearland, Texas fixes. Every square foot converts demand they can already see into revenue they can actually recognize.

This isn’t speculative capacity hoping customers show up. The customers are already in line.

It also changes their position in the supply chain. This is US made 800G and 1.6T production at the exact node the industry needs most, right as hyperscalers push to onshore their optics supply.

When big companies want domestic transceiver capacity at scale, the list of options is short, and $AAOI just made itself a bigger part of it.

And the timing lines up with the cycle. 1.6T mass adoption hits late 2026 into 2027. This capacity comes online right into that wave.

They’re not building for today’s orders, they’re building for the ramp they can see coming.

Companies don’t expand on hope. They do it when the orders are visible.

English