Stephen Spratt retweetledi

Happy 100th birthday, Sir David Attenborough 🎉❤️

The broadcaster who changed how we see the natural world.

#DavidAttenborough

English

Stephen Spratt

1.7K posts

@StephenSpratt

DM rates // FX. Opinions my own and do not reflect my employer's position.

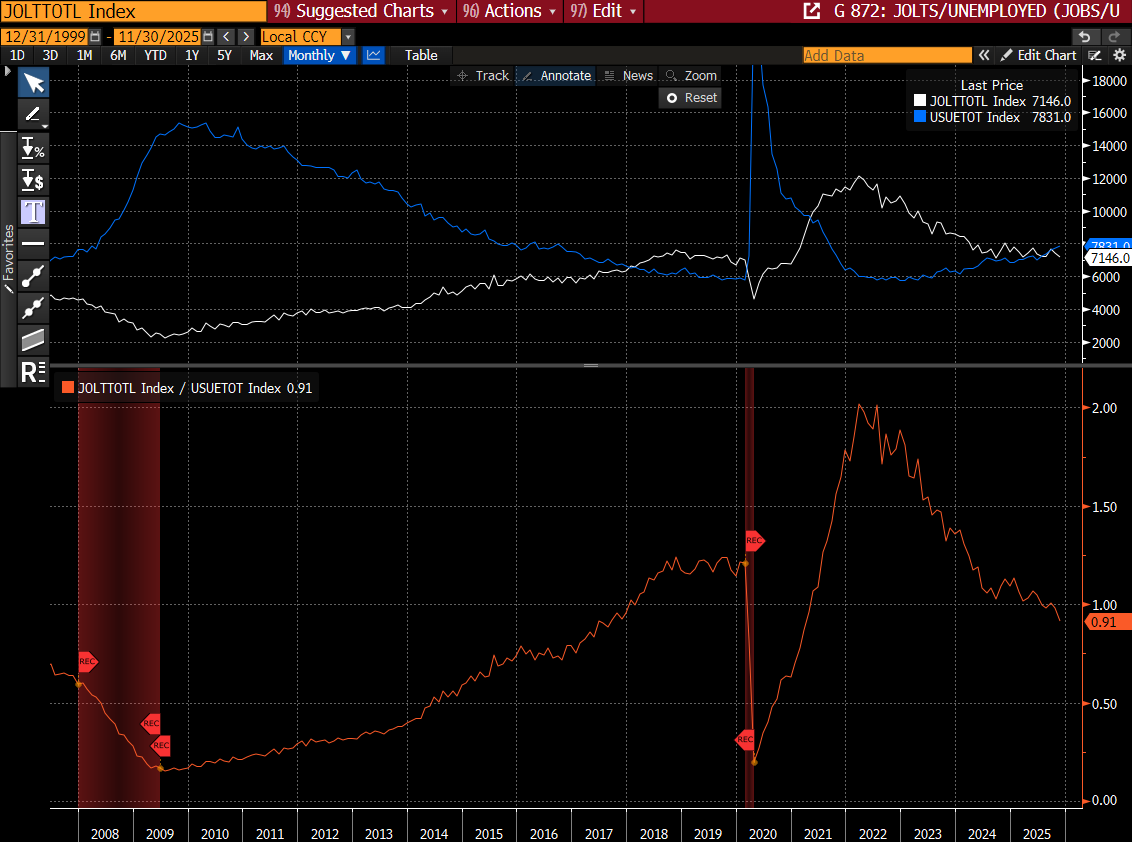

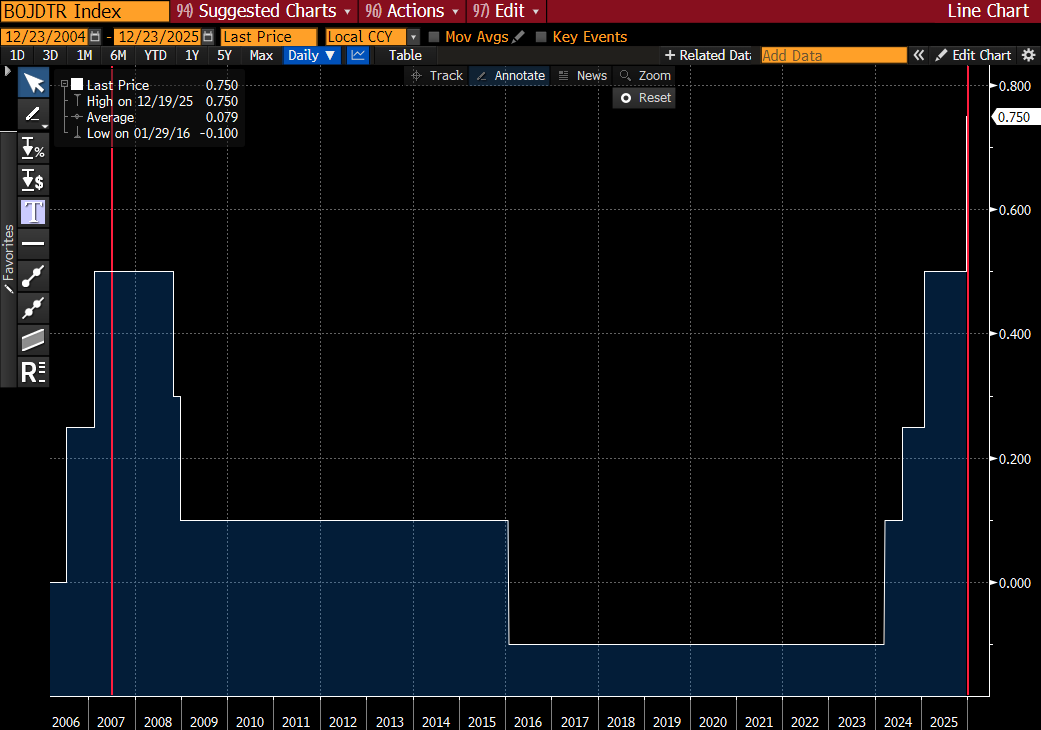

If you're trading rates/macro, it's important to think about global policy cycles. The transition between easing/pause/tightening is vicious. We're seeing this right now in APAC markets... Since mid‑October, 2‑year yields: KRW +51 bp, AUD +48 bp, NZD +34 bp.

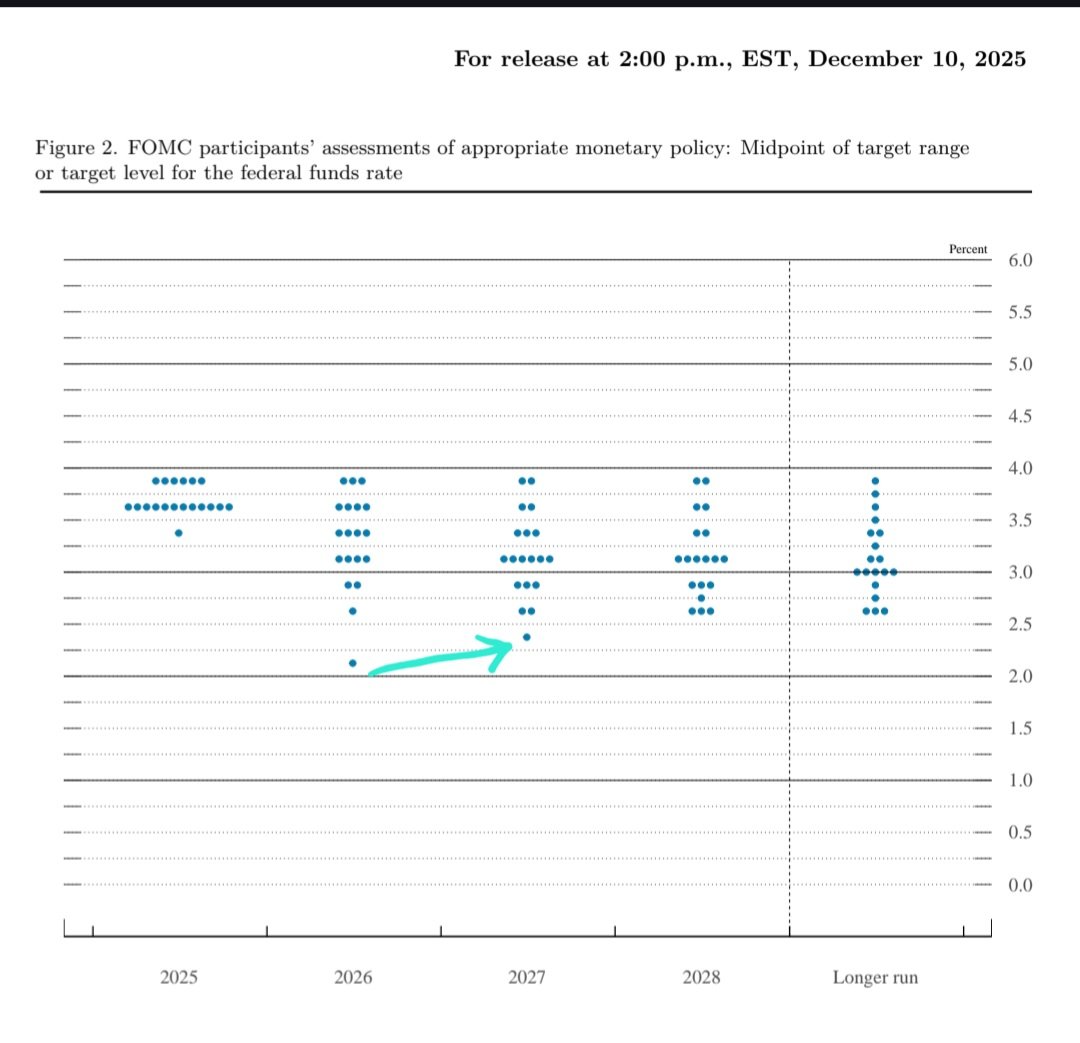

Bessent tells Maria Bartiromo that the Fed's caution on further rate cuts isn't warranted because inflation isn't going to be a problem: "The decision to cut rates by 25 basis points, I applaud. But the language that went with it tells me that this Fed is stuck in the past. Their inflation estimates have been terrible so far this year. They keep coming down, inflation keeps coming down and their models are broken. And I'm just not sure what they're thinking here in terms of signaling that they may not want to cut rates at the December meeting. They've got a lot to answer for not only for this year but for many years past, both in their GDP estimates and their inflation estimates, which are consistently wrong. And we're going to find a leader who is going to revamp the entire institution in terms of process and inner workings."