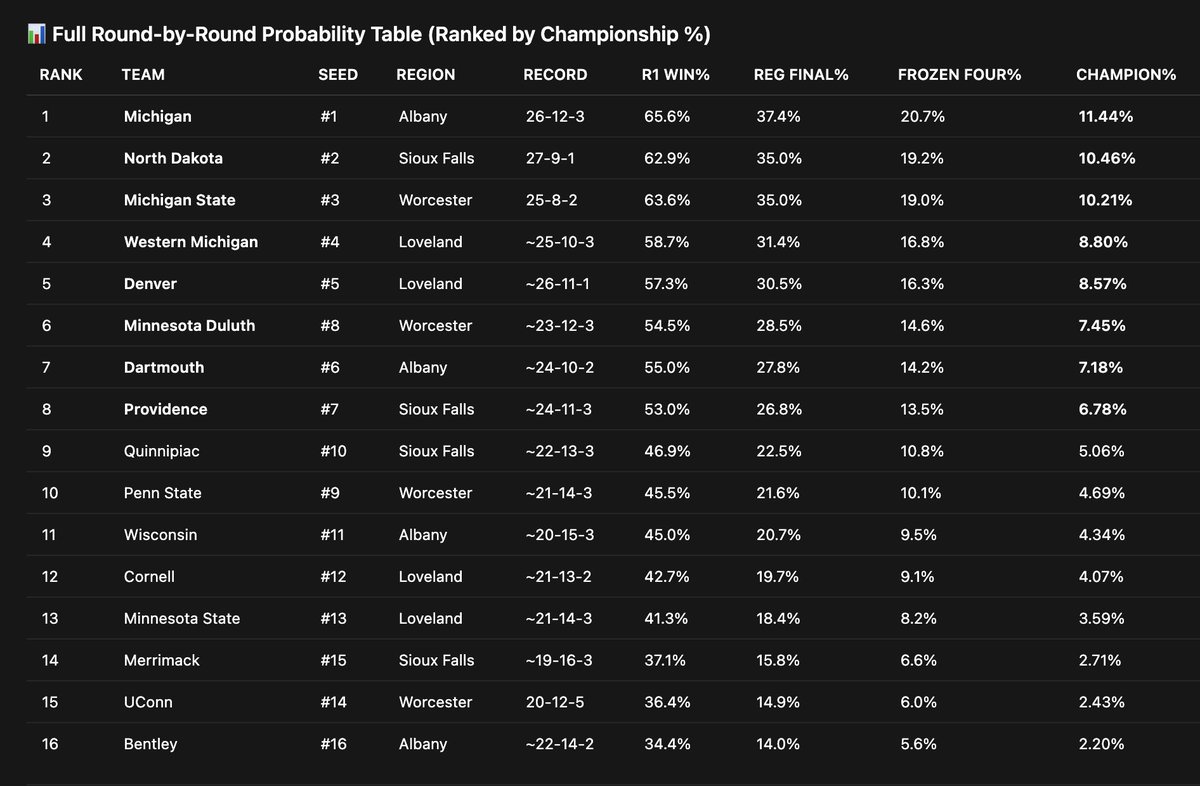

@JaneMcNally_ Jones is about Donato's age? I remember seeing him play in the 80's.

English

steve kim

10.9K posts

Ted Donato ‘91 to Step Away from the Harvard Men’s Ice Hockey Program. A national search for the next Harvard Men’s Ice Hockey head coach will begin immediately. 📰 | gocrim.info/c8x #GoCrimson | #OneCrimson

EXCLUSIVE: Multiple senior HHS officials estimate that, under Gavin Newsom, California's state Medicaid program has lost 25 percent of its budget to fraud. This would mean it is currently losing $50 billion a year to scammers, fraudsters, and organized crime rings.

🚨BREAKING: THE US WOMEN’S HOCKEY TEAM REJECTS TRUMP’S INVITATION TO THE WHITE HOUSE

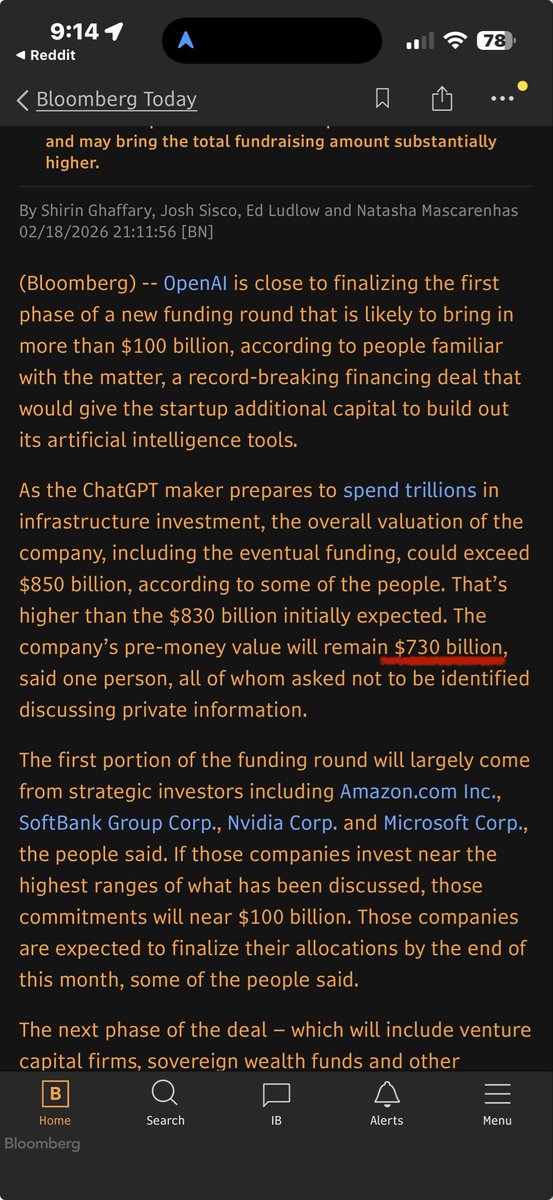

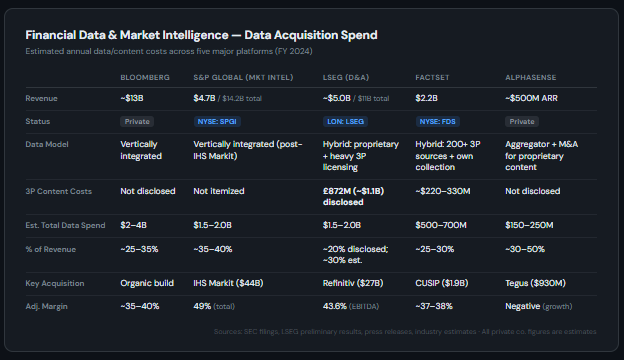

The biggest reason not to be long FDS (I'm not, btw) is that mgmt are probably too sleepy and dumb to realize what kind of gift they've been handed from gods themselves and won't take proper advantage of it.