KaiBosch

446 posts

@PitPatPet @DogsTrust @guidedogs Hi @PitPatPet , I received my pitpat gps and fully charged it yesterday morning. Today I find it’s already out of battery and I’m having to recharge it. That can’t be normal!?!?

English

“Happy International Volunteer Day! 🐶 Big wags to every human helping paws in need. If you’re in the UK and want to help wag-tail joy, check out @DogsTrust, @BlueCrossUK or @GuideDogs — they’re always on the lookout for volunteers. #IVD2025 #VolunteerPaws 🐾”

GIF

English

@CrystalHope1979 Thank you 🙏🏽 very very kind! I have guests on 6th December and thinking I’ll try this tree 🎄 because it looks SO YUM

English

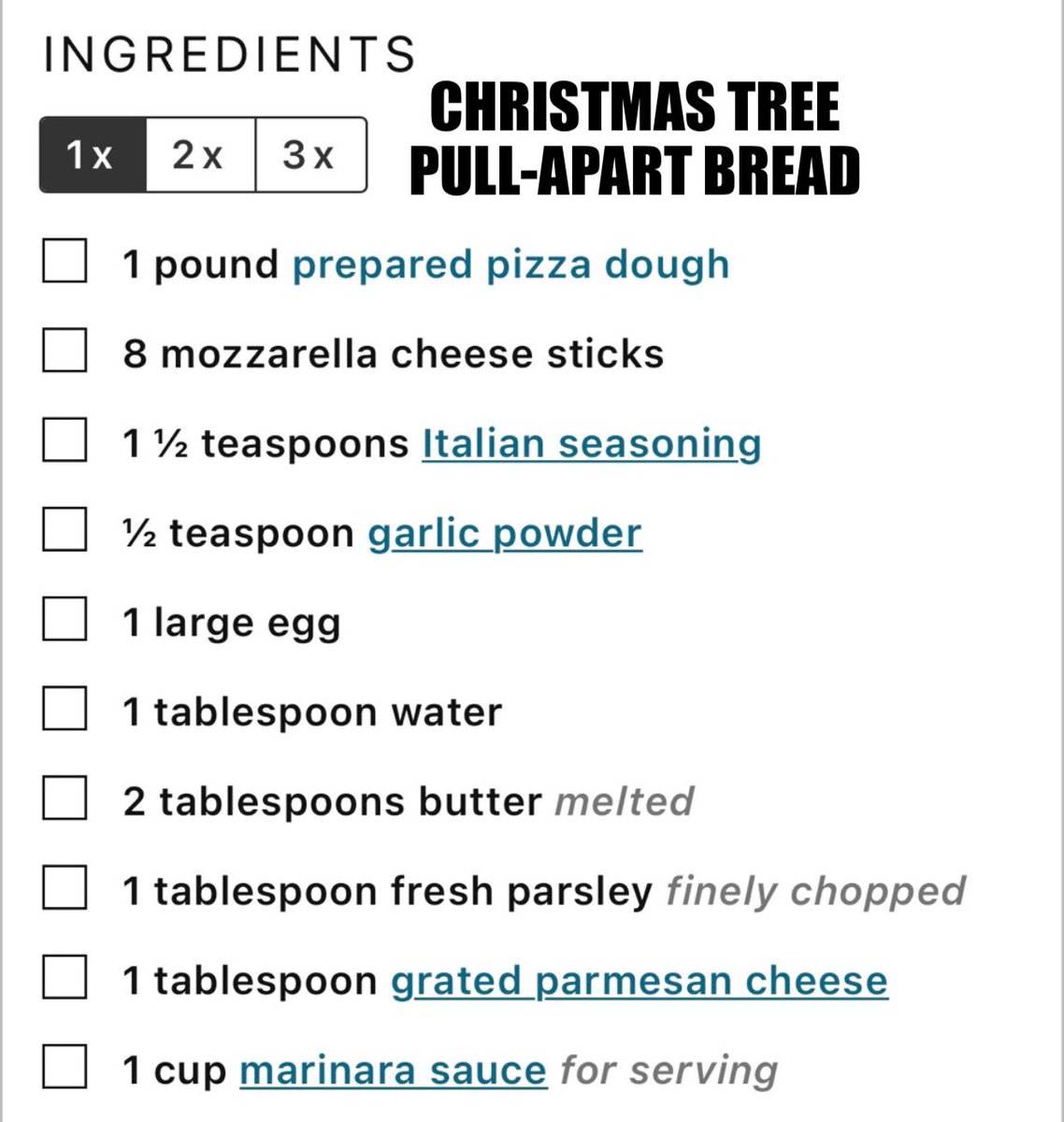

@StockBoscher Hi Kai! Here is the recipe for the Christmas Tree bread and the Pizza Dough Recipe below. 🤗 🎄

English

Cheesy pull-apart Christmas Tree bread.🎄

You can get creative— try adding pepperoni inside! 🍕 😁

English

KaiBosch retweetledi

Asset prices will get crazy this week if the US-China trade deal is announced and the Fed cuts interest rates.

Buckle up.

English

An absolutely insane daily move in Mkango Resources $MKA today.

Up 231% to close the trading day.

Wonder what happened.

This is the right tail outcome potential for all critical mineral miners btw.

English

#MKA Mkango rare earths

Myles McNulty@MylesMcNulty

Was planning to stay offline to make the most of our last few days in Puglia, but this surge in interest in the ex-China rare earths space today really is phenomenal. The implications for core holding Mkango Resources #MKA are wonderful. There are now 11 pure-play rare earths businesses listed on ex-China public exchanges that are valued at in excess of $500m. All but the top two in the list below are pre-revenue companies (at least, in any material sense). MP Materials $MP - $17.0bn Lynas Rare Earths $LYC - $13.3bn USA Rare Earth $USAR - $4.6bn Critical Metals Corp $CRML - $2.3bn Dateline Resources $DTR - $1.2bn Rare Element Resources $REEMF - $771m Idaho Strategic Resources $IDR - $724m Pensana Rare Earths #PRE - $674m Arafura Rare Earths $ARU - $663m Ucore Rare Metals $UCU - $591m Aclara Resources $ARA - $534m Even despite its 13x share price uplift over the past 12 months, Mkango #MKA, closing at 65p today, has a mkt cap of $299m. Of the 9 pre-producers in the list above, only PRE and ARU are (arguably) further ahead in the race to bring their respective mines online. Mkango's Songwe Hill is backed by the US government ($4.6m grant, a further $100m loan for mine build under consideration). It is also backed by the EU - it's been designated a "Strategic Project by the European Commission under the Critical Raw Materials Act." In reality, this means that it's reasonably likely to expect Songwe Hill to receive similar financial support to that which the US Gvt is considering. Mkango's proposed rare earths separation plant, Pulawy (to be built in Poland), has also been designated a Strategic Project by the EC. Personally, I think the FEED will demonstrate an average annual EBITDA of the combined projects of somewhere around the $200m-$300m mark - and Songwe Hill's initial mine life is two decades. But let's see. Anyhow - given the backing of the EU and US, and its advanced stage of development, I think it's fair - given the peer group valuations above - for those two assets to be valued at >$700m, as of today. Fortunately for us Mkango investors, Songwe Hill and Pulawy are being spun out onto NASDAQ in the next 2-4 moths via a SPAC listing - the company is to be called Mkango Rare Earths $MKAR). The proposed value of MKA's holding is $400m (being 40m shares at the listing price of $10). The likely mkt cap will be around $500m at listing price, with MKA retaining a circa 80% shareholding in MKAR. ...... So - the upside for MKA from its current mkt cap is blindingly obvious, given that it is ex-UK investment communities driving lofty valuations in the REE space this year, and that MKA is resultantly listing its assets on NASDAQ in the near term. BUT - that's just accounting for Mkango's upstream assets. The much more valuable side of the company is its 80% equity interest in NdFeB magnet recycling and production business, HyProMag. There is very limited rare earths IP outside of China. HyProMag's hydrogen-based recycling patents are - in my view - likely the most important worldwide. If anyone has any other suggestions, I'd love to hear them. AI (esp. robotics) is going to drive incredible improvements in recycling sorting and pre-processing (shredding, etc.). There are many tens of thousands of tonnes of NdFeB in waste streams, or in active circulation, in the US, EU East Asia, South Asia, Africa, South and Central America right now. With a low cost recycling and remanufacturing process, virgin / new permanent magnet demand could be reduced by 20%, perhaps 30% worldwide. HyProMag provides that simple and extremely low cost flowsheet. Short-loop recycling. It doesn't deal in any other of the 15 REEs than the magnet REEs. No oversupplied metals (cerium, etc.) touched at all. Purely recycling NdPr and DyTb, to repress into new magnets. In just 2-3 months, HyProMag will be recycling / manufacturing NdFeB magnets in two nations (UK and Germany); and within 18-20 months, in three nations (with the first US plant coming online sometime in H1 2027). Can anyone tell me if there's a company manufacturing permanent magnets in two countries at the moment? I don't know of any. In 3-4 years, HyProMag could be operating magnet recycling and manufacturing plants in 6 nations. It has publicly repeatedly stated that it's in discussions to open plants in Japan, South Korea and Canada, in addition to the first three nations. The US Gvt has not only backed Songwe Hill, but has provided a letter of interest to HyProMag for a $92m low cost loan for the first plant build-out. In its original design, each US plant was forecast to generate around $66m EBITDA per annum, with a 40-year life. But the plant design has been expanded by circa 50% now, to ~1,550 tonnes per annum of NdFeB material. Recently asked by the US Gvt how many plants would be ideal for fulfilling the needs of the USA, HyProMag responded, 6-7 plants across the nation. Each one has an NPV of $650-$700m, pre-production. Now imagine HyProMag rolling out 3-4 such plants in Japan, and elsewhere in the EU besides Germany. Then South Korea. Canada. India. Central and South America. I maintain that HyProMag should be one of the most valuable ex-China REE companies after MP and LYC. It seems pretty certain the HyProMag will list on NASDAQ in the nearish future. Look at USAR's mkt cap above. $4.6bn. It will in late 2026 be manufacturing NdFeB magnets. Zero IP, zero recycling capability. 3-4 times the cost of sales as HyProMag, per kg of NdFeB magnet. What valuation will HyProMag fetch when it lists? I suspect multiple $ billions, in this environment. Mkango - already operating, constructing or designing plants in 5 nations right now (Malawi, Poland, UK, Germany, US) - has the largest international footprint of any rare earths company in the world. The growth opportunity here is obscene, with the critical minerals version of Operation Warpspeed now underway. The market is slowly cottoning on, but there is a HUGE open road ahead.

Filipino

@TedHZhang #MKA Mkango Rare Earth plc. US LISTING: definitive business combination agreement between its subsidiary Lancaster Exploration (to be renamed Mkango Rare Earths) and Crown PropTech Acquisitions (CPTK), a SPAC, with the goal of listing on Nasdaq in Q4 2025

English

@venuguntupli7 #MKA Mkango Rare Earth plc. US LISTING: definitive business combination agreement between its subsidiary Lancaster Exploration (to be renamed Mkango Rare Earths) and Crown PropTech Acquisitions (CPTK), a SPAC, with the goal of listing on Nasdaq in Q4 2025

English

@sam_badawi #MKA Mkango plc +5.93%%. US LISTING: definitive business combination agreement between its subsidiary Lancaster Exploration (to be renamed Mkango Rare Earths) and Crown PropTech Acquisitions (CPTK), a SPAC, with the goal of listing on Nasdaq in Q4 2025

English

You think $BMNR $IREN $HOOD are the only stocks ripping overnight? Rare earths are having a party.

$CRML +17.42%

$USAR +15.00%

$UAMY +13.02%

$IDR +8.14%

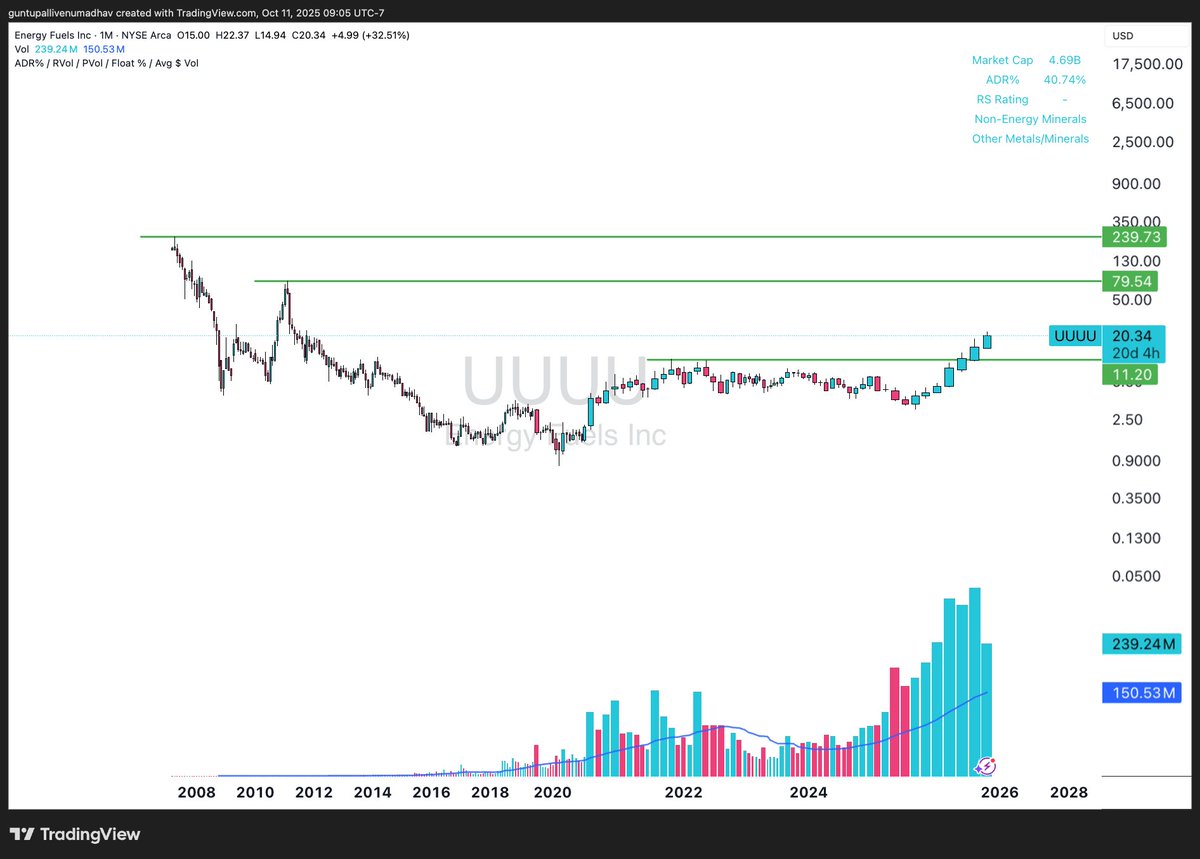

$UUUU +7.37%

$TMC +5.81%

$MP +5.56%

$TMRC +5.01%

$UMC +1.81%

Sam Badawi@Sam_Badawi

WHO ARE THE REAL WINNERS FROM THE RECENT TARIFF TENSIONS? Rare earth metals. Here’s how they performed on Friday. $SPY [-2.70%] $QQQ [-3.47%] $TMRC +23.99% $UAMY +12.22% $MP +8.49% $PPTA +7.73% $IDR +6.05% $NB +5.59% $USAR +4.96% $UUUU +3.25% $CRML +1.84% $AREC +0.99% $IPX -1.86% $TMC -5.28%

English

@anandragn #MKA Mkango plc +5.93%. US LISTING: definitive business combination agreement between its subsidiary Lancaster Exploration (to be renamed Mkango Rare Earths) and Crown PropTech Acquisitions (CPTK), a SPAC, with the goal of listing on Nasdaq in Q4 2025

English

@venuguntupli7 #MKA Mkango plc +10.07%. US LISTING: definitive business combination agreement between its subsidiary Lancaster Exploration (to be renamed Mkango Rare Earths) and Crown PropTech Acquisitions (CPTK), a SPAC, with the goal of listing on Nasdaq in Q4 2025

English

Some of the strongest names and sectors heading into next week:

Rare Earth & Uranium theme - serious strength across the board.

$NB 10-year base, heavy accumulation, trading above IPO AVWAP and long-term MA's

$UAMY – broke a 45-year base, trending above IPO AVWAP and long-term MA's

$PPTA & $USAR – both breaking 20-year bases and holding above IPO AVWAP

$UUUU – still has plenty of juice left $UEC – breakout from a 20-year base $MP – multi-year base breakout

Every single one of these closed green on Friday.

Add them to your watchlist and track their strength in the coming weeks and months.

English

@SanCompounding #MKA Mkango plc +10.07%. US LISTING: definitive business combination agreement between its subsidiary Lancaster Exploration (to be renamed Mkango Rare Earths) and Crown PropTech Acquisitions (CPTK), a SPAC, with the goal of listing on Nasdaq in Q4 2025

English

Rare Earths are in demand but it’s tough to pick stocks. So buying an ETF is a great choice !!

There are couple ETFs focused on rare earth stocks.

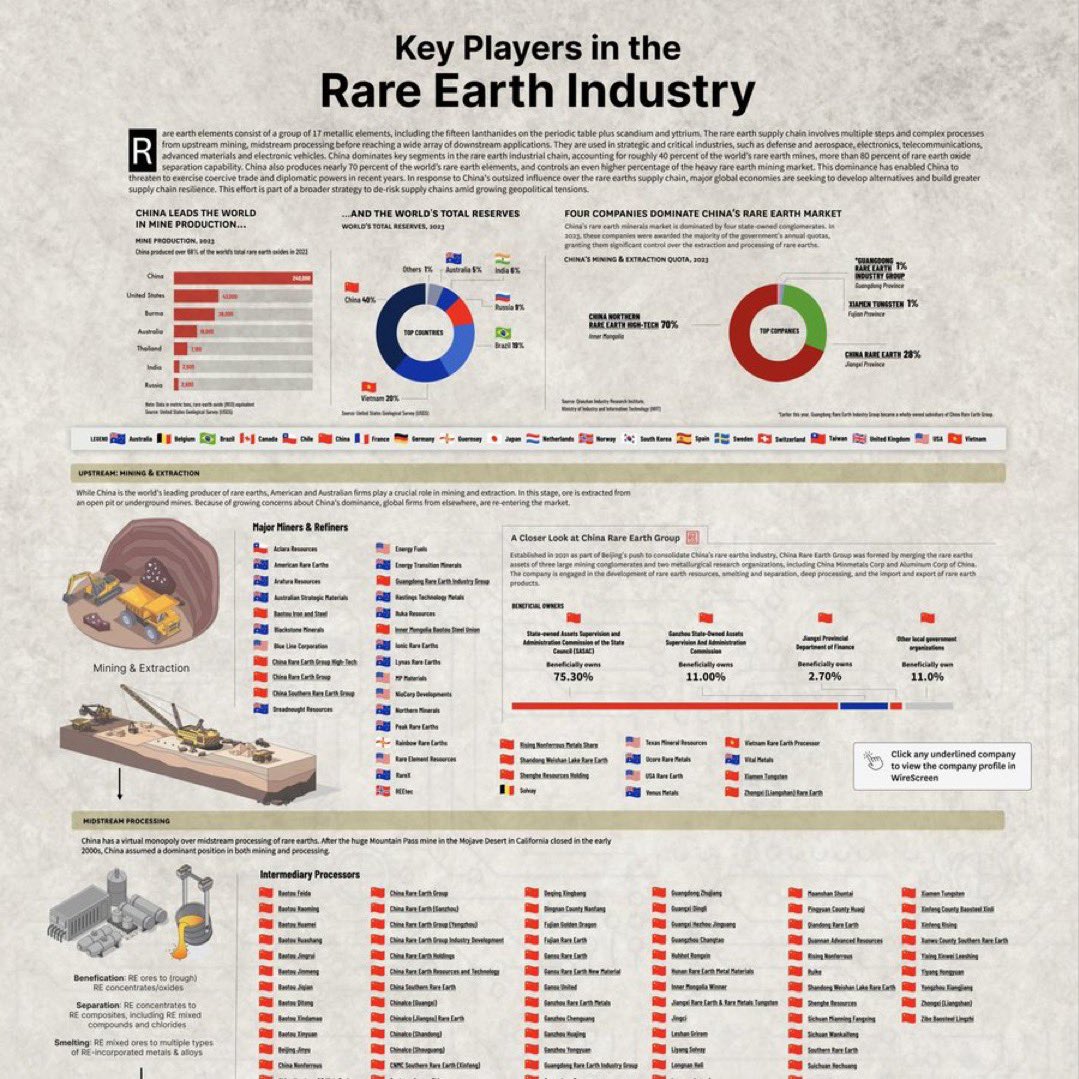

1. VanEck Rare Earth and Strategic Metals ETF ( $REMX) — Companies involved in mining, refining, and producing rare earth and strategic metals. Below is a detailed breakdown of the top 16 holdings 👇

1. TSX: $LAC - Lithium Americas Corp. (8.09%)

2. ASX: $LYC - Lynas Rare Earths Limited (7.63%)

3. $MP - MP Materials Corp. (7.12%)

4. ASX: $PLS - Pilbara Minerals Limited (6.42%)

5. $ALB - Albemarle Corporation (6.38%)

6. $SHA:600111 - China Northern Rare Earth (Group) High-Tech Co.,Ltd (5.78%)

7. $GNENF - Ganfeng Lithium Group Co., Ltd. (5.16%)

8. ASX: $ILU - Iluka Resources Limited (4.82%)

9. ASX: $LTR - Liontown Resources Limited (4.71%)

10. $SQM - Sociedad Química y Minera de Chile S.A. (4.60%)

11. $IPX - IperionX Limited (4.40%)

12. ASX: $VUL - Vulcan Energy Resources Limited (4.16%)

13. AMS: $AMG - AMG Critical Materials N.V. (3.98%)

14. EPA: $ERA - ERAMET S.A. (3.72%)

15. SHA:600549 - Xiamen Tungsten Co.,Ltd. (3.57%)

16. SHA:600392 - Shenghe Resources Holding Co., Ltd (3.52%)

Another option is the Sprott Energy Transition Materials ETF ( $SETM), which includes exposure to rare earths alongside other metals like copper, uranium, and nickel

English

@Speculator_io #MKA Mkango plc +10.07%. US LISTING: definitive business combination agreement between its subsidiary Lancaster Exploration (to be renamed Mkango Rare Earths) and Crown PropTech Acquisitions (CPTK), a SPAC, with the goal of listing on Nasdaq in Q4 2025

English

𝗠𝗼𝗿𝗴𝗮𝗻 𝗦𝘁𝗮𝗻𝗹𝗲𝘆'𝘀 𝗡𝗮𝘁𝗶𝗼𝗻𝗮𝗹 𝗦𝗲𝗰𝘂𝗿𝗶𝘁𝘆 𝗜𝗻𝗱𝗲𝘅:

𝗥𝗮𝗿𝗲 𝗘𝗮𝗿𝘁𝗵s

$TMC TMC the Metals Company

$UAMY United States Antimony

$MP MP Materials

$USAR USA Rare Earth

$IDR Idaho Strategic Resources

$NB NioCorp

$UUUU Energy Fuels

$CRML Critical Metals

$TMQ Trilogy Metals

$AREC American Resources

$TMRC Texas Mineral Resources

$REEMF Rare Element Resources

$ERO Ero Copper

$PPTA Perpetua Resources

𝗕𝗮𝘁𝘁𝗲𝗿𝗶𝗲𝘀

$TSLA Tesla

$EOSE Eos Energy

$SEI Solaris Energy Infrastructure

$AMPX Amprius

$MVST Microvast

$BLDP Ballard Power Systems

$QS QuantumScape

$ABAT American Battery Technology

$IE Ivanhoe Electric

𝗟𝗶𝘁𝗵𝗶𝘂𝗺

$ALB Albemarle

$SGML Sigma Lithium

$LAC Lithium Americas

$SLI Standard Lithium

𝗡𝘂𝗰𝗹𝗲𝗮𝗿

$OKLO Oklo

$LTBR Lightbridge

$ASPI ASP Isotopes

$LEU Centrus Energy

$CCJ Cameco

$BWXT BWX Technologies

$URG Uranium Energy

$NNE NANO Nuclear Energy

$SMR NuScale

$NXE NexGen Energy

$URC Uranium Royalty

$EU Encore Energy

$MIR Mirion

English

@sam_badawi #MKA Mkango plc +10.07%. US LISTING: definitive business combination agreement between its subsidiary Lancaster Exploration (to be renamed Mkango Rare Earths) and Crown PropTech Acquisitions (CPTK), a SPAC, with the goal of listing on Nasdaq in Q4 2025

English

WHO ARE THE REAL WINNERS FROM THE RECENT TARIFF TENSIONS?

Rare earth metals. Here’s how they performed on Friday.

$SPY [-2.70%] $QQQ [-3.47%]

$TMRC +23.99%

$UAMY +12.22%

$MP +8.49%

$PPTA +7.73%

$IDR +6.05%

$NB +5.59%

$USAR +4.96%

$UUUU +3.25%

$CRML +1.84%

$AREC +0.99%

$IPX -1.86%

$TMC -5.28%

English

@genericnomen @coinbureau On a desktop device, open up the trading page for one of the bitcoin etns e.g. LSE:WXBT (i couldn't seem to do this oon mobile) and there's a button labelled "learn more about crypto ETNs" which takes you to the right place.

English

🚨UK SCRAPS 4-YEAR CRYPTO BAN!

The UK has lifted its 4-year ban on crypto exchange-traded notes, reopening access for retail investors.

English

I’m working out everyday now. Tennis, weights, running etc. My resting heart rate is really good and I train at quite a high rate too. So my question is, Why am I still fucking fat and exhausted all the cunting time?

English

@MylesMcNulty Last deal was 10x on EV / Sales ratio which would take this over £20 - Spotify acquired Gimlet on EV of 10.2 x

English

Mark Kleinman@MarkKleinmanSky

Exclusive: Audioboom, the London-listed podcast producer whose titles include F1: Beyond The Grid, is working with bankers to explore a sale of the company after receiving a number of expressions of interest; Audioboom has a market cap of close to £100m. news.sky.com/story/formula-…

QME

Despite its ~800% share price gain over the past 12 months, Mkango #MKA remains chronically undervalued versus the rare earths international peer group.

Here's a list of the key listed pure-play rare earths companies. Note that only the top two - $MP and $LYC - are actually mining. All of the others are explorers / developers.

Simply put, I believe that – all else being equal - Mkango should have the third highest mkt cap of this peer group (after only MP and LYC).

Now – it may be that the reader thinks the likes of USAR, DTR and CRML to be chronically overvalued. Such an opinion may indeed be valid. But when cash flows are unpredictable at best, and in fact non-existent in most cases above, then relative valuation analysis really take priority.

I am not stating explicitly that I believe that MKA should be valued at >$2.85bn right now (i.e. higher than USAR). But I am stating that it should be worth more than USAR.

......

MKA has two divisions. The first one - the original business - is centered upon MKA's proposed mine in Malawi, named Songwe Hill. This asset is nearing construction-ready. It has a definitive feasibility study, all environmental permits approved, and a mine development agreement with the Malawi government.

Songwe Hill has secured support from some of the most powerful of agencies in the space:

i) SH has been designated a Strategic Project by the European Commission under the Critical Raw Materials Act;

ii) The EU has already financially backed SH (via a small direct equity investment through its EIT RawMaterials body in Q3 2025);

iii) SH is a part of the Minerals Security Partnership, a US-led alliance;

iv) The US Government has now provided a $4.6m grant to fund the FEED at SH, with a further $100m loan for construction now under consideration.

Look at the above list of peers. SH is years ahead of the deposits of DTR, CRML, REEMF, in terms of time to first production. It is also the most widely backed by various major government agencies (no other deposit has such wide ranging support from both the US, the MSP and the EU).

As such, were SH listed on a US exchange, it’s simple to see that it could be valued at more than CRML (currently ~$800m).

......

But there’s an additional aspect to MKA’s upstream business. It is in the process of designing a separation plant in Pulawy, Poland to process the feedstock from SH. This plant will materially enhance the economics of SH. Pulawy has received the same support as SH has from the EU (see i) and ii) above).

The good news for Mkanog shareholders is that mgmt. noted the colossal gulf in valuation attributed to rare earths projects by optimistic US investors, compared to dullard UK investors – and are in the advanced stages of launching the two projects onto NASDAQ via a SPAC merger deal. The new company is to be called Mkango Rare Earths ($MKAR). The value of MKA’s share in MKAR at the listing price will be $400m (being 40m shares at $10), and will likely amount to a circa 80% shareholding.

The deal is likely to complete before Christmas. Using MKA’s current number of shares in issue (346m), the value of the stake at IPO price would be circa 86p per MKA share. That’s an 85% premium to MKA’s current share price of 46.5p.

……

But the more valuable part of MKA is its second business – HyProMag, a rare earth magnet recycling and manufacturing company. In summary, HyProMag is the only company in the major ex-China territories that - through patented IP – can use hydrogen in its process to recycle rare earth permanent magnets. I provided a summary of the tech and its implications, in this blog back in March:

mylesmcnultytrades.substack.com/p/mkango-resou…

So: owing to its unique, heavily protected recycling process, HyProMag is going to be the cheapest manufacturer of rare earth permanent magnets outside of China. It can unlock native sources of NdFeB material in dozens of nations across the world (that is to say, old magnets embedded in scrap throughout waste chains) at a substantially lower cost than anyone else can.

HyProMag is already operating its first magnet recycling/manufacturing plant in the UK; will complete construction of its second plant, in Germany, in the next 2-3 months; and intends to commence construction at its first plant in the US in the next 2-5 months. It is also progressing plans to construct plants in Japan, as well as Canada and South Korea (although the launch plans for these three additional nations have yet to be revealed).

In short, HyProMag already has the largest international footprint in the rare earth magnet recycling / manufacturing space of any company in the world. And in several years, could have the largest capacity of any business outside of China.

......

To revert to the above peers, given its vastly superior margin, not having to rely on others’ feedstock, and its rapidly expanding international footprint; I believe that HyProMag should be trading at a substantial premium to USAR – the only listed magnet manufacturer besides MP in the US (although in reality, USAR will not likely be producing magnets until late next year).

Yet as at the time of writing, USAR’s mkt cap is some 13 times higher than MKA’s. Yes, USAR has just made a $200m acquisition. But MKA more than offsets that by having a listed asset in just 2-4 months (being its 80% stake in the soon-to-be-listed MKAR) worth $400m at the IPO price.

……

The absurd discount exists due to Mkango being listed in the UK, and USAR being listed in the US.

An example that really sums up the difference in valuations ascribed by US investors, versus UK investors:

Yesterday, USAR’s new CEO mentioned in an interview after hours that the company was in close contact with the Trump administration. The stock price increased by 10%, or circa $250m, in after-hours trading. A simple mention that they were even in talks with the US government, resulted in US investors driving a mkt cap increase in a mere 4 hours of more than Mkango’s entire current mkt cap.

To note, Mkango (and its US partner, CoTec) have been open that they have been in extensive talks with the US government for over a year now. Indeed, they have already secured a letter of interest from the US Government to provide a low cost loan of up to $92m for the construction costs of the first HyProMag plant in the US.

……

The obvious solution? The combined HyProMag companies are listed on NASDAQ, ASAP. It is quite simple to see that by mid next year, MKA could have a 75-80% stake in MKAR that has a mkt cap of $800m+, and a 60-65% stake in HyProMag that has a mkt cap of $2bn to $3bn – and possibly a lot more, if concrete plans for Asia expansion with a major partner (JOGMEC involvement?) are announced beforehand.

The UK market is a disaster, but spin outs / transfers to superior exchanges abroad (in this case, NASDAQ!) can provide exceptional investment opportunity.

I can see MKA doing another 9x from 46p, over the next 12 months.

English