Sabitlenmiş Tweet

Suby

2.4K posts

Suby

@subyhq

Payment Gateway: accept card & crypto payments. Get paid in stablecoins. For SaaS & communities for Discord & Telegram

Stablecoin Payments Katılım Ekim 2024

9 Takip Edilen3.1K Takipçiler

Suby retweetledi

I'm looking for the best UI/UX designer to redesign our payment checkout.

UIs I like: @AcctualTeam, for example. I want attention to detail, elements that reassure the customer, and smooth animations.

Thank you for your help.

English

Suby retweetledi

My ambition is to make @subyhq the first billion-dollar payment company without raising funds, just grind, lean & AI-driven processes, and listening to my gut and my clients.

And this is not an April Fool's joke

Wish me luck

English

Suby retweetledi

Payment service is provided by @subyhq, huge thanks to @gaspardlezin for setting me up!

English

Suby retweetledi

@levelsio Good to see Pieter building ideas.directory, we got few things working a while ago:

- idea validator

- idea MVP generator

- "Want this", which is like wait list without Stripe but will be adding @subyhq support instead

English

@FrancoEch esims are not allowed unfortunately, but if you've other businesses feel free to apply

English

@subyhq Nice, can I sell esims? Or is not allowed. Can I sign up from argentina?

English

@monogramdude @Kouwalsen 5% per transaction card

And sono 0% on stablecoins :)

English

@Kouwalsen @subyhq First time I heard about it. How are the conversion rates and fees?

English

Suby retweetledi

Suby retweetledi

We spent a year in stealth. Building, refusing, iterating. Today we unveil what we built 👇

Just us, our merchants, and the product.

We were heads down looking for product-market fit. That meant saying no to a lot, no shortcuts, no grey-area merchants, no cutting corners on compliance. Just building the right thing for the right people. We found it. Now we grow.

Suby is payment infrastructure for online businesses. Card, e-wallet, bank, and stablecoin. We operate as a Merchant of Record, meaning we handle the payment complexity, the compliance, the reconciliation. So merchants can focus on what they actually do: selling.

We're not just another payment gateway. We're the full stack. Scaling this the right way means having people who fully own their domain.

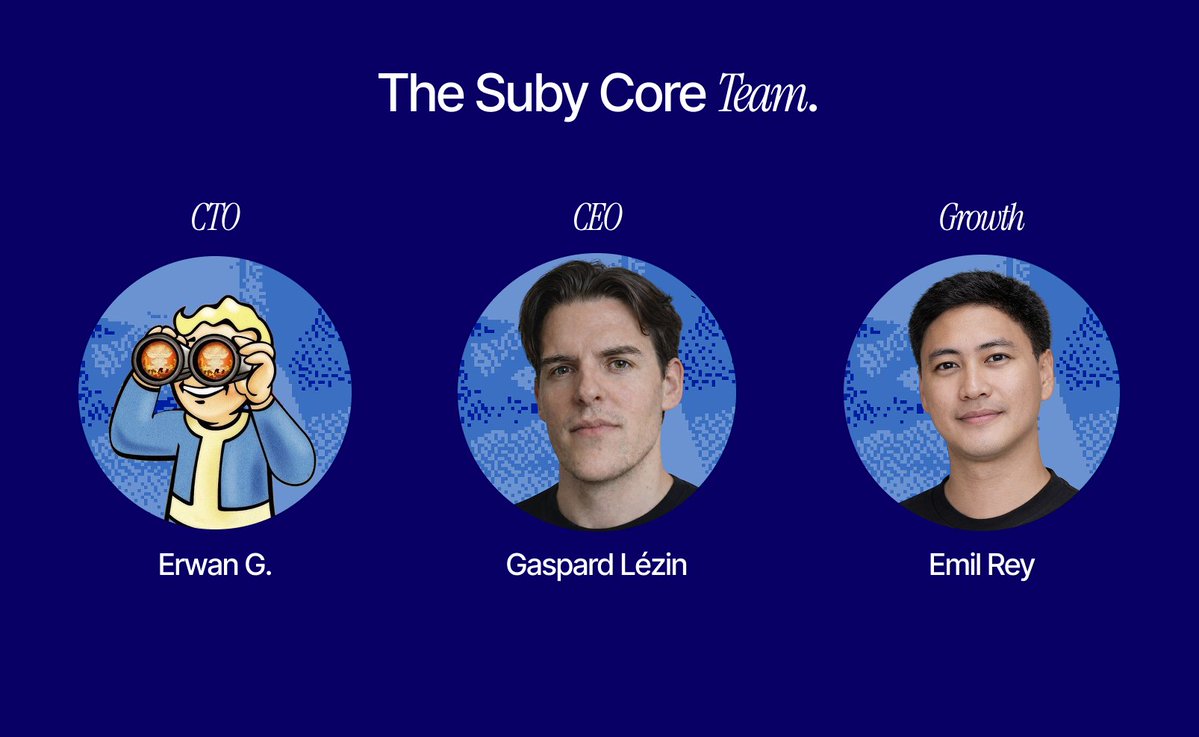

So here's who's running it:

- @etherwan_ : CTO - API, infra, stack. Every transaction that flows through Suby runs on what he built. Quietly, consistently, at scale.

- @ert_suby: Growth - Acquisition, activation, retention. He turns individual merchants into a network.

- Me: CEO - Business, product, GTM. Connecting the dots between what merchants need and what we build.

And behind all of us, a dedicated legal & compliance team making sure every merchant on Suby operates on solid ground.

One year of stealth taught us one thing: build something real before you talk about it. Now we're talking and if you're selling online, you should be too.

PS: I post about payments, stablecoins & the founder journey every week. Follow me for more!

English

Suby retweetledi

It’s official: we’re now officially paying our freelancers with Suby instead of @Upwork!!

0% fees on stablecoins payments

English

Suby retweetledi

.@Mastercard has 80% gross margins. They don't move money, they move messages. Yesterday they paid $1.8B for BVNK, because stablecoins are becoming a new rail, and they intend to sit in the middle of that one too.

Mastercard isn't a payment company. It's a messaging network.

Every card payment is a sequence of messages: authorization, clearing, settlement. Mastercard sits in the middle, routing information between banks, without holding funds, without lending a dollar, without taking any credit risk.

On a $100 card payment, the merchant pays ~1.5% in fees. Mastercard takes ~$0.20 of that. The rest flows to the issuing bank and the acquirer.

They never touch the money. They charge for every message that moves it.

And fees aren't flat, they scale with complexity.

- Domestic transaction? ~$0.20.

- Cross-border with FX conversion? Network fees can exceed $1.00 on that same $100.

The more fragmented the world becomes, across countries, currencies, and rails, the more valuable their coordination layer gets.

Their real moat though? The chicken-and-egg no one can crack.

In payments, there's the Switch (the rail) and the Scheme (the network). Mastercard is a Scheme.

To challenge them, you need merchants to accept the card. But merchants only accept cards that cardholders carry. And cardholders only carry cards that merchants accept. You need banks, merchants, and consumers, simultaneously, at scale, across 210+ countries. No one has done it. Not in decades.

That's why Mastercard doesn't need to own the money. They own the network effect.

So why BVNK?

Stablecoins are becoming a new rail, especially for cross-border transfers, remittances, and B2B flows. BVNK operates on all major blockchains across 130+ countries.

Mastercard isn't scared of stablecoins. They're doing what they've always done: sitting at the coordination layer of a new rail, and charging fees on every message flowing through it.

The business model doesn't change. The rail does.

PS: I post about payments, stablecoins & the founder journey every week. Follow me for more!

English

Suby retweetledi