@Mar49931H @KobeissiLetter If Iran controls the Strait, then Chinese vessels may be unaffected. However, the panda is possibly smiling in the hope that the end of empire arrives sooner rather than later, with minimal effort.

English

Sugar Market News

51.4K posts

@SugarAlerts

International sugar news and analysis, ethanol, agriculture and the environment. Physicals, futures, options, stocks and ETFs. Commodities | Biofuels | Trading

Secondary impacts: Brazil, the world's largest #sugar producer and exporter, is expected to cut shipments in the 2026/27 season that starts in April by 14.2% as mills divert sugarcane to make ethanol due to high energy prices, consultancy Safras & Mercado said on Thursday. Source: Reuters

🚨🇷🇺🇪🇺 Russia eyeing a gasoline export ban for producers starting April 1? Authorities are actively discussing reinstating it; no final decision yet, but focused on gasoline only (not diesel). If that happens... It's gonna be a kick in Europe's balls, as they're already struggling from the closure of Strait of Hormuz Europe is sooooo screwed this year Source: @zerohedge

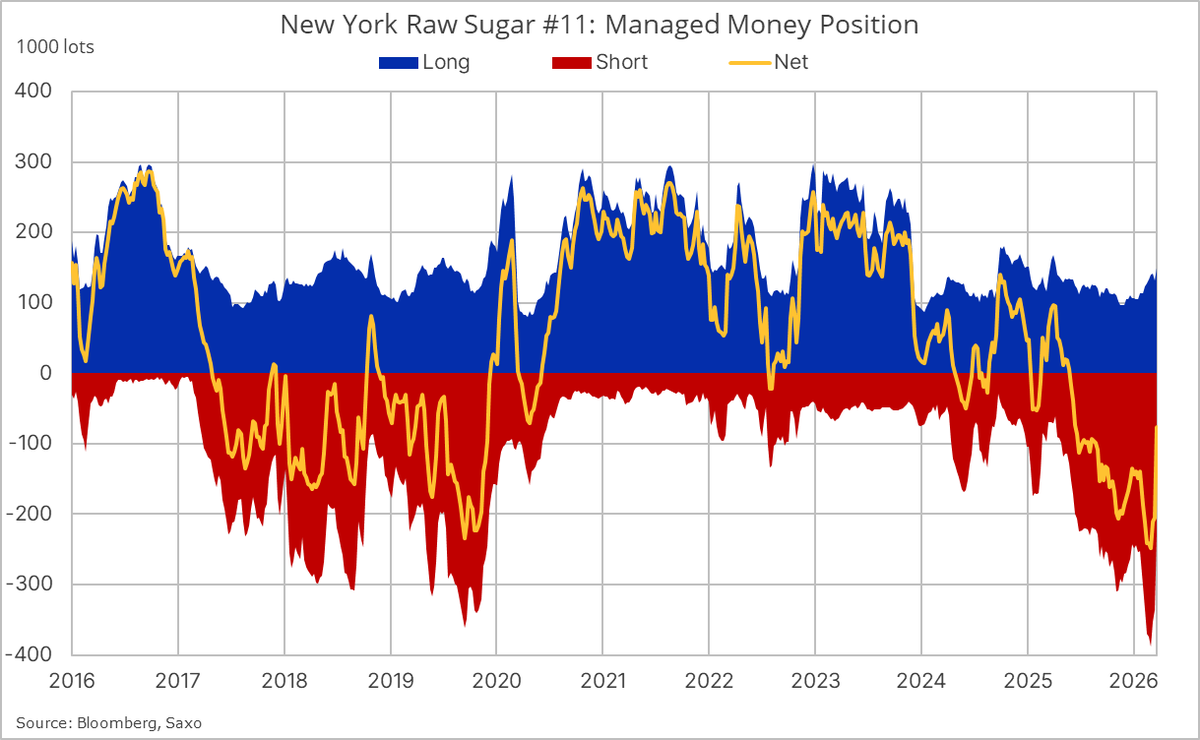

The most underpriced commodity right now might be sugar, and that is because Brazilian ethanol is the solver of the global gasoline market shortage. Here's the Brazil gasoline arbitrage nobody is talking about. 1/ Brazil is a net importer of 150'000 barrels per day of gasoline and blending components (light ends). A massive, structural deficit for the world's largest ethanol producer. That gasoline import is about 9 million tonnes per year of sugar-equivalent ethanol sitting one government price decision away from being diverted. Brazil is also a net importer of 300 kbd of diesel for farm and trucking, and boatloats of nitrogen fertilizers, but that is story for another day. 2/ Why? Because Brazilian domestic gasoline prices are currently at ~60% of international levels. Petrobras imports at world prices, sells cheap. The government eats the subsidy. 3/ This matters enormously for the sugar/ethanol split. Brazil's flex-fuel fleet prices ethanol at pump parity — i.e. ~70-75% of gasoline. If gasoline is at 60% of world prices, domestic ethanol is worth ~42-45% of international gasoline equivalent. 4/ Now stress-test with Hormuz. A sustained closure creates a persisting global gasoline price spike. Petrobras faces an existential fiscal hole importing at high prices and selling at 60% of it. This is called the defasagem or subsidy gap. The government eventually capitulates — they always do, they just lag. Meanwhile, the BRL devalues because it hurts the fiscal situation, balooning the import bill. Eventually Petrobras aligns gasoline prices to international levels, ethanol then rallies. Until then, Brazilian ethanol and subsidized gasoline gets exported in increasing quantities, through official channels but also the porous Paraguay border. 5/ When domestic gasoline normalises toward world prices, the math inverts overnight. Pump parity makes domestic ethanol suddenly valuable. Mills flip the cane mix lever toward ethanol. Sugar export volumes collapses at the precise moment demand from the middle east is catching up post Ramadan 6/ Turning raw sugar into white sugar requires refineries (Etihad in Iraq is getting sugar through Hormoz, but waiting to see what Al Khaleej and that Saudi "doctor" gets), polypropylene bags (scarce and more expensive) and natural gas (scarce and more expensive) and diesel trucking (scarce and more expensive). You also know what I think about the white sugar premium over raws. 7/ The kickers: we are entering Brazil's pre-harvest window and it has been raining so harvesting pace is slow and crushing favors ethanol. Funds are net short sugar and the momentum has already reverted with upside asymetry. A demand shock into an inelastic supply = price spike. I think this year it will rain Reals on the Brazilian cane industry, and by the look of it, some players can immensely benefit. Party time. youtube.com/watch?v=CCF1_j… Disclaimer : I am rather obviously long sugar and brazilian sugar equities.