Tony Tang

1K posts

Tony Tang

@TTRainmaker

CEO, Founder @inkfinance

California, USA Katılım Ekim 2021

478 Takip Edilen6.1K Takipçiler

现在这些天天比较大模型的 KOL 让我想起当年攒电脑的时候,我们一帮人天天比较各种主板、显示器、CPU、显卡、声卡、机箱电源。除了在人前炫耀,毛意义都没有,但也是真快乐。

中文

@Jingyuan_521 @zarazhangrui 互联网刚兴起的时候也有这种说法。

总之是要警惕那种年龄不大、过得很顺、经历很少的人做出来的那种普世性的判断。

中文

我今天刷到字节AI产品经理张咋啦@zarazhangrui的一条帖子:“人类最有效的合作方式,就是不合作。一个人的end-to-end全权负责,然后和Agents一起工作”。我想到“一人公司”,Peter一个人就搞出了火遍全网的Openclaw,想到我曾在学校和职场中感到的迷茫,想到这2年开始全职做自媒体后,一个人工作时的百分百专注+思考+掌控,开始用AI agent后@StarchildOnX 我从一个周更/月更博主变成了现在的日更博主,和大家聊聊我自己的感想。

中文

@myanTokenGeek words are cheap, why not🤣 everyone wins, including the one that’s beaten into a pulp🤣

English

Thougts:

1) Banks' concern about uneven regulatory requirents is warranted. GENIUS Act designates stablecoins as non-security, but if they bear interests then this designation should be challenged.

2) Banks will still face the threat of balance sheet contraction (and hence the contraction of total credits available in the entire fiat financial system), because

3) Non-yield bearing stablecoins can earn yields when RWAs are prolific on-chain, giving them more utility than just being a super efficient payment vehicle

4) Protocol-issued, RWA-backed, and yield bearing stablecoins now have a better chance to compete with GENIUS-permitted stablecoins.

Shay Boloor@StockSavvyShay

$CRCL falls ~15% after the CLARITY Act deal signals no yield on stablecoin balances by allowing only activity-based rewards. That weakens a key part of the bull case by making USDC harder to evolve from a payments utility into a real store-of-value product.

English

华裔女孩Lucy Guo 拿下全球90后白手起家女首富的头衔,这两天已经刷屏了全网

作为 Scale AI 的联创,踩中AI 时代最刚需的AI数据标准产,她无疑是幸运的

Scale AI 被Meta 以300亿美元估值投资143亿美元后,核心成员 Ahmed Rashad @AhmedZRashad 又继续在这个赛道创立了Perle Labs

他最开始的想法是,当前 AI 数据供应链存在明显缺陷:来源不透明、过程不可追溯,以及大量 AI 生成数据反向进入训练集,形成“AI 训练 AI”的闭环,进而导致模型坍塌(Model Collapse),使模型逐渐偏离真实世界。

在医疗、金融、法律等高风险领域,这种偏差甚至会带来现实决策风险。AI 行业的核心矛盾,正在从“算力与模型能力”转向“数据是否可信”

因此Perle @PerleLabs 目标是构建专业、真实、可信的企业级 & 主权国家 的 AI 数据基础设施,已经服务多家企业级乃至主权级客户

与传统众包标注不同,Perle 构建的是“专家驱动的数据体系”:由医生、律师、语言学家等专业人士完成数据标注,从源头保证质量。

贡献者通过链上信誉体系积累记录,形成长期激励。所有数据可追溯、可审计,确保责任明确。这使其能够服务政府、医疗、国防等对数据容错率极低的场景。

从行业演进来看,AI 正从算力竞争、模型竞争,进入“数据质量竞争”阶段,随着 AI 深度参与现实决策,数据已成为关键基础设施,“谁能提供最可信的数据”,将成为下一阶段的核心竞争力

目前Perle 已完成 1,750万美元融资,目前已被列入 Coinbase 上币路线图,投资方包Framework Ventures、CoinFund 等顶级机构。代币 $PRL 的经济模型已公布和空投注册已开启

Perle Foundation@PerleFDN

$PRL is the native token powering @PerleLabs — the sovereign intelligence data layer for AI. As AI systems move into high-stakes domains like healthcare, robotics, and defense, the integrity, provenance, and accountability of data becomes even more critical. Models can no longer rely on opaque or unverified data pipelines. Perle Labs is building this infrastructure, with $PRL aligning incentives across contributors, enterprises, and the network to support expert-validated, human-driven data at scale. $PRL enables access to the Perle ecosystem, including workflows, tools, and contributor opportunities across high-quality AI data pipelines, while introducing priority positioning across tasks, features, and emerging platform capabilities. By bringing access, incentives, and contribution into one system, $PRL supports the Perle protocol in enabling human-validated data and the infrastructure that makes trustworthy AI possible.

中文

@JingOuyang6 你别徒劳了。无非是想在回国之前企图确保安全。实际没有必要。一则没什么人认识你,也没金币可爆,只要你不在黑名单上,回去就回去嘛,基本上是安全的。二则你好像还是不太了解那个系统,如果你真的在黑名单上,你写文章输诚没有半毛钱保护作用。

中文

《我为什么不再反党,甚至支持共产党?》

最近很多人批评我是大外宣,说我“舔共”。那好,因为我信服岳飞的名言:“大丈夫无一事不可对人言”,我就把这个问题讲清楚,大家来谈个明白,省得以后费事。(注:AI对此文毫无贡献。)

埃里克·霍弗认为,“穷人对周围的世界充满敬畏,所以不欢迎变革……穷人的保守主义与特权者的保守主义一样深刻,前者与后者一样,是维护社会秩序的重要因素”。

亨廷顿也认为,真正的穷人,是没有机会去参政,也没有机会去抗议。

所以,让一个社会保持稳定的办法,一定程度上在于让人民保持贫穷。而这显然不是共产党现在所做的事情,共产党在做的事情恰恰相反:搁置争议,大力维稳,全力发展经济,改善民生。

而历史研究表明:一个社会最不安定的时候,往往是经济发展迅速的时候。因为经济发展增加了经济不平等,经济的不平等容易增加政治的动荡。所以,任何发展中的国家,关键之关键都在于维持一个稳定的政治制度,因为创造政治制度的能力,就是创造公共利益的能力。而制度性利益,包括共产党本身的利益,都是与公共利益是相一致的。

一个软弱的政府——一个缺乏权威的政府——无法履行其职能,在道德意义上是失败的;这种不道德性,与腐败的法官、怯懦的士兵或无知的教师在道德意义上的不道德性并无不同。(《变化社会中的政治秩序》)

所以,我从一个20年前坚决反对共产党的人,变成一个现在坚决支持共产党政府的人。(当然,我不会无条件支持她所有的政策,比如说人权政策。)

但是,这不意味着我会永远支持共产党。我只是认为,目前的高速发展阶段,需要共产党这个高效高能的政府,来保持社会稳定和国家主权的完整。

而且,任何一个政府,都会只有在认为某种自由不会造成危害时,才会容许某种自由(伯林语)。所以,我认为共产党对言论自由的控制,从维持社会稳定和国家安全的角度而言,是可以理解和接受的。

一旦发展进入尾声,比如达到西方发达国家的水平的时候,各种利益的诉求会更加明显,但由于社会整体文明程度提升了,这种利益冲突不再会用野蛮的形式来体现,所以社会的稳定程度和国家的安全程度就高很多,没有政治动荡的风险。

那时候,一党专制必然会结束其历史使命,共产党就会和平地、安全地把最后一棒交出来,交给具备了参政议政能力和民主素养的人民。因为我赞同威尔杜兰特的观点:“民主制度是世界上最困难的政治形式,因为它要求普通公民具备高水平的理性判断、自我约束与政治责任感。”

至于交给谁,什么时候交,这都是历史和天意,我们普通人只要做好自己,上对得起天,下对得起地,中间对得起父母妻儿亲朋就好了。

中文

@jtreble_deriv @michaelxpettis He has shown this number through pretty simple math. you can find out :)

English

@michaelxpettis “My guess is that we won't see meaningful rebalancing, via a redistribution of income in favor of households, either until China is forced into a disruptive rebalancing by debt or external pressures, or until Beijing brings GDP growth targets to below 2-3%.”

👀

English

1/5

SCMP: "Beijing’s forceful campaign to instil a “correct” understanding of tenure performance among party cadres may signal Chinese leaders’ determination to downplay headline growth figures and move away from the “at-all-costs” development model."

sc.mp/1wuah?utm_sour…

English

A country which has written "men are women if they say so" into the law is worried about disinformation.

English

@MattWalshBlog you do speak like a layman, but honest. the thing does NOT understand. it's your understanding about understanding that's fooling you. the thing is amazing indeed, but it doesn't understand anything. trust me on this.

English

Admittedly I’m a layman. I don’t understand how the technology works. But the thing I find most shocking and frankly terrifying about AI, at its current stage of development, is its ability to apparently understand. You can, right now, feed AI a legal contract and it will read the whole thing and spit out a detailed lawyerly analysis in 30 seconds. Even more startling, you can feed it a whole film script and it will read the entire thing and give you creative feedback, even picking up on subtext and themes and individual character beats, and do it all in a minute. It doesn’t even seem possible, but that’s what it can do. That’s the unsettling thing. And the even more unsettling thing is that I don’t think anyone really fully understands exactly how the thing is able to understand.

English

Tony Tang retweetledi

From issuance to syndication,

Ink Finance provides an end-to-end framework for RWA operations. Your legal structure and compliance integrity will be fully reflected on-chain, without writing code.

We will release a series of short videos showing exactly how this flexible and transparent process works, demonstrating our SaaS grade modular RWA infrastructure.

youtu.be/oe8E79JpDHk

YouTube

English

A man has been charged with 10 counts of attempted murder following a mass stabbing on a train in the U.K.

Read more: abcnews.link/XT5j9BP

English

Congratulations, @MandalaChain and @inkfinance team!

We don't deploy for the sake of it. Mandala's broad BD reach combined with INK's deep structuring capabilities and tech infra would allow us to launch some exciting RWA projects on the Mandala chain, including both the institution-rooted and fan-based assets.

Stay tuned...

Mandala@MandalaChain

🚨 Partnership Announcement 🚨 Thrilled to announce we’re partnering with @inkfinance to bring RWA issuance and fund management to the Mandala Chain ecosystem 🤝🏽 Testnet integration is complete ✅ Some major use cases unlocked: tokenized commodities and IP, trade finance, compliant funds, DAO treasury workflows 🏢💰 AMA Coming soon 🎙️ Read more: mandalachain.medium.com/225b2e3bb884

English

@Kathleen_Tyson_ Has any country in the top 17 solved any problems recently?

English

Stunning collapse in the US global reputation from 2024 to 2025!

US falls 18 places, now bracketed between Kuwait and Kazakhstan!

Link below.

English

Tony Tang retweetledi

What's the most fascinating example of mathematics you've seen in nature? ✍️

English

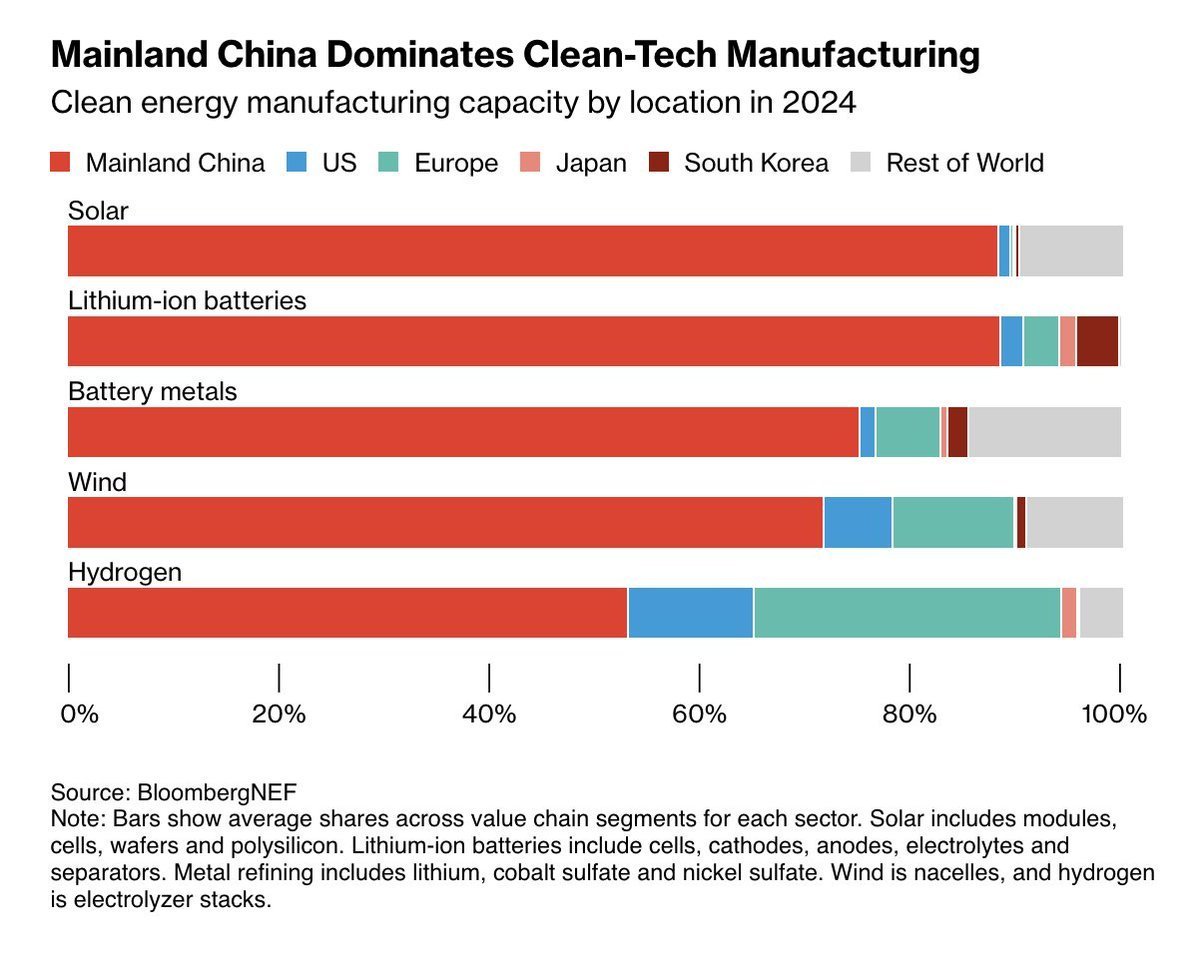

@haugejostein if you don't believe in free lunch, why do you suppose they can do it with such low price? hint: 1) debt that's not repayable; 2) exploitative salary; 3) other forms of pollution that hurts Mother Earth (yes, their factories use coal-fired power).

English

China faces regular accusations of 'flooding' foreign markets with clean energy products, such as solar panels, wind turbines, EVs, and batteries.

China indeed dominates the global market for clean energy products: it manufactures about 80% of the world’s solar panels, 60% of the world’s wind turbines, 70% of the world’s EVs, and 75% of the world’s batteries — all at a lower cost than the West.

In the middle of a climate emergency, this is something we should celebrate rather than demonise.

The accusation oddly seems to be that China is doing too much of something right.

English

美国稀土行业必须要翻越的山口

驱车沿着I-15州际高速公路从洛杉矶前往拉斯维加斯,穿越加州沙漠的尽头,你会翻过克拉克山脉(Clark Mountain Range),进入内华达州。

在经过山口的最高处时,你会看到左手一片灰白色的“梯田”,层层叠叠,醒目异常,那不是农田,而是加州最大的露天稀土矿的矿石堆料区,这里是美国仅存的稀土开采地Mountain Pass矿区。

从山口下来,三座反射烈焰光芒的高塔赫然在目,那是伊万帕太阳能发电站(Ivanpah Solar Electric Generating System)。一旦经过这三个“火炬”,标志着你已跨过州界,进入内华达州的Primm区域。

梯田与光塔,宛如加州与内华达交界处的地标,诉说着两种截然不同的故事。

沙漠中的梯田:Mountain Pass的露天矿

Mountain Pass坐落于圣贝纳迪诺县的最东端,地处加州与内华达交界的高原,也是I-15公路的分水岭。

这个矿区采用阶梯式露天采矿(bench mining)设计,层层开凿,既便于挖掘,又能防止塌方。

1949年发现的这片矿脉,富含镧、铈、镨、钕等轻稀土元素,稀土氧化物(REO)含量高达7%至12%,跻身全球品位最高的稀土矿之一。

冷战时期,Molybdenum Corporation of America在此开采,为导弹制导、电视显像管、雷达和核技术提供关键原料。

那时的Mountain Pass,是高科技的象征,是加州工业荣光的旗帜。

20世纪80年代,环保先锋的加州的法规日趋严格,稀土冶炼产生的放射性钍和氨氮废水处理成本高昂。

1998年,尾矿池泄漏事件成为压垮骆驼的最后一根稻草,政府监管部门勒令停产。到2002年,Molycorp破产,Mountain Pass沦为废弃矿坑。

从“高科技的象征”,它骤然坠为“污染的罪证”。

此后,美国几乎停止稀土冶炼,矿石被运往中国加工,相当于“脏活”外包,中国江西赣州接下了这个“大活”。

在接下来的三十年,中国构建了完整的稀土分离、提纯和磁体制造产业链,南赣州,北包头成为两个世界稀土之都,占据全球90%以上的精炼产能。

美国这边,虽握有矿源,却丧失了技术、工厂和熟练工人,昔日的“稀土强国”,沦为仰赖进口的资源依赖者。

复活的山口:MP Materials的重新崛起

2017年,MP Materials以“Mountain Pass”之名收购矿区并恢复生产。这不仅是一场商业冒险,更是一次战略回归。

美国政府将稀土列为“关键矿产”,动用《国防生产法》第三章资金,支持重建国内供应链。

如今,MP Materials每年生产约4万吨稀土氧化物,恢复了采矿与初步分离能力,但精炼金属和磁体制造仍需海外完成。

为打破瓶颈,公司在德克萨斯州沃斯堡(Fort Worth)兴建磁体工厂,并与通用汽车达成长期供货协议,计划于2025年前实现从矿石到钕铁硼磁体的全链条国产化。

从冷战工业的遗迹,到新能源前哨,Mountain Pass完成了一次命运的轮回。

资本与地缘:股票的热潮

2024年以来,MP Materials的股价如过山车般起伏。随着中美供应链脱钩和稀土出口限制的讨论升温,市场重新审视其战略价值。

2025年秋,德州磁体工厂试生产成功的消息传来,股价数周内飙升超40%。华尔街重拾对它的热情:一个曾因污染被抛弃、如今因战略被追捧的企业。

几十年来,它从“高科技的象征”沦为“环保时代的弃儿”,再摇身一变为“国家安全的宠儿”。

每一次转身,都不是技术突破的功劳,而是政策、资本与观念的风向使然。

在这片沙漠中,两种能源景观并肩而立,相距不足十公里。

伊万帕太阳能发电站是加州环保理想的化身,三座光塔将阳光转化为清洁电力;Mountain Pass则是现实资源的象征,风车、太阳能板和电动车所需的磁体,皆仰赖它脚下的矿土。

两者同属一州,受同一套环保法规约束,却被时代赋予截然不同的命运:一个因“洁净”而受赞颂,一个因“肮脏”而被放逐。

三十年后,旧矿重启,旧污再来,只因“洁净”的绿色梦想离不开“肮脏”的金属支撑。

加州在十公里之内,完成了从理想到悖论的闭环。

这座矿山的故事,是美国现代能源政策的一面镜子,在阳光最炽烈的地方,映照出文明最深的矛盾。

中文

This is really very simple math, but if a reader doesn't have some basic background of economics, the contents in such articles will appear hard to comprehend. The languages used definitely make things worse, as today's content consumers don't have the ability to, or are unwilling to, chew on formal writing.

Michael Pettis@michaelxpettis

These numbers are well-known, but they still shock every time you see them. China's internal imbalances make it such an extreme outlier. This matters to the world because a country's internal imbalances must always be consistent with its external imbalances, and of course its external imbalances must always be consistent with the external imbalances of its trade partners. Because the balance of payments must always balance, both internally and externally, both of these statements are necessarily true. But it doesn't end there. Given the size of the Chinese economy, the extent of its internal imbalances must also be a constraining factor on the internal imbalances of the rest of the world through their impact on their respective external imbalances. This may not necessarily be a bad thing, but it certainly must be understood by anyone who wants to understand other economies. For example, if a group of countries implement policies that force domestic saving to rise above domestic investment, as long as they are able to control their external accounts, and as long as at least some of their trade partners don't, the rest of the world must "choose" to save less than it invests. There are good ways this can happen, and bad ways, but it must happen. Similarly, if a group of countries implement policies that cause their manufacturing to grow faster than their GDP, and their consumption to grow more slowly, as long as they are able to control their external accounts, and as long as at least some of their trade partners don't, the rest of the world must "choose" to have manufacturing grow more slowly than GDP and consumption grow more quickly. Again, there are good ways this can happen, and bad ways, but it must happen. The point is that we live in a highly globalized world in which some countries choose to have more open external accounts, while other countries (more determined to maintain economic sovereignty) choose to have more closed capital accounts. One consequence is that not only do the latter have more control over their domestic economies, but they also exert substantial control over the domestic economies of the former by constraining the range of policies they can pursue. This, Joan Robinson explained, is ultimately unsustainable, and must eventually lead to a breakdown in global trade once the former decide to regain control of their external accounts. As she (and most economists back then) understood, very deep imbalances in more open economies are not the result of "free trade", as must economists believe today, but are rather the result of a trading system in which different major economies choose different levels of trade intervention.

English