Tyler Caldwell

27 posts

ANTHROPIC VALUATION: $965B

WALMART VALUATION: $940B

ANTHROPIC REVENUE: $20B

WALMART REVENUE: $725B

BUT AI IS NOT A BUBBLE, RIGHT?

Kalshi Finance@Kalshi_Finance

JUST IN: Anthropic raises $65B at $965B valuation 70% chance of IPO this year

English

@grant__gregory Preach! Lots of thinking spills in from other asset classes that doesn’t apply to VC.

If everyone has the same info and access, you only create alpha by being non-consensus. Not so in VC. Some of the most consensus bets in VC are money makers bc of access constraint.

English

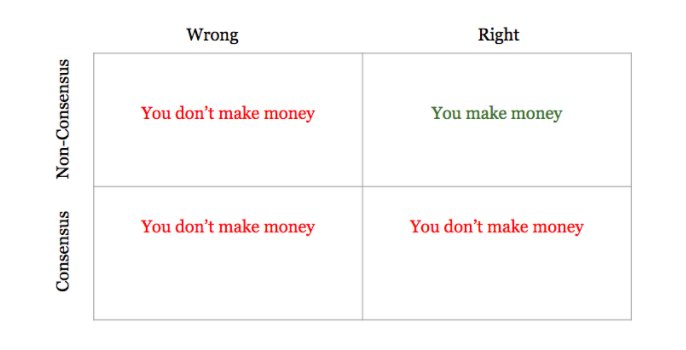

Everyone knows this chart, few people know where it actually came from (not Thiel!)

When it comes to modern venture capital this framework is useless at best and misleading at worst... it comes from credit, after all

ian@IanRountree

English

Some analysis from @StepStoneVC that cuts sample of early stage funds into a 2x2, small vs. large and concentrated vs. diversified.

Large & diversified has highest hit rate of 3x+ TVPI funds (33%), but…

Small & concentrated cohort has highest aggregate TVPI (3.6x total, 6.6x across just the upper quartile funds).

Makes sense, spreading your net = higher chance of some success, but lower ceiling.

English

Early stage VCs should (probably, on average) make more investments.

Lots of objections, some of them very valid. But the general disdain for "spray and pray" is pretty anti-math.

Link to the full argument as laid out by @credistick in following post

English

Tyler Caldwell retweetledi

Some great data in here 👇🏻 A few facts that stood out:

Funds closed in ‘24 were open for 22 months (on avg). In ‘18 this was 14 months

In ‘24, aggregate PE distributions exceeded capital called for the 1st time since ‘15 😳 - a good sign that GPs are finding ways to exit!

StepStone Group@stepstonegroup

We are pleased to share that we partnered with @McKinsey to provide data and insight for their Global Private Markets Report 2025. The report leverages SPI by StepStone’s data and custom analysis, as well as findings from our private equity co-investment GP survey. 📄 Check out McKinsey’s full report: mckinsey.com/industries/pri… 💡 Learn more about SPI by StepStone’s industry-leading data platform here: bit.ly/410K6JH 🔎 Read about our PE co-investment survey findings: bit.ly/3NeBedp #SPIbyStepStone #PrivateEquity

English

Tyler Caldwell retweetledi

Last month, our 2025 Venture & Growth Annual Meeting brought together an incredible group of clients, GPs, CEOs, and friends of the firm for two days of great conversations and meaningful connections.

The conversations covered topics ranging from deep tech and defense tech to the evolving AI landscape and were engaging, insightful, and full of forward-thinking ideas.

A huge thank you to everyone joining us in Boca Raton—your energy and participation make this event special. Check out the highlights from this year’s meeting below! 🎥✨

#STEPVC #VentureCapital #GrowthEquity

English

Data from @StepStoneVC on persistence of returns.

- If a VC’s last fund was 1st quartile, the probability it’s next fund will also be 1st quartile is 42% (vs 25% base rate).

- The probability it’s next fund will be 3rd or 4th quartile is 28% (vs 50% base rate).

The hot hand dynamic is a real thing in VC.

Tyler Caldwell@T_Caldwell

I hear a lot of assumptions about persistence of returns in VC, from both the GP and LP community. How powerful is persistence? @StepStoneVC data on persistence of returns in VC from 1990-2020👇🏻 Question: If a VC’s last fund was upper quartile, how is their next fund likely to perform? Data: Given most recent fund is 1st quartile, probability of next fund finishing…. - 1st quartile ➡️ 42% - 2nd quartile ➡️ 29% - 3rd quartile ➡️ 19% - 4th quartile ➡️ 9% (Margin of error ➡️ +\- 5%) Punchline: Meaningful evidence that returns tend to persist at least to the next fund. Impact is a nice tilt in probabilities (42% chance of a repeat compared to 25% baseline), but not grounds for an automatic re-up as many LPs assume (mostly likely outcome is still failure to hit upper quartile). Persistence should help LPs gain conviction, but still need to do the work. Further Questions: - Do returns continue to persist to the 3rd fund, 4th fund, etc? How long does the hot hand stay hot? - What explains persist of returns to begin with? Network / sourcing advantage? Insight / Information advantage from board responsibilities? Something else? - Why don’t other asset classes demonstrate persistence of returns? - What else?

English

I hear a lot of assumptions about persistence of returns in VC, from both the GP and LP community. How powerful is persistence? @StepStoneVC data on persistence of returns in VC from 1990-2020👇🏻

Question:

If a VC’s last fund was upper quartile, how is their next fund likely to perform?

Data:

Given most recent fund is 1st quartile, probability of next fund finishing….

- 1st quartile ➡️ 42%

- 2nd quartile ➡️ 29%

- 3rd quartile ➡️ 19%

- 4th quartile ➡️ 9%

(Margin of error ➡️ +\- 5%)

Punchline:

Meaningful evidence that returns tend to persist at least to the next fund. Impact is a nice tilt in probabilities (42% chance of a repeat compared to 25% baseline), but not grounds for an automatic re-up as many LPs assume (mostly likely outcome is still failure to hit upper quartile). Persistence should help LPs gain conviction, but still need to do the work.

Further Questions:

- Do returns continue to persist to the 3rd fund, 4th fund, etc? How long does the hot hand stay hot?

- What explains persist of returns to begin with? Network / sourcing advantage? Insight / Information advantage from board responsibilities? Something else?

- Why don’t other asset classes demonstrate persistence of returns?

- What else?

English

@Jeffreyw5000 @StepStoneVC data - only 53% of emerging managers that raised a Fund I in 2019 have survived and since returned to raise a Fund II. Brutal vintage in terms of survivability, but will look like a walk in the park compared to ‘20-21.

English

After speaking with hundreds of LPs and GPs over the past year, it seems that the ratio of allocable LP capital versus the amount of GP mouths to feed is by far the worst ever, which makes this an absolutely brutal fundraising environment for emerging managers.

Reasons are:

-Cambrian explosion of VC funds in the past 10 years means more funds are competing for LP $ than ever before

-<10 megafunds are hoovering up largest-ever % and $ of LP capital

-Over-allocated / illiquid LPs are cutting rather than adding new names.

-QQQ and private credit performance paired with IPO/M&A winter make VC look less appealing by comparison.

NET: extinction level event for sub-scale VC firms. Good luck out there friends :)

English

Great insight from @samirkaji. #11 is especially tricky - the best GPs often hold at a ~30%+ discount to last round price, so their performance can look “meh” relative to benchmarks. Less sophisticated LPs miss this all the time.

samir kaji@Samirkaji

13 things LPs should know about venture capital. 1/ VC is highly cyclical, alternating between long risk-on periods followed by sudden risk-off periods. Trying to time things is a fools errand, which is why consistency across vintages is required. 2)75-90% of VC funds (depending on the cycle) will underperform top quartile lower middle-market PE funds, especially when accounting for illiquidity/risk. 3)Most LPs would achieve better returns investing in established large/mid-cap tier-1 brands rather than trying to pick individual micro funds. The latter requires expertise and TIME 4) Small seed funds consistently make up the majority of the top 10% and bottom 10% of funds in every vintage year. 5)While DPI (Distributions to Paid-In) ultimately matters most, avoid drawing conclusions from funds <6 years old. Our data shows that some top-performing funds actually took longer to achieve their first meaningful DPI. The Carta and AngelList data is valuable, but being surprised by lack of DPI for 2020+ vintage years shows little understanding of the asset class. Also 2017/2018 DPI is indeed poor, but this reflects the challenging exit markets of 2022-2023. Focus on company quality and wait to judge. 6) Recent posts suggesting that $100M-$500M funds are in "no man's land" are both incorrect and correct at the same time. This applies to firms lacking advantages in brand, domain expertise, or network. There's significant value for founders raising Series A from high-quality mid-cap managers who can provide quality senior partner support. 7) While track records and historical performance provide useful context, in VC, backward-looking analysis almost always leads to suboptimal deployment decisions. 8) A recent LI post citing PitchBook benchmarks claimed 11% of sub-$100M funds achieve 5x returns. This is significantly overstated due to survivorship bias and using small samples as a denominator. The figure is closer to ~1-2%. Funds achieving 5x+ DPI are truly rare. 9) VC faces a significant liquidity challenge and needs to mature in developing better liquidity paths. Extended liquidity timelines are increasingly incompatible with viable risk-returns, especially for those who cannot access top managers. 10) Thea ability gap between top and mediocre/poor VCs is enormous and becomes readily apparent to LPs with sufficient experience. However, since VC often represents only 5-10% of an LP's portfolio, many lack the sample size or network access for proper comparison. 11) Track record assessment requires careful analysis of holding values. Managers' holding valuations can inversely correlate with the firm's fundraising risk. I've seen firms that don't worry much about being able to raise typically maintain more conservative valuation policies. LPs must scrutinize the marks of top portfolio companies driving past unrealized performance. 12) For seed funds having a real edge in sourcing & winning deals can> picking ability. Brand/distribution matter. 13/ Every decade, there is a new guard of firms that come in and become dominant long term forces. 2000's, 2010's saw it, and we are already seeing early signs of breakout new firms in the 2020's. There are far more things.

English

We’re now far enough from the pandemic to start seeing its effect on the VC landscape.

2019 was brutal for VCs raising their first fund - just 53% survived to raise a Fund II. Only year worse since 2000 was ‘09. Expecting to see record low survivability in ‘20-21 vintages.

English

Macro factors have a huge impact on survival rates for emerging managers.

@StepStoneVC data: VCs that raised a Fund I in 2019 have a 53% survival rate so far. Huge shakeout in short amount of time. The only vintage more deadly for emerging managers from 2000-2020 was ‘09.

@jason@Jason

The VC business has collapsed — or reverted back to what it was ment to be: a bespoke practice Discuss

English

@thomasschulzz Interesting… you have recent data on all these firms? I’d agree with maybe ~50% of your categorizations, but there are some monsters in Tier 3 you aren’t including.

English

Tier 1:

- Sequoia

- Founders Fund

- A16Z

- YC

Tier 2:

- Benchmark

- General Catalyst

- Khosla

- Lightspeed VP

- Index

- Kleiner Perkins

- Caffeinated Capital

- SV Angel

- Tiger Global

- First Round

- Greenoaks

- Accel

- Bessemer

- Greylock

- USV

- Paradigm

- Homebrew

- Form Cap

- Menlo

- Craft

Tier 3 & beyond:

- Everyone else

Unranked:

- There are some newer unranked funds that have a lot to prove that I wouldn’t include in Tier 3.

Thomas Schulz@thomasschulzz

Never raise money from Tier 3 VCs. Every horror story I hear is from uncalibrated VCs that have no operating experience who think they can tell a founder how to run their company.

English

Headline performance metrics of prior funds for an early stage VC strategy are severely lagging indicators. Mostly useful only for mature funds (7+ years into the fund life cycle)...

However, prior fund portfolios can contain plenty of signals when looking at the calibre of founding teams, early customer adoption, quality of follow-on investors, etc.

Looking under the hood is essential when evaluating VC funds.

Tyler Caldwell@T_Caldwell

@StepStoneVC research on what signals matter most in DD of a VC fund. How important is recent fund performance? Probability of finishing top quartile in yr 10, given the fund was top quartile in yr X 👇🏻 Year 1 ➡️ 30% Year 2 ➡️ 36% Year 3 ➡️ 43% Year 4 ➡️ 46% Year 5 ➡️ 48% Punchline: It’s not nothing, but not the signal you might expect. LPs, dig deeper than headline performance.

English

@StepStoneVC research on what signals matter most in DD of a VC fund.

How important is recent fund performance? Probability of finishing top quartile in yr 10, given the fund was top quartile in yr X 👇🏻

Year 1 ➡️ 30%

Year 2 ➡️ 36%

Year 3 ➡️ 43%

Year 4 ➡️ 46%

Year 5 ➡️ 48%

Punchline: It’s not nothing, but not the signal you might expect. LPs, dig deeper than headline performance.

English

@MeghanKReynolds @stepstonegroup The natural question is “how did they do it?” All three of those $2bn+ VC funds had at least 1-2 fund returners off big checks, still following a power law distribution. Rare and remarkable for GPs to have that kind of access at scale.

English

Heard from LPs this week: A data present 🎁

So many convos in ‘24 around fund math. Can a big fund deliver big returns? So, I posed the question to my VC data guru @T_Caldwell from @stepstonegroup

How many VC Funds over $2B have delivered over 3x Net TVPI or DPI?

The Punchline:

Only 3 out of 72 $2bn+ VC Funds have crossed 3x TVPI and only 1 has crossed 3x DPI (1%)

(All of those funds are pre-2020, which makes sense these are funds that have had a chance to mature)

We then looked at all PE, Growth VC Funds… to apply the same question to big funds in general, not just VC

The Punchline:

Only 15 out of 648 (2%) of $2bn+ Funds have crossed 3x TVPI and only 5 has crossed 3x DPI (1%)

I think a better understanding of this data will reset expectations for VC portfolios. Big funds expected to deliver consistency. Small funds expected to deliver upside.

English

English

English

Tyler Caldwell retweetledi

Heard from VC LPs this week:

For our AGM, we asked @StepStoneVC (best VC data) to analyze return distribution in VC. @fredwilson @pmarca have discussed; this is 25+ yrs of data. TLDR: Even Top 5% underperform underwriting on ~3/4 of deals. Great = $$ in big winners #powerlaw

English

This is a good question -- what goes into a good go-to-market strategy?

Especially at pre-seed when there's nothing there?

Read on >>

Lolita Taub@lolitataub

🤔 Asking for a founder: what goes into a good gtm strategy?

English

@djrosent Interesting that $SQ is buying an audio media company while Jack’s other company, $TWTR, is making big moves to monetize the creator economy. The only way I can make sense of the acquisition is to assume they’re related to the same strategy.

English