Yue retweetledi

Could SK Square be a 10x stock?

I believe SK Square (KRX: 402340) could be one of the craziest risk/reward opportunities in the market right now!

Please read the full post to understand all parts of the idea here, there are many important factors and I want you to understand all the opportunities and risks fully.

🧠 THE THESIS

Yesterday’s Big Tech earnings (once again) confirmed the AI capex cycle is not just NOT slowing down, it's actually accelerating.

$GOOGL, $MSFT, $AMZN and $META all showed the same thing:

AI adoption is scaling ✅

AI cloud demand is exploding ✅

High-ROI enterprise use cases are emerging ✅

Capex is going up, even above (high) estimates ✅

I think it's quite clear that all Big Tech players see winning in AI as essential to have a future.

The alternative is to get disrupted and left behind forever.

Knowing that, I believe smart investors should ask a simple question:

Where does all that money go?

A huge part goes to companies like $NVDA, $AMD and $AVGO making (custom) chips.

But directly or indirectly, a huge part of that spending then flows into the HBM providers and there are only 3 that truly matter:

SK Hynix (KRX: 000660), Samsung (KRX: 005930) and Micron $MU.

These companies are printing cash. TODAY. If AI demand continues, they may keep printing cash through 2030 and potentially beyond.

The cleanest pure-play exposure to HBM is SK Hynix with ~60% market share.

SK Hynix looks incredibly undervalued today if you believe this is not just a short-term memory cycle already at peak earnings.

Bears compare this to the fiber bubble and say we're at the peak.

I think the comparison is simply wrong and we don't have to guess to know that.

Back then, fiber supply was built decades ahead of demand.

Today, the AI supply chain is still severely supply constrained. HBM capacity is tight, leading-edge packaging is constrained, power is constrained, and many critical parts of the infrastructure stack are sold out years in advance.

All the AI Clouds are sold out months in advance.

Fiber = Supply was decades ahead of demand.

AI = Demand is years ahead of supply and the gap likely increases over time, because digital demand outscales physical infra growth massively.

So what if there were a way to not only own SK Hynix, but at a massive discount on top of SKH already being a great investment?

Meet SK Square.

SK Square owns ~20% of SK Hynix, the current king of HBM and one of the most important companies in the AI infrastructure stack.

But you are not paying the full price.

You are buying it at a large ~40% holding-company discount, just as Hynix profits may be entering a historic AI-driven upcycle!

That discount is coming down fast. This is happeening NOW! See image below. In the last year SK Hynix went up 650%, but SK Square went up 846%! I expect the discount to decrease to ~30%.

⚙️ THE TRIPLE LEVER

Your potential return is driven by three things happening at once:

1. Earnings growth

Hynix profits scale as HBM becomes one of the key bottlenecks of AI for years to come.

2. Multiple expansion

The market stops valuing Hynix like a cyclical memory company and starts valuing it more like strategic AI infrastructure (supercycle over a 5+ years). HBM is increasingly being sold through multi-year, customer-committed supply agreements, not purely spot/cyclical memory pricing!

3. Discount compression

SK Square’s holding-company discount shrinks as they buy back and cancel shares.

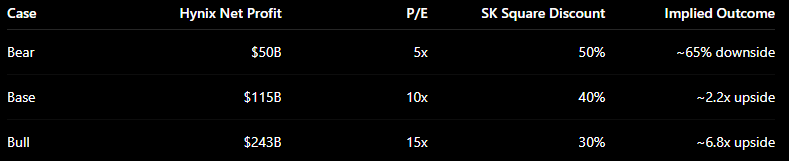

End of 2027 bear-, base- and bull-case

-> see 2. image below for the table view

To estimate 2027 SK Hynix profit, I use the low, midpoint and high-end analyst scenarios.

Today SK Hynix trades at a ~21 P/E ratio. For 2027 We'll be very conservative and take 5 as the bear case, 10 as the base case and 15 as the bull case. We're being very conservative here, because the market might keep thinking this is a cycle top and might take time to understand it's a new paradigm.

For the holding discount we assume it actually increases to 50% in a bear case, stays at the current 40% in the base case and decreases to 30% in the bull case. I think 30-40% is a realistic range, so we're also being quite conservative here.

This means we'd get a -65% downside in the bear case, but a 2.2x - 6.8x upside in the base to bull case, which I consider realistic (by end of 2027)!

Crazy risk-reward.

🚀 EXTREME UPSIDE CASE (10x)

If Hynix ever gets valued closer to a true AI infrastructure bottleneck at something like 20x earnings, SK Square could become a ~10x outcome.

Not my assumption here, just want to point it out. As I explain in almost all of my posts, the human mind fundamentally doesn't understand exponentials. AI growth is another one of those. AI is slowly eating the entire global Economy. If you believe HBM is a critical layer and true bottleneck of AI you understand that future growth potential is VERY big. It's hard to imagine how big.

🇰🇷 WHY NOW?

First of all you can look at the performance of SK Hynix and SK Square to see that the re-rating of both is already in full force. But I do see a couple of further reasons why right now is a great moment in time.

1. Buybacks

SK Square is using Hynix dividends to buy back and cancel its own shares.

That means every cancelled share increases remaining shareholders’ claim on the Hynix stake.

They want to get the discount down to 30%.

2. Korea discount compression

Governance reform, shareholder returns, and Korea’s Value-Up program are all pushing the market in the same direction: less empire-building, more capital return, more focus on shareholder value. That is a reason why the Korean market is increasingly more attractive for investors and is seeing such an insane re-rate. This is a long-term trend, not just something that happened in 2025 and 2026! This will happen over many years to come.

3. Potential U.S. listing

Reuters reported that SK Hynix is considering a confidential U.S. listing in H2 2026. If that happens, it could make Hynix easier for global investors to own and compare directly against U.S.-listed semiconductor peers. $AMD trades at 129 x PE, $NVDA at 42 x PE.

If you look at SK Hynis you will see they have fantastic growth, a very strong moat and insanely attractive margins. This is not a speculative company that deserves a PE discount. If anything it deserves a premium to many overhyped Semi stocks where much of the valuation is pure expected future growth. SK Hynix prints money this year and next year and the year after. We know that.

4. Global AI rotation

IBKR and I assume soon other brokers are now allowing investors to directly buy Korean stocks. But the bigger point is institutional: global funds are looking for the next AI winner that is not already priced at 40x earnings.

SK Hynix is the obvious and confirmed winner.

SK Square is the discounted version.

⚠️ THE RISK

This is not a 100% guaranteed free money stock.

Maybe I'm just straight up wrong. If the AI buildout slows, suddenly out of the blue big tech massively lowers capex, HBM pricing weakens, Samsung or Micron leap ahead, or the market refuses to re-rate Korean semis, SK Square can obviously go down. Maybe Korea suddenly adds horrible laws for international investors or something like that happens.

There are always unknown unknowns.

The downside exists.

My excited about this stock mainly stems from my view that the upside is just more likely and... well, massive!

HOW YOU CAN PLAY THIS

1. If you have IBKR, you can just buy SK Square

(KRX: 402340)

2. If you don't want the levered version or don't feel comfortable with the holding structure, you can just buy SK Hynix (KRX: 000660) which I think is still a crazy good opportunity.

3. If you don't have IBKR or just want to invest in things that are listed in the US, you can just buy $DRAM which is a great ETF for HBM. Then you'll still own like 25% SK Hynix, but also the other HBM players like $MU and Samsung (among a few smaller positions like $SNDK).

Personally I made SK Square a fat position today. Getting the chance to buy SK Hynix basically at 2-3 x forward P/E just sounds like the bargain of a century to me.

English