FollowTheFilings@fdzmurillo

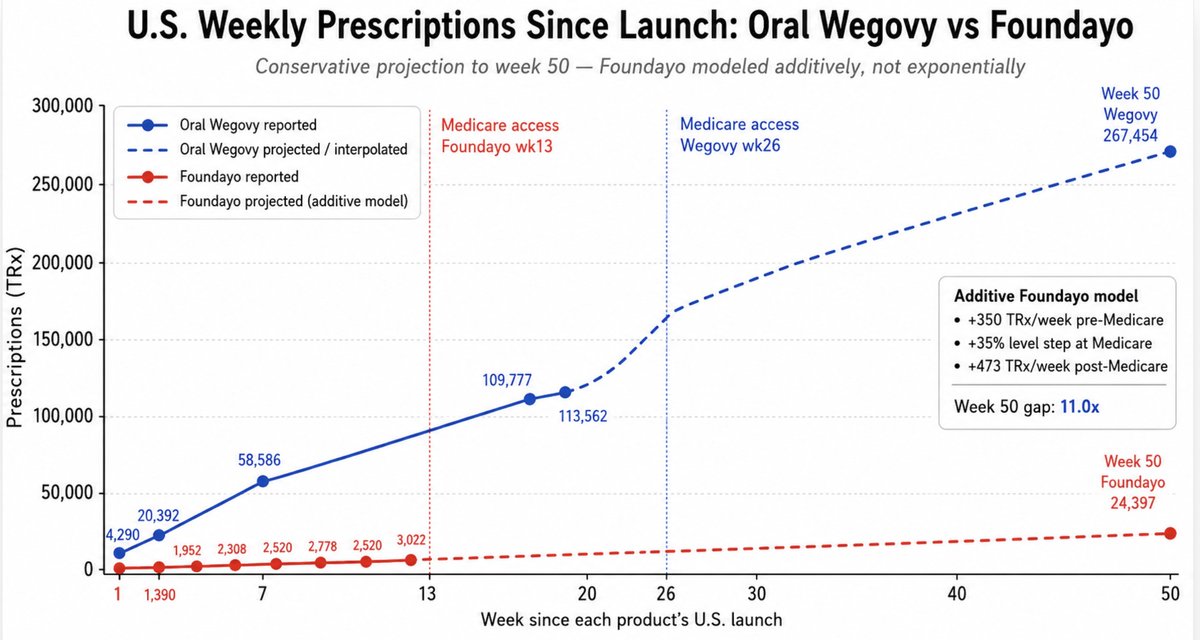

The question isn't whether $NVO deserves credit for Oral Wegovy. It obviously does. 200K scripts/week. 21.6% in responders. Strongest pharma launch in history.

The question is why the credit is taking so long to arrive.

The answer isn't complicated. It's portfolio math.

Major institutions loaded up on $LLY between 2023-2024 at $500-900. It became their flagship healthcare position. A top-10 holding in hundreds of funds. Conference presentations built around it. Client letters praising the position.

$LLY is now at $966 with 35x forward earnings and an oral pill doing 10,248 scripts in week 5.

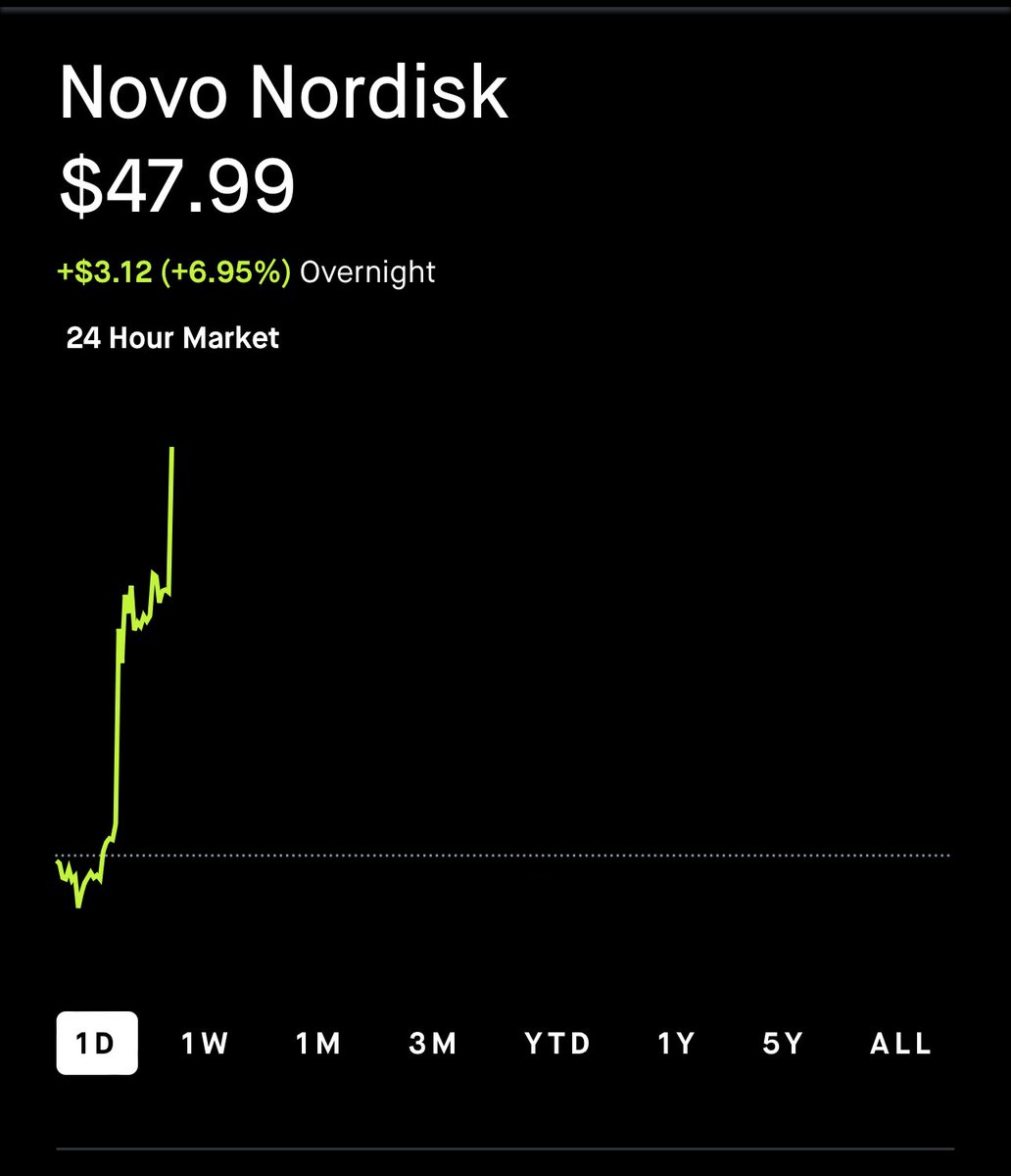

$NVO is at $46 with 12x forward earnings and an oral pill doing 200,000+ scripts per week.

The data says rotate. The portfolio says you can't.

Because selling a $700B position moves the market. You can't unwind $LLY quietly. Every block trade signals to the market that smart money is leaving. The stock drops. Your remaining position loses value. Your clients ask questions.

So instead you hold $LLY, maintain "neutral" on $NVO, and wait for a moment when you can rotate without destroying your own position.

That's not analysis. That's asset management.

The rotation will happen. It always does. The only question is whether it happens gradually or all at once.

And the longer they wait, the more violent the repricing.

$NVO $LLY $VKTX