K0N2TI

216 posts

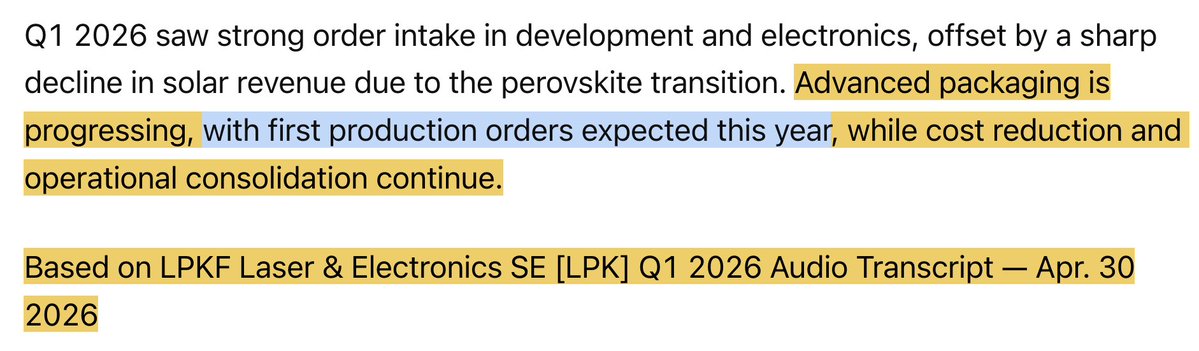

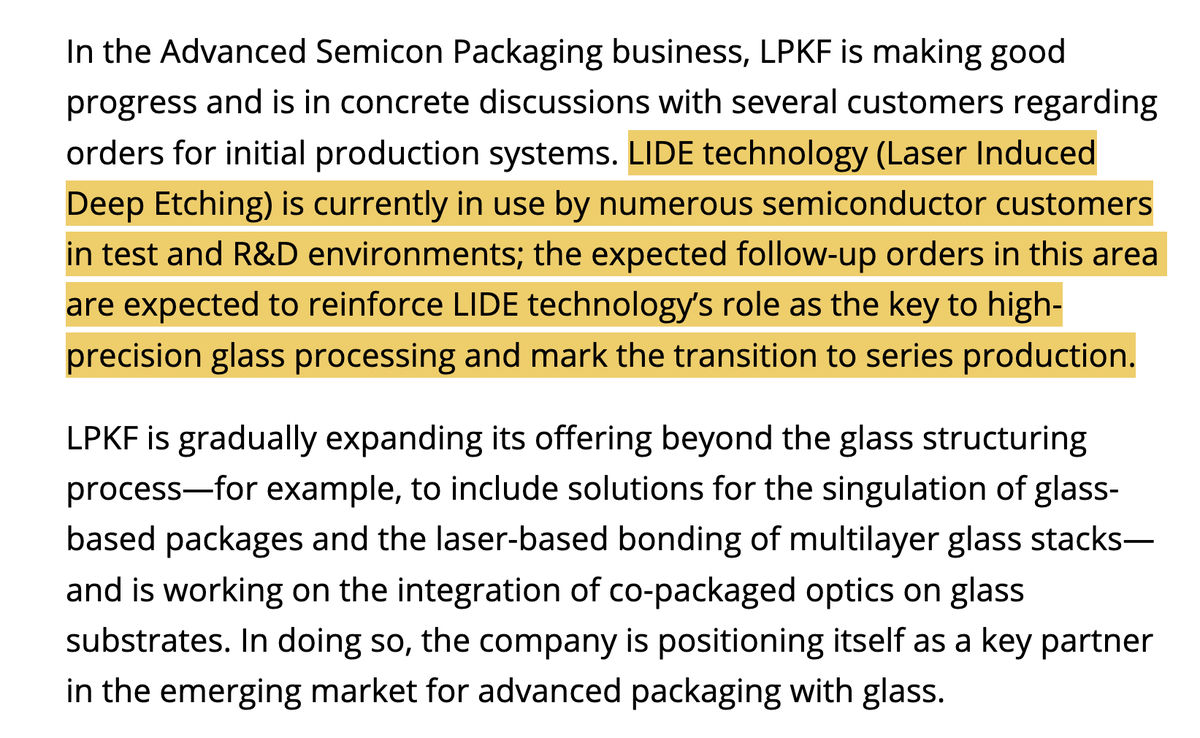

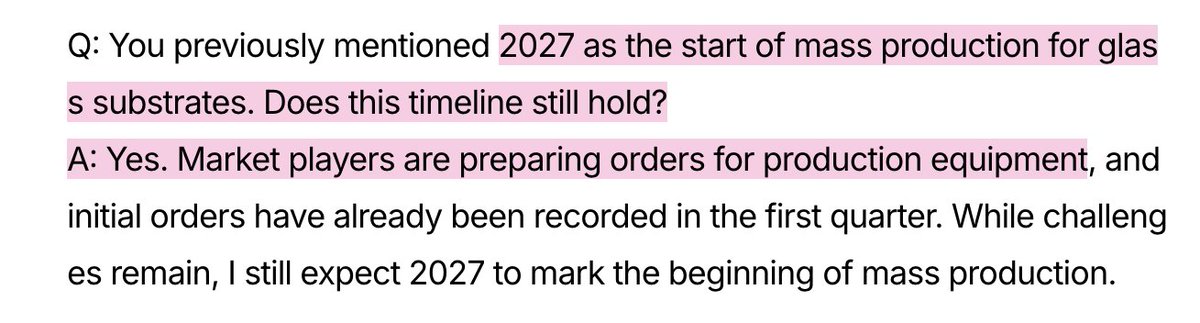

$LPK / $LPKFF earnings are out. Seeing a lot of very dumb commentary on X. If you're wondering how to analyze qualification-cycle players, it's the same as $AEHR. Nobody cares about current earnings unless there's something extremely bad. If your revenue declines -8M euros before any volume ramp, it doesn't mean anything. The only reason why LPKF is a long anyway is 2027 LIDE glass core substrate mass production. Main thing to look at is earnings call in 2 hours not current financials and indication of high volume production + customers. People made this same mistake with $AEHR selling off on previous financials instead of listening to the call.

Ended up buying 75 more shares this morning of Nynomic $M7U Behind this name lies LayTec, a great player for in-situ metrology for MOCVD reactors (the same reactors used to manufacture the InP lasers that power all AI data centers) 130m market cap.