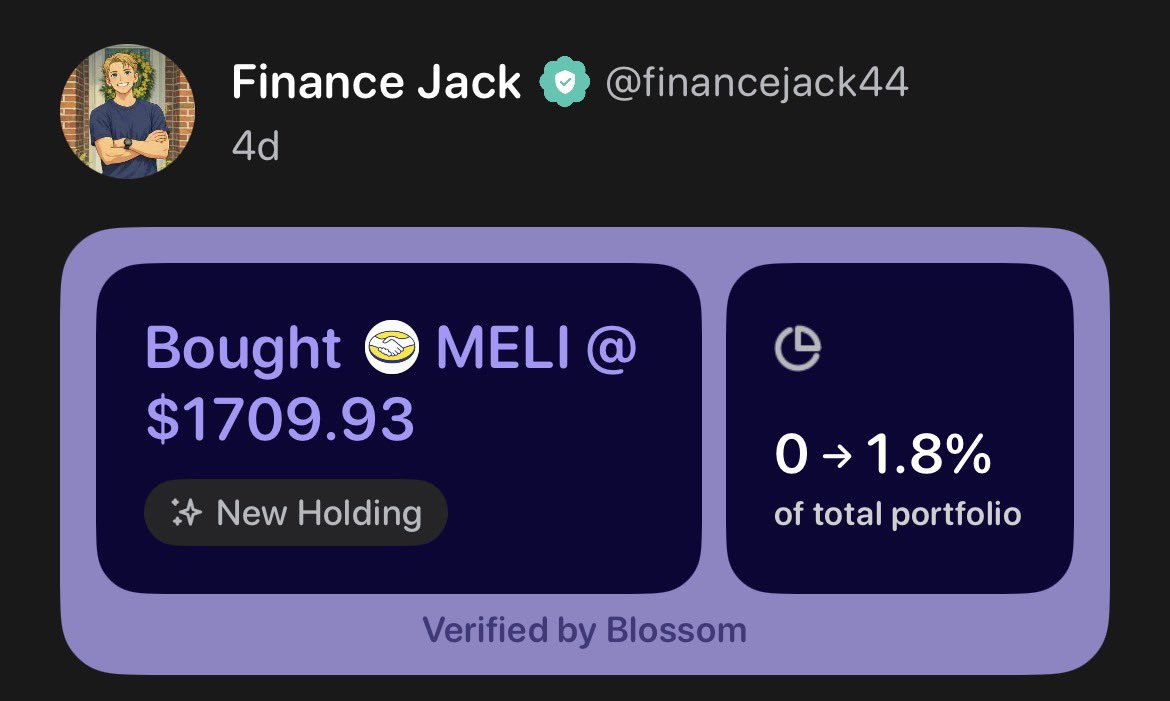

Rose Celine Investments 🌹@realroseceline

I have been investing in $MELI for almost 15 years. That is almost 2/3 of the company’s existence. I have watched this business go from a small few billion dollar company into one of the most important platforms in Latin America, and through all those years the narrative was almost always the same. Competition was coming. Some new heavily funded company was going to destroy them. Some giant was going to overpower them. Yet somehow through discipline, execution, frugality, and an elite culture, $MELI just kept winning.

What always stood out to me was that they rarely behaved like a reckless growth company. They did not constantly dilute shareholders. They did not load the balance sheet with insane debt. They did not chase every shiny object or light billions on fire with dumb experiments that never worked. They executed carefully, maintained an incredibly stable leadership culture, and kept building piece by piece while other companies constantly changed direction or management teams.

Then around 2018 they made one of the boldest transitions I have ever seen from a large public company. They realized the old marketplace and auction style model was not enough and they essentially rebuilt the company around logistics, fulfillment, payments, and infrastructure. Think about how crazy that really was. Latin America is an incredibly difficult region logistically, financially, politically, and operationally. Most companies would fail attempting something like that even with unlimited capital.

What amazes me is they completely repositioned the business from a relatively asset light marketplace model into a much more infrastructure heavy ecosystem without missing a beat. Most companies cannot reinvent themselves like that once they reach scale. $MELI did it while continuing to grow rapidly. That tells you something important about the culture and management quality behind this business.

I also think many people still misunderstand what $MELI actually is. They still think of it primarily as an ecommerce company. I increasingly think ecommerce is almost the bait. Underneath it they are quietly building the infrastructure of commerce and financial services across Latin America.

The flywheel is beautiful, Pago increases checkout conversion and trust. Logistics improves delivery speed and reliability. Credit helps merchants buy inventory and helps consumers spend more inside the ecosystem. Advertising monetizes attention. Fulfillment improves consistency and customer satisfaction. Scale lowers shipping costs. Lower shipping costs improve frequency and conversion. More buyers attract more sellers. More sellers improve selection. The entire ecosystem reinforces itself.

People still debate Pago, ecommerce, credit, logistics, and ads as if they are separate businesses. I increasingly think that misses the point entirely. The value comes from how every layer strengthens every other layer. The ecosystem itself is becoming the moat.

That is what makes the business so dangerous competitively. The moat is no longer one thing. It is the interaction between all the things. Every year the ecosystem becomes more integrated, more efficient, and more embedded into the daily economic life of consumers and merchants across Latin America.

And what makes this even harder to replicate is that Latin America is not an easy region to operate in. Payments are fragmented, infrastructure is weaker, fraud risks are higher. Inflation and currency volatility exist, regulations vary country by country and logistics are far more difficult than most American investors realize. Ironically, those difficulties become advantages for $MELI that successfully builds the network first because the operational complexity itself becomes part of the moat.

1/👇