Sabitlenmiş Tweet

New blog post:

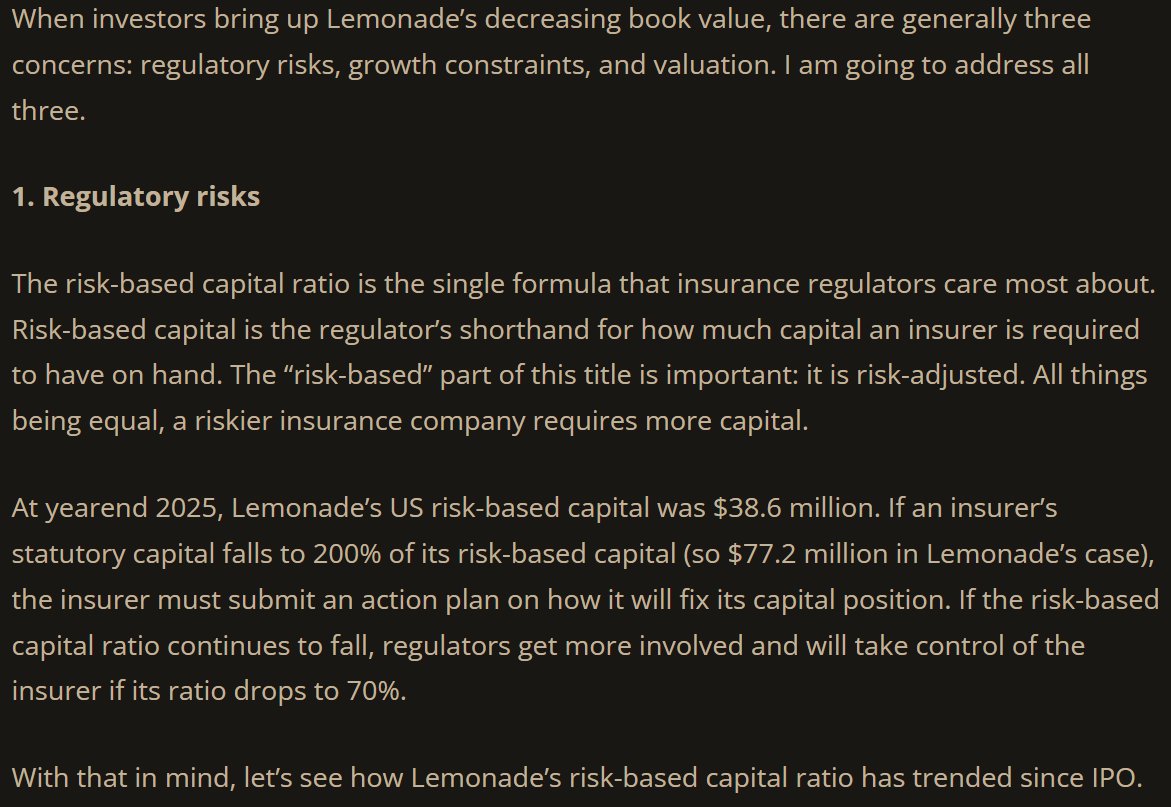

Lemonade’s Book Value: Regulatory Risks, Growth Constraints, and Valuation

(link in bio and next tweet)

$LMND

English

Travis Wiedower

1.8K posts

@TravisWiedower

Optimist, investor. Seeking the forest through the trees.