@YourShami Sir, Any idea. Why this stock falling in last two sessions??

English

TrendSpy

247 posts

@TrendSensor

Passionate equity swing trader and investor, dedicated to maximizing opportunities. 📈💼 Macro enthusiast and diligent follower of market trends.

Jeena Sikho Lifecare Ltd #JSLL What the market is missing ? ① OTC Optionality — Under-modelled Street expectations are already moving towards ~250 Cr. OTC potential by FY28, but the actual optionality can be significantly larger. The company has rapidly expanded distribution, entered new topical OTC categories, and is building a portfolio with structurally better margins compared to prescription products. If execution continues at the current pace, OTC itself can become a major standalone value creator over the next few years. ━━━━━━━━━━━━━━ ② Capital-Light Diagnostics #Chandan_Diagnostics The diagnostics business has the potential to create a ~50 Cr. annual revenue stream with almost zero incremental capex. Since the ecosystem, lab partnerships, and collection infrastructure are already in place, scaling becomes highly efficient from here. This is the kind of expansion that improves operating leverage without putting pressure on the balance sheet. ━━━━━━━━━━━━━━ ③ Insurance Tailwind — Silent Re-rating Trigger A structural shift is happening in reimbursement behaviour. Treatments and day-care procedures that were previously ignored are now increasingly getting insurance acceptance. This improves affordability for patients, increases treatment continuity, and can meaningfully improve demand visibility. Markets are still underestimating how powerful this change can become over time. ━━━━━━━━━━━━━━ ④ Governance Upgrade Statutory auditor Walker Chandiok (GT, Big 5), internal auditor Forvis Mazars (World #7), ERP migrated to Oracle, CRM live on Salesforce. In a sector rife with unorganised family-run clinics, this is a material re-rating trigger as institutional allocators have historically discounted the category. ━━━━━━━━━━━━━━ ⑤ UAE Insurance Expansion The company’s positioning in UAE creates access to a premium-paying patient base with better realization and higher ARPU. Insurance-backed acceptance of alternative medicine is improving steadily, which opens a much larger monetisation opportunity. This international optionality is still not fully reflected in market expectations. Some Key Triggers: ① Entero distribution partnership. Exclusive Ayurveda distribution tie-up with Entero Healthcare (Jan 2026). Opens up 1.25 lakh chemist network nationwide. Instant national footprint that would have cost JSLL 5 years and ₹200 Cr+ to build. Revenue potential: ₹150-300 Cr in FY27 if even 20% of 16 SKUs achieve meaningful retail velocity. Entero's track record with Emami and similar brands is the sanity check. ② Bed capacity scale-up to 5,800. Current: 2,850 built / 2,290 operational. Target: 5,800 beds by FY28 across owned + franchisee + college-partnership models. Capex-light (₹34 lakh/bed vs allopathy's ₹70L-1Cr). If mature-cohort occupancy of 80% holds, 5,800 beds at ₹8,500 ARPOB generates ~₹1,440 Cr service revenue alone — 10x current. Plus medicine cross-sell follows proportionately. Disc: Info for educations. @manikanth2304 @LearningEleven if you are also tracking this company, please share the key points of your thesis in case I have missed anything here.

GNG Electronics Ltd Global memory chip shortage. Clear beneficiary: #EBGNG. Margins currently at 8–9%, but the company now expects them to cross 11%. Very interesting insights around inventory. You can see why GNG is set to be a direct beneficiary.

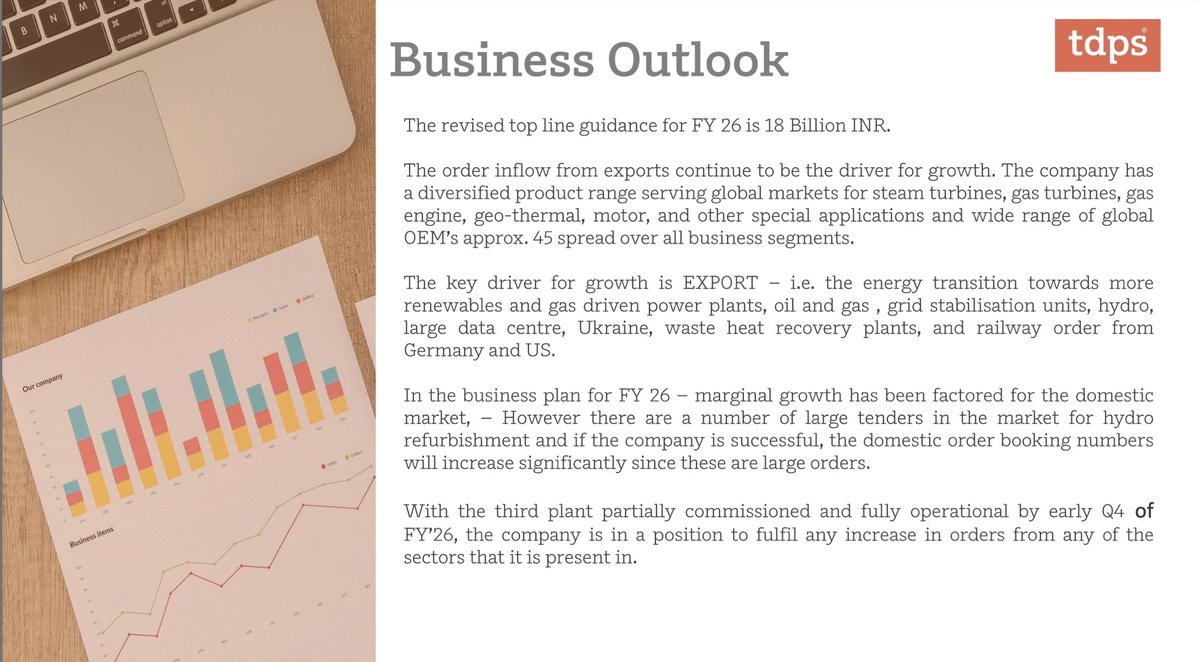

TD Power Systems Ltd - Earning outs for Q3FY26. Order book is growing, margins are stable, and FY26 guidance remains unchanged, so the overall story is on the right track. I thought margins would face some pressure this quarter due to the hike in commodity prices, but that view was proven wrong. The company maintained an 18% OPM, which shows that strong businesses can effectively pass on higher costs to customers. Company stick to the guidance for FY26 and the extended guidance for FY27. For 1800cr guidance . To achieve this, the coming quarter needs to deliver 533cr, which represents a 20% QoQ.. Is this possible? Yes, it is. The reason is that the capex becomes operational in Q3 in multiple phases, which should comfortably contribute to the required 20% growth. Order book stands 1845cr and this quarter growth 61% ( 656cr vs 407cr), This is excellent . I remember, last concall they said, will add 550cr orderbook each quarter, done better. Do not compare Q3 with the previous quarter, as exports in this season are usually lower than in the last quarter. lets see, what management will tell us in Concall.

Vintage Coffee & Beverages Ltd Zero U.S. exports combined with currency appreciation make this a good time to reassess the business.

I met many people and had several investment discussions. One common pattern stood out. Something that is completely within their control. Most of them do not limit their losses. Instead, they limit their profits to 5–10% and justify holding on to losses of 30% or more, believing that the stock will reverse once the market stabilizes and turns around because it is a “quality” stock and they spend 1-2 hours daily tracking the market and market news.

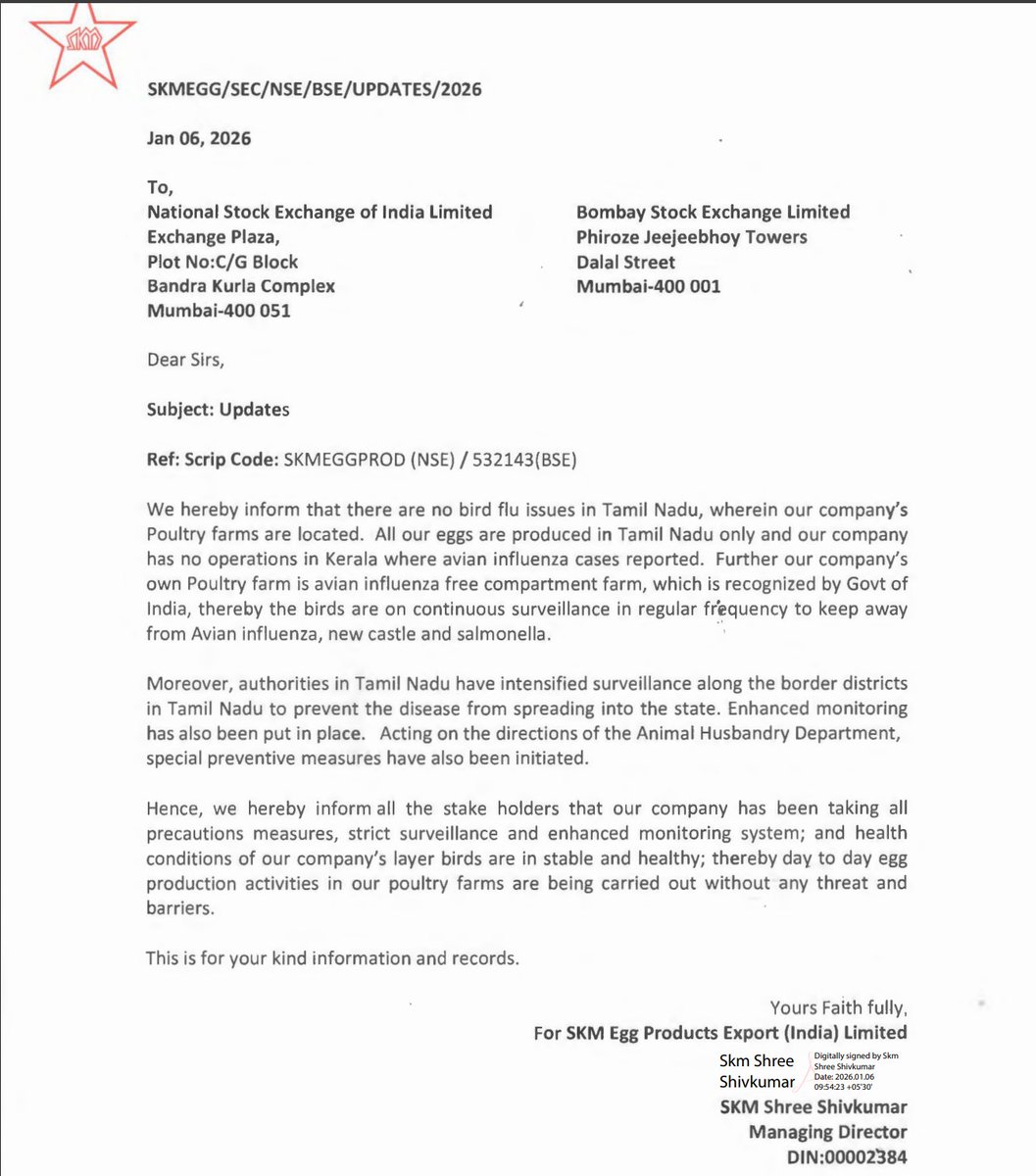

SKM Egg Products & Ovobel Foods Ltd Risk: There has been news of a bird flu outbreak in a district of Kerala, where authorities have culled around 30,000 chickens. If the outbreak spreads to other states like Tamil Nadu and Karnataka, it could have a significant impact on production for these companies. This is an important risk to monitor, and I am sharing this purely for awareness. If this risk starts to play out, the situation could become challenging. You may have also noticed that egg prices have been rising recently, mainly due to a supply & demand mismatch. Egg prices are rising because supply is tight. If bird flu spreads, production may fall further, which can push prices higher. Keep this risk–reward in mind Disc: No buy and sell recomm. DYODD. ndtv.com/health/bird-fl…

Expecting a good quarterly update for #Q3FY26 from Jewellery companies Shanti Gold Utssav CZ PN Gadgil Jewellers Kalyan Jewellers Titan Company Value Retail: Q3 might be weaker vs Q2 on the growth front as Dussehra was preponed to Q2 this year vs Q3 last year That should have some impact #V2Retail #BaazarStyle Sai Silk Kalamandir #SaiSilk Expecting tepid Q3 Might be the weakest of the last 6-8 qtrs 9M should still look good Q3 can be weakish Won't be surprised if there is some degrowth as well for Q3

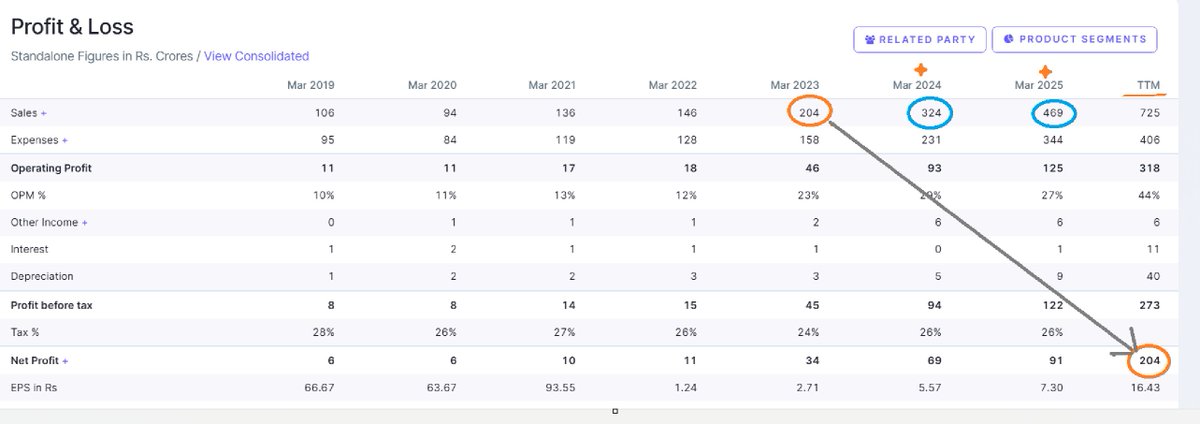

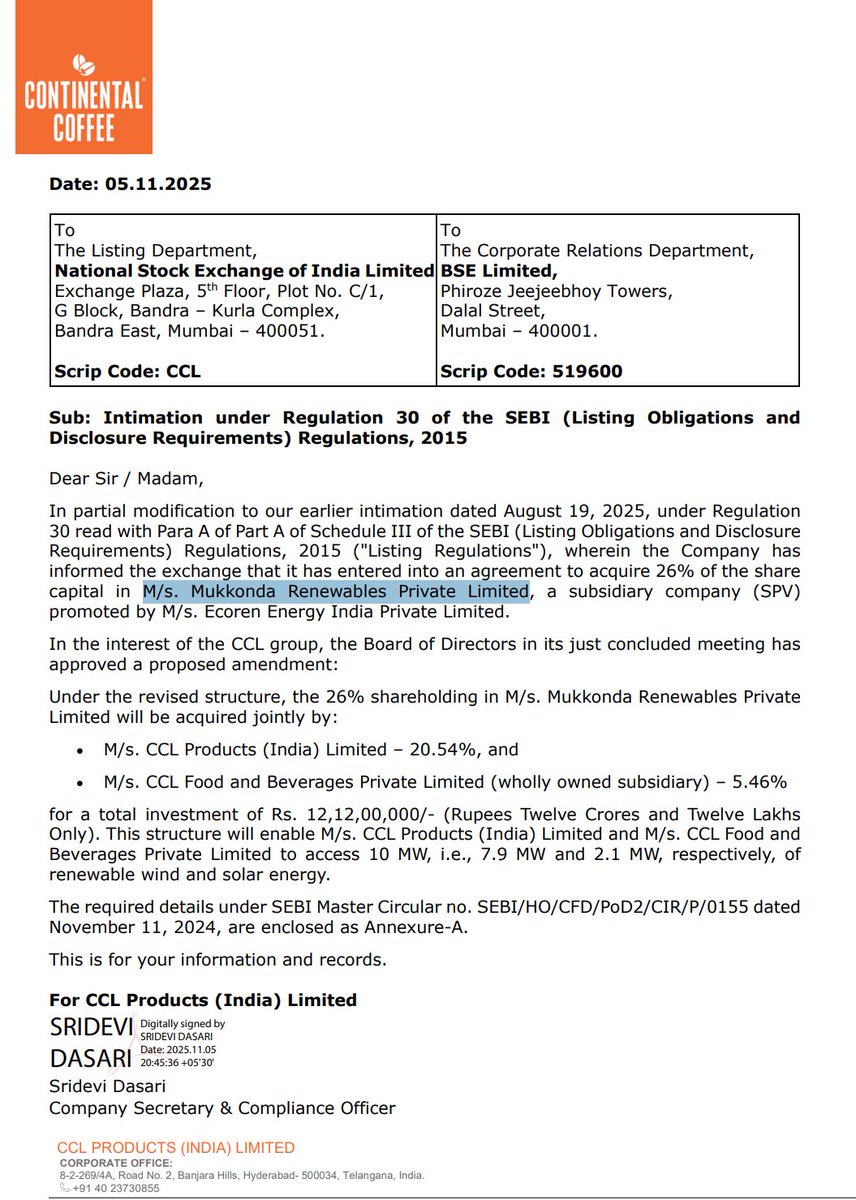

CCL Products - Q2FY26 - Excellent Numbers All the catalyst points are discussed here. OPM 17.5% vs 15.1% ( QoQ) and All time high topline. x.com/YourShami/stat…

Interarch Building Solutions Ltd Last month data points are connecting positively ( just observations) Steel Price Volatility: Steel accounts for ~65% of product cost; margins are highly sensitive to raw material price swings. Operational Costs: Conversion costs (engineering, manufacturing, paint) add ~15% and can fluctuate with project mix. Volume-Driven Margins: Profitability depends more on tonnage sold than revenue, making margins vulnerable to market price changes. Risk Mitigation: Mix of fixed-price and variable-price contracts to manage steel price risk. Maintains 2 months of steel inventory plus 2 months of orders in the pipeline at fixed prices. Techno-FUNDA: -New Capex live -WPI Steel str not much volatility in past couple months. -Chart taking support at 100DMA -New MF entered in August. Note: I am not 100% sure if the WPI price for 'Steel structures' aligns with Interarch. If anyone is closely tracking, please share your notes related to finished goods

Post Results - CCL Products Management talk! youtube.com/watch?v=Kx4KEU…

Hariom Pipe Industries Ltd provided clarity on its MoU at the recent Arihant Capital Conference. Capex & Expansion:A major expansion initiative is the MoU with the Maharashtra government to establish a 1.5 MTPA integrated steel plant in Kurl. The seven-year phased project will focus on engineering and value-added products like galvanized, color-coated, and CR sheets for the auto and light engineering sectors. Funding will align with cash flows and balance sheet strength, with detailed planning in a DPR. Some key interesting key notes👇

#RRKABEL - 🏆🔥 Excellent Q2 Results - Just Out - 2 minutes ago Link - bseindia.com/xml-data/corpf… #Q2Results #Q2FY26 #StockMarket #stockmarketsindia #StockMarketUpdate #stocksinnews

Astra Microwave Products Ltd #ASTRAMICRO JV with Rafael Israel: 50:50 JV producing Software Defined Radios; called a “hidden gem.” Expected to secure $100M+ orders this year, with 35% flowing to Astra. Profitable and strategically significant. Order Book: Current ~2,230Cr guidance for 1,300–1,400Cr new orders. A large BEL order (1500–1600Cr) could take it above 3000Cr+ Atim Kabra – Director of Astra Microwave, advises viewing the defense industry in “stacks of 2 to 3 years,” expecting significant, irreversible incremental improvements and a steady progression from one capability set to another. JV Subsidiary company website: astrafaelcomsys.com Key things- have to notice? Rafale ≠ Rafael Rafale (France) → Fighter jets by Dassault Aviation Rafael (Israel) → Defense systems, missiles, radars Astra Rafael Comsys is tied to Rafael (Israel), not to Rafale jets. BEL- Orders related and other Catalysts are discussed in below threads. Disc: No buy and sell.