Sabitlenmiş Tweet

Ubbe

2.9K posts

Ubbe

@UbbeInvest

Pragmatisk aktienörd (svenska microcaps) och probability junkie inom filosofi och finans. CEO @financelab_SE https://t.co/hZMmTJxif4

Stockholm, Sverige Katılım Kasım 2016

490 Takip Edilen2.6K Takipçiler

I agree it's life-changing. I've seen it happened to other young investors and traders who strike gold. Those who don't know what to do when it happens.

Instant riches does that to some people, it replaces your brain with a greedy engine wanting more and disconnecting from reality. Some don't even realize part of their profits as it stacks up, simply locked in and blinded by their new immortal ways of life.

So yeah. It's life-changing because you will learn the best lesson of your life after the unrealized gains is back at where you started.. all wrapped up in a single beautiful word: "shit".

English

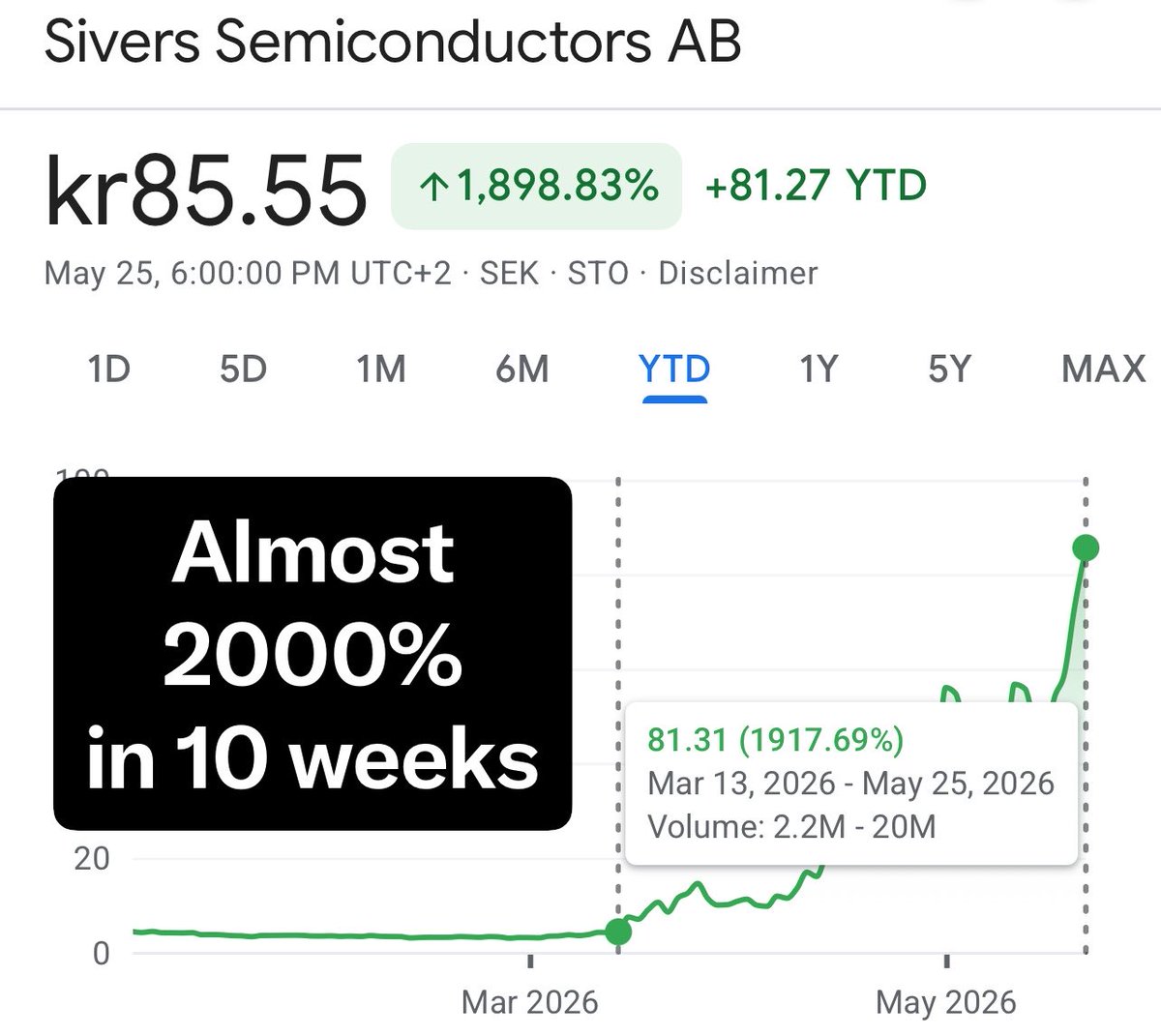

$SIVE can someone pinch me and wake me up? Is this even real life?

It's been 10 weeks since Serenity called this name and gave it the recognition it deserved. It's up almost 2000% in those 10 weeks...

I invested early and heavy, making it 10% of my not-so-small portfolio at a $7.50 average. I'm up 1100%.

This is truly a life-changing stock. We are witnessing a $SNDK in the making or even better, an $AXTI. Except this time, a large number of us were early and ready.

Today was my first day back at the office after parental leave and I can't help but smile at the realization that if I wanted to, I could quit my job since my portfolio is now worth more than 10 times my annual salary.

My wife tells me to realize my gains. I tell my wife to trust me, as she always does.

I'll see you guys at the finish line in 3 years.

Bullish AF

English

The valuation is already twice that.

Of course it will crash. Don't you worry about it.

Thousands and thousands of retail investors are mislead by an anonymous cult leader, grossly overstating the current status of the company.

Don't try discussing potential growth trajectory and business models with them or you will be called a troll.

English

Can anyone tell me how $SIVE grows into the current valuation?

I understand it’s a bottleneck

But they guided for $50m in revenue by 2027

Will they jack up the prices just like memory companies or something that I’m missing

Because if there is no path of it growing into the valuation of $1.5B - it could crash badly. Just don’t know when.

English

@TommyAitchKay That's now beyond 2.9 billion dollars.

2 900 000 000 dollars

It's thrilling, one of the sickest moves I've seen in the Swedish stock market.

See you on the free fall!

🤯

English

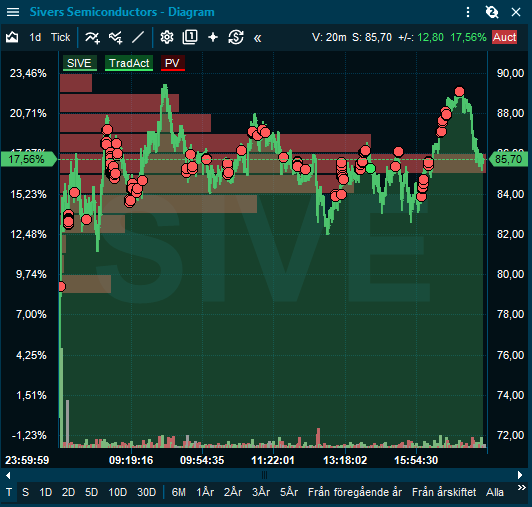

@UbbeInvest Well Idc what you say, 34% day without even US stock market open. Have fun

English

$SIVE has a $10m revenue photonics business with a few really interesting strategic partnerships, mostly in early-stage development. This venture is now valued at $ 2.5bn after a two months explosive upswinging run.

(Sivers also has a ~$20m wireless business which you may want to take into account. It's not part of the narrative so let's stick to the photonics side.)

This would bring Sivers implied photonics multiple to 250x sales.

For comparison:

Nvidia's extreme levels peaked at 45x sales (20-25x today) while being massively profitable and dominating an entire industriy.

That's just bananas. Take those numbers and bring them to any analyst, AI reasoning, seasoned investor or non-anonymous financial professional. "No, that can't be right"

Keep in mind Sivers is a potential pick-and-shovels infrastructure component play competing with large and established players.

Don't get me wrong. It IS an exciting business but currently the stock is akin to paying a million dollars for ape jpgs, $5,000 for a haircut or paying $2,500 for a pizza, or whatever analogy you prefer.

I love the irony that nobody cares about the price tag yet spend all day long looking at the share price.

They're the same thing.

Apes together strong!

English

@PepInvestStocks I think "speculative small-cap hardware company" sums it up pretty well.

English

The craziest part to me is that the market still seems to value $SIVE like a speculative small-cap hardware company instead of what it’s potentially becoming, a mission-critical AI infrastructure enabler with software-like operating leverage.

Most investors still don’t fully understand the asymmetry here.

If hyperscaler deployment timelines hold, Sivers doesn’t need to win the entire market, they only need a small share of the exploding CPO/optical interconnect stack for the economics to become absurd relative to today’s valuation.

The fabless structure is the real hidden weapon:

• minimal CapEx

• scalable through WIN + Jabil

• tiny employee base

• potentially massive revenue per employee

• operating margins that could eventually look closer to elite AI infrastructure companies than legacy optical vendors

Meanwhile, the validation stack keeps growing:

Ayar supplier positioning

Jabil demand commentary

CHIPS Act relevance

Nasdaq uplisting

passive index inclusion flows

increasing institutional visibility

strategic M&A optionality

And unlike many AI names trading at massive forward multiples, Sivers is still early enough that most institutions haven’t even built positions yet.

That disconnect is why the risk/reward still looks wildly asymmetric to the upside in my opinion.

Serenity@aleabitoreddit

I’m not selling a single share of $SIVE. I personally think it’s a once-a-generation long given how many hyperscaler suppliers they’re already in. Coupled with GS extreme TAM expansion projections for both pluggables and CPO in the next 2 years. If you didn’t read the $JBL fireside transcript by now validating demand/timeline. Or the fact Ayar removed Lumentum and Macom from their website as laser suppliers validating moat. Or literal CHIPS ACT funding validating technological importance. Or that management is literally doing everything right in my view, with NASDAQ listing into M&A focus, validating forward growth vision. Upside is just way too compelling at current valuations. Institutions have barely entered yet as well… and we’re about to see tens of millions of passive, long term new inflow next month from Nasdaq, Blackrock, MSCI indexes.

English

Som förväntat var det en varningsklockan man direkt hamna plus, dubblat och lite till idag.

Longterms@Longterms1

Oroväckande att blankningen börjar på plus...

Svenska

@tien_huynh7682 @jasonschips It's called "ramp up" and not "teleport". That's baselines for you, enjoy!

English

@UbbeInvest @jasonschips Sounds retarded to me. Using old rev to caculate when the ramp not even started yet. Stupid college kid think he’s right

English

@Aktiepappa @thekarlgent Var med om samma upplevelse för en vecka sen! Första Jureskogaren 🥳😳

Svenska

Käkade min första Jureskogs-burgare på flygplatsen. Största besvikelsen på länge…. Betydligt mindre än bilderna och smakmässigt som en McDonald’s cheeseburgare som stått två dagar i kylen.

1/5

Svenska

I think this video explains the problem regarding the valuation, and agree it will make people lose their savings. Not related to $SIVE but in general.

youtube.com/watch?v=Sb4W5M…

YouTube

Jason's Chips@jasonschips

" $SIVE can reach $80b because $LITE is $80b" has to be the dumbest and most dangerous investment thesis ever. People will lose their savings listening to all this misinformation. It's sad and needs to stop (I am starting an anti $SIVE crusade). 1. $SIVE is not a bottleneck (despite it being the poster child of the photonics bottleneck craze). A bottleneck, by definition, must be the company that constrains the production of a massive downstream industry. To constrain production, you must both own hard physical assets and hold a dominant market share position. Sivers has neither. Sivers is a fabless design company that relies on WIN for Foundry services, and with revenues of ~$30 million, they hold near zero market share in the massive datacom laser industry. 2. Supply chain analysis is misleading. In semiconductors (or any industry producing a durable manufactured good) switching costs are near zero while process power, cornered resources, and scale dominate. Therefore, "who has a superior product" is far more important than "who supplies what to whom." CPO external light sources require quality lasers meeting noise (linewidth and RIN) and power (400mW+) specs. $SIVE lasers are far inferior to that of larger peers like $LITE. 3. $SIVE valuation is comically detached from reality. On NTM metrics, $LITE trades at 14x EV/Revenue and 32x EV/EBITDA while $SIVE trades at 50x and 650x (!!) those same metrics. As a permanent AI infra bull, I fully agree that consensus is too conservative; however, they are not off by two orders of magnitude. The misinformation needs to stop. Let's help actually help retail understand what they own.

English

Allow me to contribute with some unsolicited feedback.

You are combining an appeal to your own authority based on a fine track record, with bold statements of how the industry will unfold. That can become dangerous when a large audience starts treating probabilistic outcomes as near certainties.

There are tons of uncertainties, such as:

- The competition is tough, Sivers is part of a complex multi-source ecosystem

- At least 6-12 months left until high volume production if all goes well

- Other bottlenecks and chokepoints could affect the broader market adoption

- Hyperscalers slowing down

- Actual revenues and profitability remain to be proven

You know very well that the one thing that doesn't add up is the crazy 2,000%+ development of the share price over the last two months, implying a ~2.5 billion dollar price tag which is simply out of proportion for an early stage unproven business.

Does it mean the company isn't interesting? No, not at all. It's very interesting.

But there is a difference between identifying overlooked opportunities early (which is amazing and impressive) and continuing to push a narrative beyond what the current fundamentals reasonably support.

I do believe that everybody is responsible for their own investments. It's completely optional to follow somebody and read their X posts. However I also believe that with great influence comes some degree of responsibility.

🙏

English

Photonics is nuanced and using ChatGPT/Gemini makes you miss all of it:

1. $SIVE is actually a chokepoint and partially a bottleneck.

The reason it's a chokepoint is leading CPO/optical hyperscaler players go through Sivers, likely:

Ayar. Celestial. Lightmatter. Lightelligence. Poet.

If you take out Sivers, you literally can't make some of their products + delay their roadmap by years.

As many are sole/primary source but are heading the direction on multi-source.

As for the bottleneck argument: Win Semi is the bottleneck for scaling laser production.

But... the nuance is when you have capacity allocated for the next few years.

You become part of the bottleneck itself if players fight you for allocation of finished lasers.

That's the nuance people miss with capacity allocation dynamics.

It's like saying $SNDK is not part of the NAND bottleneck when Kioxia makes all of it.

But when Sandisk has the ultimate control of output supply, they become the bottleneck + have all the pricing power.

Sivers controls output supply of CW lasers given allocations, and as seen with $LITE earnings, CW laser is currently bottlenecked as everyone seems to be stuck producing EMLs.

2. Like how LLMs always uses em-dashes.

You can tell when people use AI when they always use the same "CW is a dumb interchangeable laser" argument or compare "power" specs after conflating different architectures.

That's why your "analysts" using AI will get this wrong over and over.

There's CW lasers... and then there's a specific architectural design that Sivers achieves with DFB lasers.

If you compare power specs with $LITE vs. Sivers, Lumentum wins in isolation. But they're completely different laser architectures.

All the leading CPO players like Ayar, chose $SIVE for an architectural reason for high power, low thermal, laser arrays. $JBL 1.6T LRO also made one of the most dramatic moats cited by their fireside chat, using Sivers lasers.

If you think CW lasers are interchangeable with Sumitomo/Furukawa, and others. And can be plug-and-play... i don't know what to tell you?

Again: $SIVE makes architecturally unique CW lasers for leading CPO players.

3. I'm not sure how many times I need to say this:

$SIVE for 2024-2025 has been going through development contracts. People using TTM revenue or former P/S metrics are using completely the wrong metrics, when there's volume ramp in 2027.

It's the same with $AAOI which volume ramps in H1 2027.

$AEHR which volume ramps after qualification.

$LPK that volume ramps after qualification.

This is just missing qualification cycles in semiconductors and how to model financials currently.

As for the $LITE comparisons (which was also my long last year):

$LITE literally started off selling laser dies before acquisition of Cloud Lite and other downstream optical engine components.

This is where $SIVE is at today with starting off in the laser chokepoint for CPO:

People are modeling laser revenue off very isolated TAM projections. Meanwhile Sivers is targeting M&A to expand revenue for TAM projections.

This is not a simple component FAU + ramp valuation modeling over with a Taiwanese company.

Since Laser companies like $LITE, $COHR are known to downstream expand to make their lasers more valuable, then vertically integrate (fabs, assembly) afterward.

Again, Sivers worked with Ayar and these types of companies before they all became billion dollar companies. I have high conviction knowing they know what to acquire down the ELS/optical engine stack + pluggable transceiver for TAM expansion.

It's just annoying when I get people who don't understand the nuances backseat commenting wrong things about my longs.

I got the same thing about $AXTI is not a bottleneck! InP isn't needed! China! back at $14.

Now it's $140

I got the same thing about $AAOI "is going down 50%!" back at $65. or "AOI management is shady at $30".

Now it's $170

I got the "there's nothing new with $SOI" back at $45.

Now it's $170.

I think I'm one of the few who actually understands the nuances with photonics, since I did call out $LITE, $TSEM, Innolight, $AXTI, $AAOI, $SOI, that outperformed both photonics markets and overall markets over the past year.

And now I'm long on $SIVE.

English

@UbbeInvest Let's say again but slowly this time, stocks are forward looking

English

@glozanomoran Looks like it will list at around 100x sales? Which is slightly ridiculous.. Let’s party like it’s 1999!

English

@UbbeInvest So by your logic, how much do you think, for example, SpaceX is “worth”?

English

Did you mean P/S?

Of course the current sales is relevant if you want to get an idea about the future. That's why it's used everywhere, you see!

If you see something really crazy like 50x or 250x sales, the market demands explosive growth. Preferably showing strong progress every quarter.

Last year they grew their photonics business with 19 % from ~$8.4m to ~$10m. They need to grow faster than that, quite a lot faster.

English

@UbbeInvest P/E on $SIVE at this stage is pretty irrelevant, nobody is investing on what the revenue is right now, they’re investing the what the revenues will be in 2 years.

English

Hur ”early” är Sivers folket tro? Har för mig interfox hade T-shirts också.

Mr_Asparagus🇪🇺@NomMiniman

Today my new $SIVE uniform arrived! Huge thanks to @PepInvestStocks for the shirt! As someone holding a pretty massive position in $SIVE, I’ll be wearing this with absolute honor. Make sure to follow @PepInvestStocks one of the best out there!♥️🙌

Svenska

@UbbeInvest You are equating a photonics manufacturer with proven tech to NFTs. Are you trying to sound like an idiot? You also aren’t taking into the fact that they are massively scaling future production in the 1 year time frame, so that 250x sales will go down rapidly.

English

@Discod144 Ah my apologies, I should have stated more clearly that this is not investment advice!

English

@UbbeInvest Please don’t give investment advice. Valuing a growth company using TTM sales is amateur level especially when the growth ramp up is over the next 3 years. Stick to index funds.

English

@SaintAgnesBets Congratulations on fantastic returns in such a short time!

The potentia... what. Right. Never mind :)

Damn you for stealing the ape.

English

@UbbeInvest markets are forward looking. the potential of $SIVE is way more than Nvidia's was at its peak P/S

I might just steal that ape Jpeg though. it's mine now

English

@TommyAitchKay I will break it down for you:

Number of shares: 319 953 572

Price per share: 72.9 SEK

319 953 572 * 72.9 = 23 324 615 399 SEK

23 324 615 399 SEK = 2 489 897 772 USD

Yes, markets are forward looking, thank you for that.

English

@UbbeInvest Before you post anything, I'd suggest checking your fundamentals. Sivers sits at 1,61bnEUR = 1,87bnUSD. Markets are forward looking and pricing in future revenue and growth potential due to apparent supply chain bottleneck position. Execution risks are there but it's quite simple

English

@jonesrrrrrr Why not?

When these "technology and assets and balance sheet" you talk about have nothing in common with the share price, it's strikingly similar to how the NFT craze worked out a few years ago.

Great company

Great apes

Apes together strong!

English

@UbbeInvest lol never compare a great company with technology and assets and a balance sheet to an NFT again. Thanks broskie!

English