Sabitlenmiş Tweet

Decided to make a Substack (see bio). Will be posting free articles on market and paid articles on individual stocks

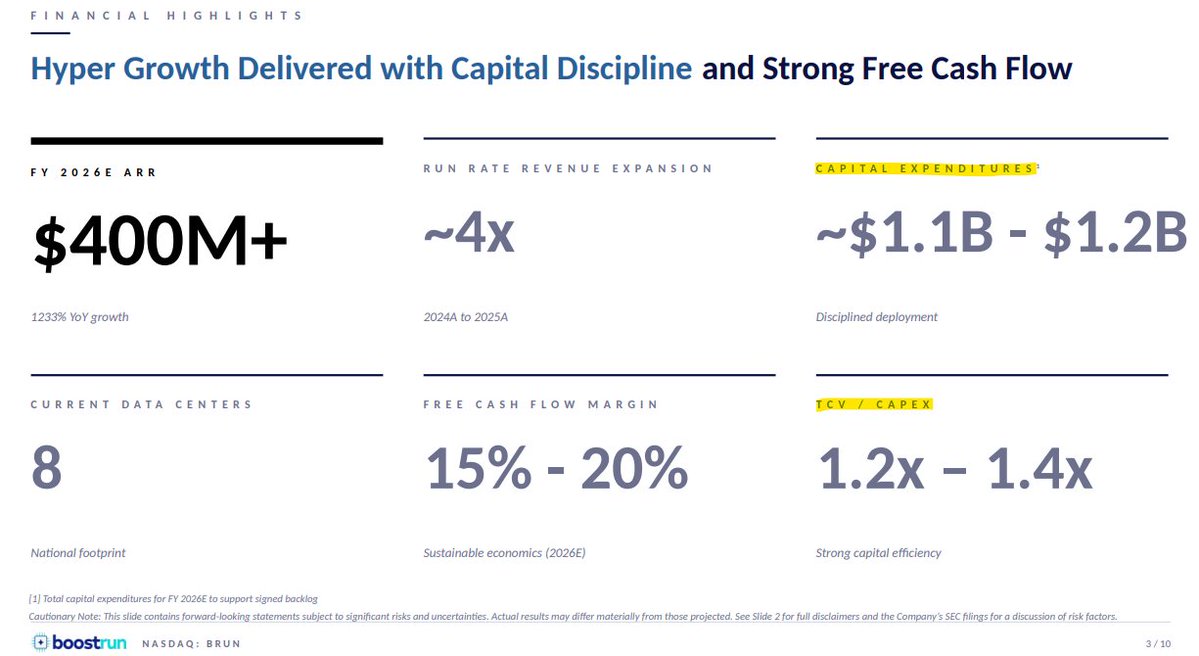

First write up is on $brun, which I think will 3x in the next 12 months following a similar path as $NBIS $CRWV

Write up covers founding origins, business model explained simply, $nvda Exemplar Cloud partnership, customers and partnerships, compares coreweave and nebius trajectories to BRUN, covers unit economics of BRUN's contracts including IRRs, insider lock up debunked, sizing the neocloud market and brun's opportunity within it, rebuttals to common questions, valuation framework

Let me know what you think

@JonahLupton

English