Sabitlenmiş Tweet

Underlying_hl

141 posts

Underlying_hl

@Underlying_hl

“what’s the underlying of a hyperliquid ?”

Katılım Ağustos 2025

351 Takip Edilen31 Takipçiler

Underlying_hl retweetledi

$HYPE has once again reached $44, a first since November 1.

$BTC was trading at $109,532

$ETH was trading at $3,852

$SOL was trading at $186.71

English

Underlying_hl retweetledi

Everything just lined up for Hyperliquid. Let me spell it out because I don't think people fully see what happen.

April 13, 2026:

The SEC Division of Trading and Markets publishes a staff statement explicitly carving out a path for crypto user interfaces that prepare transactions in crypto asset securities to operate without registering as broker-dealers.

The conditions: self-custodial wallets, transparent routing, disclosed fees, no discretion over execution, no payment for order flow. Hyperliquid's architecture already matches almost every single one of these criteria by design.

Same day:

Jeff quietly updates his bio. From "building a pretty good dex" then "building a pretty good L1" and finally "building a pretty good house of all finance"

This week also priority fees go LIVE on mainnet in alpha mode. Not testnet. Real HYPE burning, real auctions, real revenue capture. The mechanism that was science fiction two weeks ago is operational today.

Now connect the dots.

HIP-3 lets anyone deploy perps on ANY asset. Oil, gold, Apple, Tesla, Nasdaq-100, wheat, the VIX. Currently on Hyperliquid you can trade these assets 24/7. On traditional exchanges you can't. Wall Street closes at 4pm. Hyperliquid never does.

HIP-4 adds prediction markets on real world events. CDS-like instruments. Parametric insurance. Binary options on economic data. All settling natively on the same L1 as the perps. All cross-margining against each other in the same account.

Priority fees create a native pricing mechanism for execution order. No private order flow. No dark pools. No colocation advantage hidden behind closed APIs. Anyone willing to pay HYPE can access the front of the line.

Every bid burns the native token into protocol value.

And now the SEC has essentially blessed the model as long as the interface stays user-sovereign, transparent, and non-discretionary.

What does that unlock?

Institutional desks in the US that were waiting for regulatory clarity can now start building on Hyperliquid without fear of the broker-dealer registration trap. Prop shops that want to trade oil and Tesla on weekends have a venue that matches their needs.

Market makers who used to need ISDAs and prime broker relationships can now provide liquidity via simple API calls. Hedge funds that wanted 24/7 exposure to equities without the paperwork finally have a legitimate path.

The traditional finance infrastructure is closed 40% of the time. Hyperliquid is open 100% of the time. And now institutional US participants have a legal framework to engage with it.

What's missing?

Three things, and all three are solvable.

First, full transparency on order routing so the last gray zone disappears. The SEC statement is clear that routing logic must be based on pre-disclosed and objective parameters.

Hyperliquid's matching engine is onchain and auditable by design, but the routing layer from frontends needs to be documented and verified. Androolloyd's work on independent client verification is directly relevant here.

Second, a clean Clarity Act or equivalent federal legislation that codifies what the SEC staff statement already suggests informally.

Staff statements are not law. A full legal framework is. Once that lands, every institutional compliance team in the US gets a green light to engage.

Third, dedicated stablecoin infrastructure for TradFi. USDH is a start. USDC on Hyperliquid via Native Markets is another.

But institutional desks need specific rails for settlement, reporting, and treasury operations. The pieces are being built, and the pace is accelerating.

The economics for HYPE holders are straightforward. Every new institutional dollar that enters Hyperliquid generates fees. Fees flow back through staking, priority auctions, and structural demand for the native token.

The more sophisticated the users, the more they pay for priority. The more they pay for priority, the more HYPE burns. The more HYPE burns, the tighter the supply. The tighter the supply, the higher the floor for anyone holding.

This isn't about a new DEX. This isn't about a new L1.

This is about an onchain venue that can host the entire apparatus of global finance on infrastructure that runs 24/7, settles in seconds, is transparent by design, and is now being implicitly legitimized by US regulators.

Jeff wrote it plainly. A house for all finance. Not for crypto traders. Not for degens. For all finance.

TradFi ran on closed systems, delayed settlement, fragmented liquidity, and restricted hours for 100 years.

Hyperliquid is rebuilding the same functions with open access, instant settlement, unified liquidity, and continuous operation.

The institutional door just opened. The priority fee machine just turned on. The product suite is live. The regulatory path is emerging. The timing isn't a coincidence, it's a convergence.

Just use Hyperliquid.

English

Underlying_hl retweetledi

This is the story of Hyperliquid, the most profitable startup per employee on earth, told from a guarded office in Singapore.

Last year, its team of 11 generated $900 million in profit. It's 3 years old, has never taken a dollar of venture capital, and is beginning to change how century-old markets work.

Its founder, Jeffrey Yan (@chameleon_jeff), had never taken a physics class when he picked up a textbook at 16. Two years later, he won gold at the International Physics Olympiad. In 2019, he started trading with $10,000 from a living room in Puerto Rico—working off a television because he didn't own a monitor.

Within 3 years, he was running one of the largest anonymous crypto trading firms.

Then he shut it down. Yan was rich and free, but he had spent years inside crypto, watching it betray itself. Bitcoin's central premise was decentralization. Yet the biggest exchanges were centralized. Crypto kept reintroducing the dependence on trust it was built to eliminate. He set out to create what should have existed.

Hyperliquid is a blockchain with a trading exchange on top, and anyone can build on it. Yan's vision is to house all of finance. In 3 years, it has done over $4 trillion in volume. And in the past few months, it has begun to outgrow crypto.

Markets for oil, silver, and the S&P 500 now trade on Hyperliquid around the clock, weekends included, and are growing roughly 40% week on week. When the US and Israel bombed Iran on a Saturday in February, Hyperliquid was the venue traders turned to.

Hyperliquid's success has cost Yan his freedom. He works out of a secret office in Singapore and cannot travel without two bodyguards. Even the team's housekeeper doesn't know what they do.

In January, @domcooke spent a week at their office. Read his profile on Yan and @HyperliquidX below.

English

Underlying_hl retweetledi

Most protocols are built by a team. Hyperliquid is being built by an entire army.

It's all of us. We are all Hyperliquid.

From @rediamondjr @dschamis @hyunsujung_ taking the charge in the TradFi world alongside @HyperliquidPC in Washington

To deployers like @tradexyz @Kinetiq_xyz @felixprotocol @Dreamcash @ventuals @tradeparagon

To projects building on builder codes like @phantom @InsilicoTrading @pvp_dot_trade @Dexari @Rabby_io

To solo devs like @LorisTools @Yaugourt @Syavel @skewga_capital @janklimo shipping tooling, dashboards & explorers

To Hyperliquid aligned stable-coin issuer @nativemarkets

To researchers like @HyperliquidR @smartestxyz @Decentralisedco

To HyperEVM protocols like @hyperlendx @ryskfinance @prjx_hl and many others

To communities like @hypurr_co @HLglobal_ and the global regional communities and volunteer leads curaing HL events

I could go on and on, and I'd still be missing so many.

I'm proud to be one small part of this.

All of us. Working toward one collective goal.

Until we house all of finance.

Hyperliquid.

English

Underlying_hl retweetledi

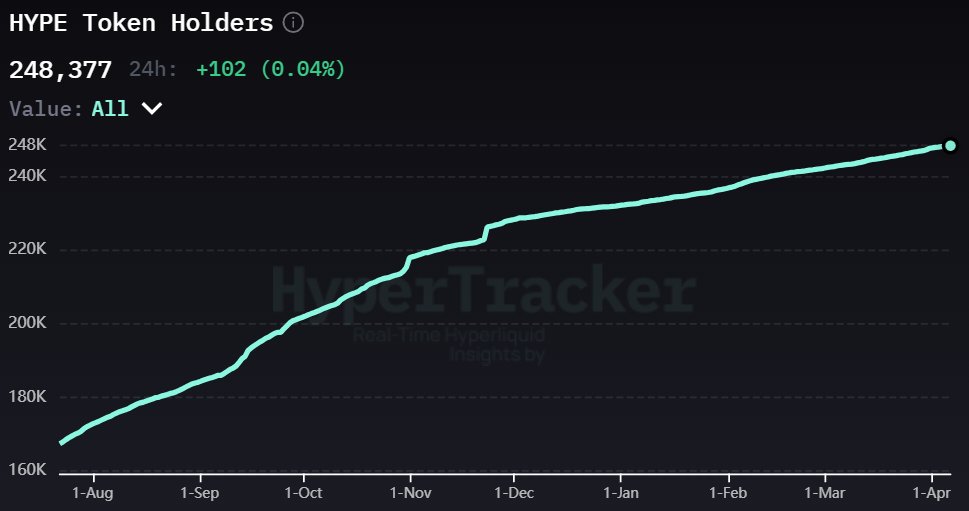

The number of $HYPE holders has not reached 250,000.

Only 51,727 holders own more than 10 $HYPE, and only 7,177 wallets hold more than 1,000 $HYPE.

English

Underlying_hl retweetledi

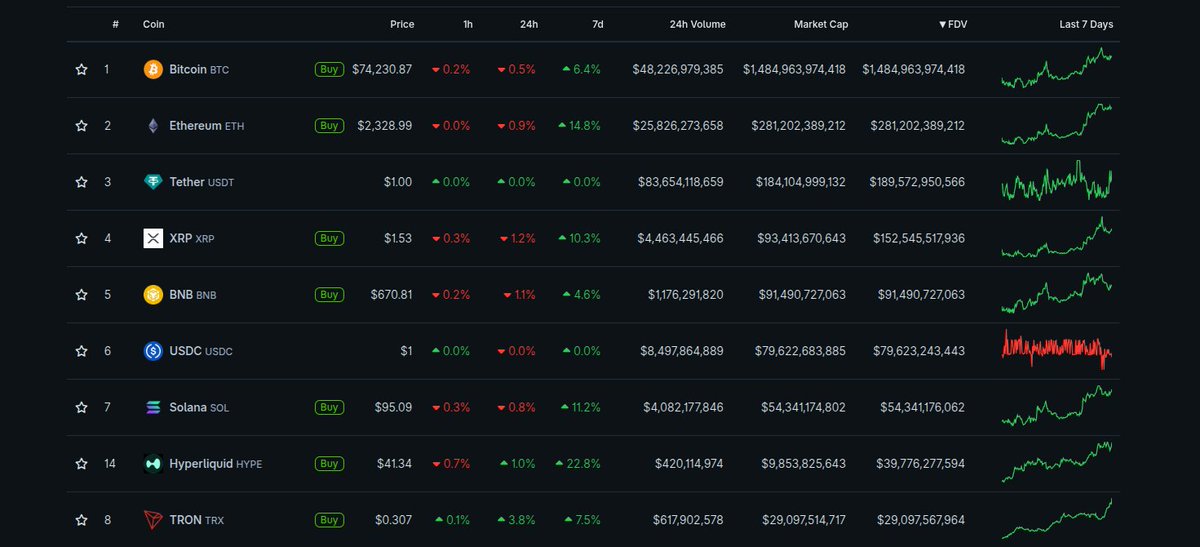

HYPE/TOTAL alltime high

If you're a BTC, ETH, XRP, BNB or SOL maxi:

you could trade 0.03%, 0.14%, 0.26%, 0.43% or 0.73% of your coin's total supply for 1% of HYPE's

then sell it at a higher ratio to defend your coin and increase your position in it

TechnoRevenant@Techno_Revenant

English

@KookCapitalLLC @RemindMe_OfThis 2 years

50m days being the norm will see the price higher than $200 for sure

🌝

English

in the next 2 years hyperliquid will go from

doing $5m in token buybacks per day to $50m

hype token supply will be burned at an alarming rate

market share upside is ~infinite~ bc hyperliquid will eat tradfi derivative mkt share

and prediction market volume

hype $200+

English

Underlying_hl retweetledi

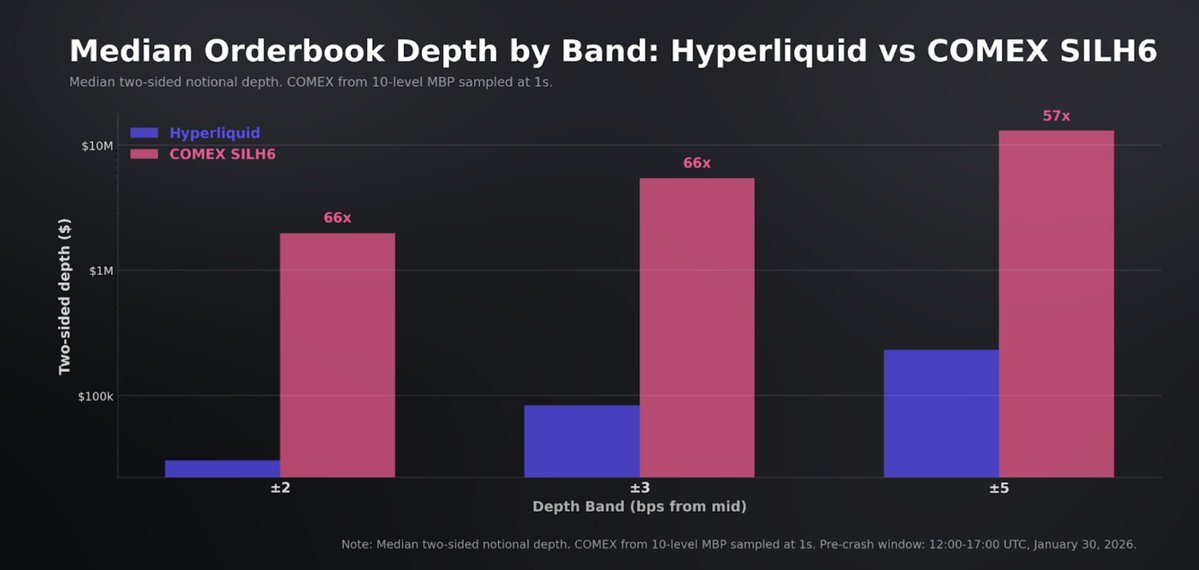

“Hyperliquid’s HIP‑3 silver perp cleared the most volatile silver regime in DECADES without halting and with tight top‑of‑book pricing for the dominant retail and mid‑sized flow

Still, the HIP-3 constraint is capacity; the venue handles small‑to‑mid clips well, but large‑clip execution remains materially limited relative to COMEX depth.”

Fantastic coverage by @shaundadevens on HL's silver market. An incredible accomplishment barely a month after listing.

shaunda devens@shaundadevens

English

Underlying_hl retweetledi

A personal update from Richard E. Ptardio

=

Chaps, after much soul-searching, I have decided that the time is right to make a decisive move regarding my future in crypto-currency.

I intend, as you young fellows are so fond of saying, to lock in.

I appreciate that some founders and investors are moving away now that prices have gone a little limp.

But as a man who survived Black Wednesday, the Asian Financial Crisis and the dot com implosion, I find it rather hard to be frightened by a screen going slightly the wrong colour.

A little wobble on a chart feels almost nostalgic.

Crypto-currency has given me not only a renewed sense of purpose, but the daily joy of engaging with a most unusual group of new friends. You chaps, chiefly.

So no, I shan’t be leaving. If anything, I’m loosening my tie and getting down to business.

Crypto-currency will have to endure me a while longer.

English

Underlying_hl retweetledi

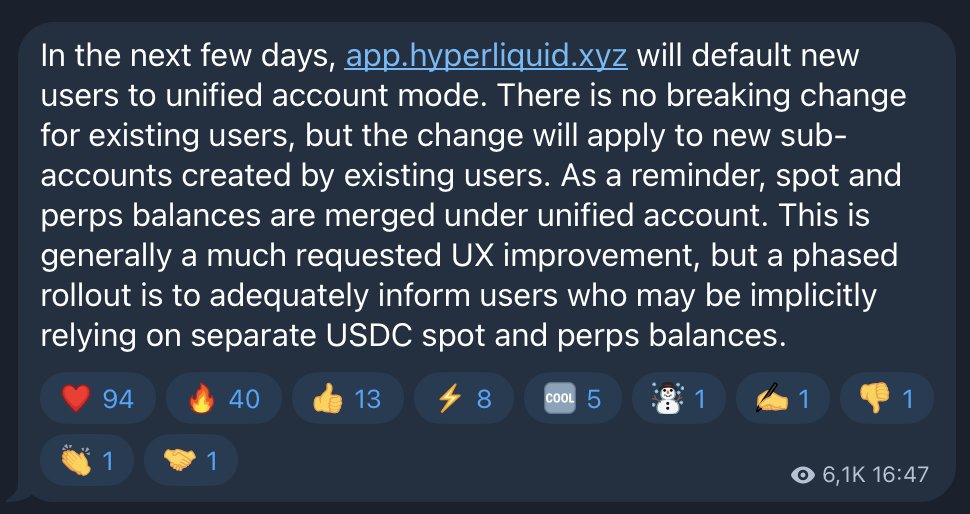

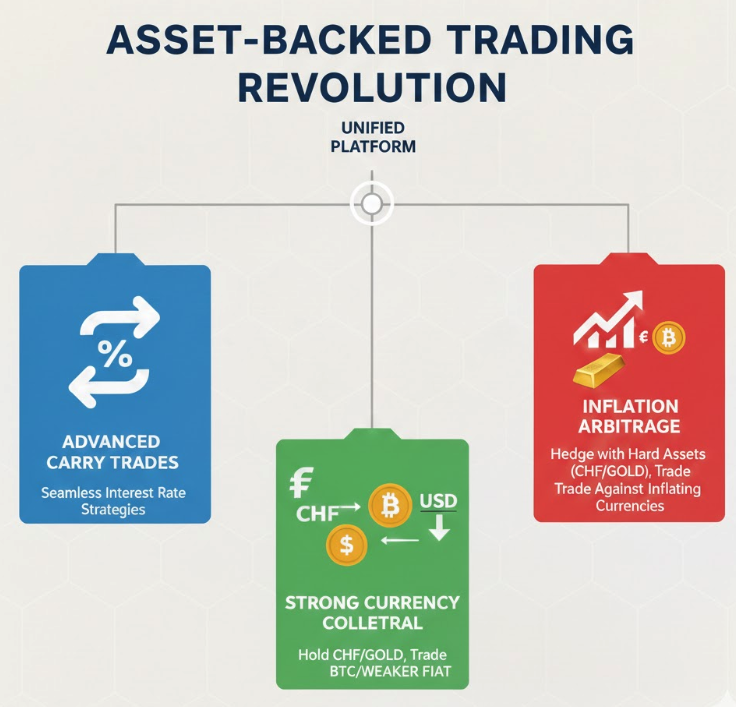

Hyperliquid's unified account era is here.

New users will now have unified accounts by default. This means spot and perpetuals are merged, allowing you to use your entire portfolio to back your positions.

However, in my opinion, the real game-changer is what’s coming: spot equities and Forex as collateral.

Imagine the possibilities when you can use Tesla stock or Gold to back your trades. We are moving toward a platform where you can pull off professional-grade moves with ease:

> Advanced Carry Trades: Execute interest rate strategies without moving funds between different platforms.

> Strong Currency Collateral: You could hold Swiss Francs as your base (which performs much better than the Dollar long-term) and use them as collateral to trade BTC or weaker fiat pairs.

> Inflation Arbitrage: Trade Bitcoin against currencies with high inflation while keeping your "savings" in a hard asset like CHF or Gold.

Hyperliquid is building the infrastructure to do things we can't even fully imagine yet.

Having everything under one roof (equities, Forex, spot, and perps) is going to make traditional banking look like a joke.

We aren't just trading tokens anymore; we are engineering wealth with total flexibility.

English

Underlying_hl retweetledi

@benjamincowen Obi Ben Kenobi - are you monitoring the force of Hype whilst you continue to master the crypto universe ? ✨

English

In 2019 when BTC dominance dropped, it dropped because BTC was dropping faster than alts.

Why?

Because by the time the bear market started, altcoins had already been annihilated.

Once BTC broke out of the bear market, BTC dominance went back up to the highs.

So I think it feels similar now.

BTC is post-top and after QT ended.

BTC goes down and drags the rest of the market with it.

Good chance this process ends later this year, so stay tuned!

English

Underlying_hl retweetledi

I don't think the NASDAQ should be the total addressable market.

It's like saying Uber's TAM is 10% of the total taxi market (10b and not 200b+).

By improving the product offering through new use cases or improving accessibility, you can grow the overall market massively like Uber and Amazon did.

Hyperliquid will have every future market listed on its platform through potentially infinite independent deployers, with no KYC or any barriers to entry.

This increases the customer base to anything on Earth with an internet connection. And every style of market will be tradable if Jeff's vision is to be realized.

HL can also charge more than traditional markets. Silver perps at 2b volume earned HL & tradexyz around 70k in fees. For the same volume, I think the CME would earn around 13.58k. (correct me if wrong)

People don't mind paying 0.003% fees if Silver moves 10% per hour and you can use 20x lev.

For reference, max lev in stocks / commodities is usually under 8x. So this forces people into options that are harder to use.

So I think higher fees aren't going to limit HL as long as they can get these novel markets listed.

Hyperliquid also benefits from network effects. It's a massive hassle to wait 1 business day to transfer money between brokerages to take advantage of lower fees for a specific market. You'd rather just have everything on one brokerage, especially if fees are negligible compared to volatility.

We also know liquidity has network effects (more traders -> more money for MMs to farm -> more liquidity).

So this would be another network effect style advantage that lets HL have pricing power.

But is HL priced fairly today?

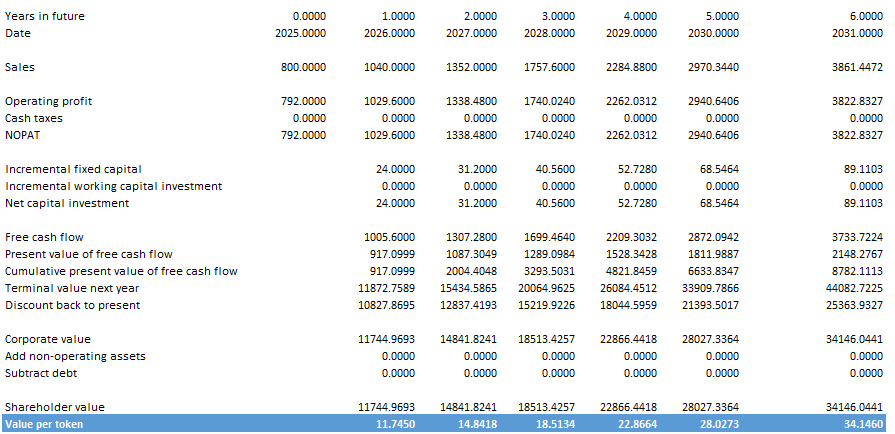

I'm using 800b annual revenue at 99% profit margin, an investment rate of around 10% of revenue per year (5x the actual rate), ~9% cost of capital (super high estimate) and the high 30% growth rate that TraderNoah mentioned.

Using these estimates, HYPE would hit its current value of 33 in 6 years.

So HYPE is priced similar to something like Dominos Pizza in 2019. It has high expectations priced in, but not unreasonable at all.

I know a 30% growth rate is high, but I think it's reasonable for the first few years of lifespan considering HYPE grew by 300%+ this year.

And personally I don't think the growth rate will be 30% per year. I also think the execution risk is lower than 75%. HYPE has an effective monopoly with network effects, and free to grow short term without the constraints that tradfi markets are dealing with. Eg HL is just the backend for separate legal entities listing these markets.

I treat this like a moonshot with 100x potential, so I'm willing to hold through through temporary overvaluations and multiple 70% drawdowns.

I don't mind holding it at 12 or 35 since I think it will go to 2000.

Noah@TraderNoah

In the most aggressive scenario, I think you need a bit under 30% annual returns to hold HYPE through 2030. I think the most aggressive assumption of true supply of HYPE is ~60% of fd, so its $20bn marketcap assuming no future airdrops. You need to believe that the expected value of HYPE is $56bn EOY 2030 to own it today. Putting aside the 25-75% probability skew that it somehow dies between today and 2030, you're assuming it gets to the Nasdaq's current valuation. The market of non-fundamental analysts will point to the high margins, low team number etc... as a sign of strength, when in reality having a high margin isn't a good thing for future business defensibility. Not arguing its necessarily bad, just to say its objectively not a good thing. So the question is then, what is the terminal margin for HYPE in 2030 if it succeeds, what's its success worth, and what's the multiple on 2030 earnings that you can pay today. Let's say there's 25% probability of failure, and in the rest of the scenarios HYPE gets to $75bn marketcap (required to be ev nasdaq 2030), on a mature company, the correct earnings multiple for an exchange with high margins and high business defensibility is 20-25x (average of CME, ICE, NDAQ, etc...). Let's say they exit with 50% margins (high end of comps) and trade at 25x (high end of comps) , you need $6bn of revenue. I'm giving you aggressive assumptions partially anchored to the last century of financial history around competitive dynamics of all markets. I understand that people will say "margins are going to be higher than 50%" or "it's doing $800mm of revenue, and was doing over $1bn earlier, so $6bn isn't hard to get to" but that requires the future to differ from the past of financial history in ways that none of these people have attempted to form a coherent argument for. There's recency bias that lets people believe that the current metrics are sustainable, but the most likely outcome is that high margins and large enough revenue opportunity invite competition. In order to defend business, it will have to sacrifice margin by lowering pricing or spending more to differentiate from competition. Competition may not be crypto-native. It will involve regulated entities competing with more resources than crypto incumbents. I'm willing to buy $HYPE at a relatively high price vs. what most non-crypto valuation focused people would pay, but that doesn't mean that the current price is the right price. The most likely explanation is that there's still on average overvaluation across tokens, and many people who feel forced to allocate to crypto feel the need to have HYPE exposure because some of the other largecap alternatives are relatively worse ev.

English

Underlying_hl retweetledi

Soon Hyperliquid will have a wide selection of spot and perpetual RWAs to complement their crypto listings.

And then they’ll have crypto and equity options.

And then they’ll have prediction markets and sports betting.

And then they’ll have native borrowing and lending on HyperCore.

They’ll have a wider selection of assets with deep liquidity than any other traditional or crypto exchange in the world.

Seems CT is finally coming to the conclusion that Hyperliquid truly can house all of finance.

English

@ThinkingUSD dogS - for anyone also saying dog, for your sake and theirs get them a sibling or 5 - it’s so so much better than having only 1 dog, which is arguably unfair 🐾 🐾 and usually no extra ‘work’, at times it saves you time and effort

English

Underlying_hl retweetledi

HyperCore will support outcome trading (HIP-4). Outcomes are fully collateralized contracts that settle within a fixed range. They are a general-purpose primitive that are useful for applications such as prediction markets and bounded options-like instruments. There has been extensive user demand in both of these areas, and builders will likely think of novel applications as well.

Outcomes bring non-linearity, dated contracts, and an alternative form of derivative trading that does not involve leverage or liquidations. The outcome primitive expands the expressivity of HyperCore, while composing with other primitives such as portfolio margin and the HyperEVM.

Outcomes are a work in progress and currently only being tested on testnet. Canonical markets based on objective settlement sources will be deployed once technical development is complete. Canonical markets will be denominated in USDH. Pending user feedback, the infrastructure will be extended to permissionless deployment.

English

@tenten19901107 Vibe check checks out ☑️ 2 truly toxic humans

English

@benjamincowen Don’t change, you done the space a great service

English

I hope I saved some people from the pain of altcoins over the last few years.

With that said, I have recently started acting like an arrogant asshole about altcoins.

I am sorry.

I’ll try and be better.

English