Sabitlenmiş Tweet

DCo

1.1K posts

@Decentralisedco

Research and investments. DMs open.

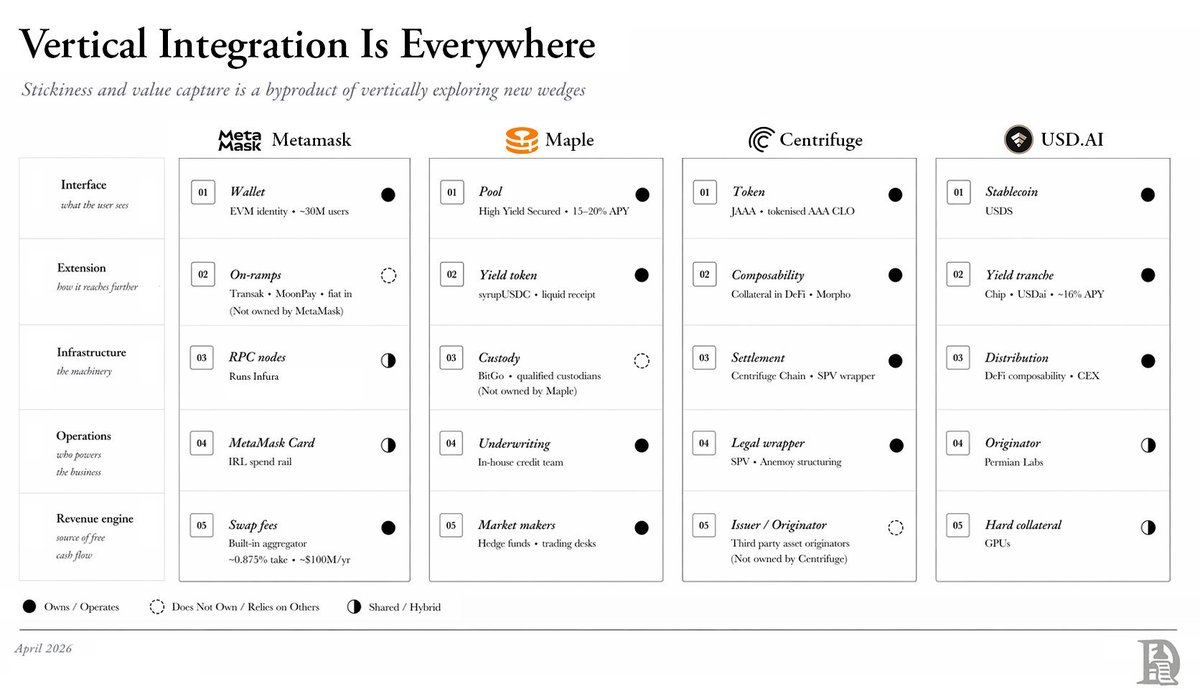

Margins in crypto will increasingly come from firms capturing the whole supply chain for value. That means building capability to speak to legacy legal systems and traditional financial markets. Vertical integrations for capital are everywhere for those with eyes to see.

Margins in crypto will increasingly come from firms capturing the whole supply chain for value. That means building capability to speak to legacy legal systems and traditional financial markets. Vertical integrations for capital are everywhere for those with eyes to see.