Sabitlenmiş Tweet

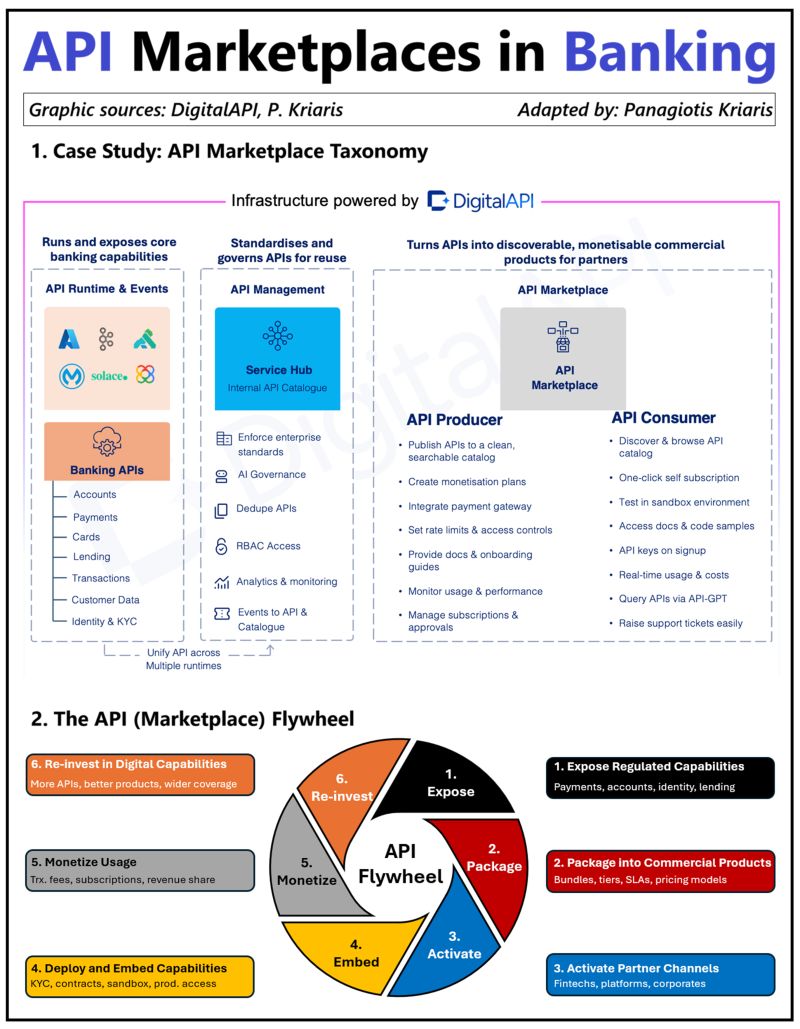

Sendsprint's Market Entry Toolkit is that bridge you need to launch fast in the US Market.

Our founder, Damisi Busari, shares more details on what you need to know about our infrastructure.

Contact us now via #diaspora" target="_blank" rel="nofollow noopener">sendsprint.com/contact-sales#… to get started with us.

#crossborderpayments #internationalpayments #moneytransfer #crossborderpaymentsinfrastructure #remittanceservices

English