...above all, human ® retweetledi

...above all, human ®

5K posts

@VOC1628

Passionate about investing, crypto and macro-economics. Learning daily to make smarter decisions. Join me on this journey of discovery and growth!

March was a tough month on investors. Global equities lost $12 trillion in March, marking the largest monthly dollar decline on record.

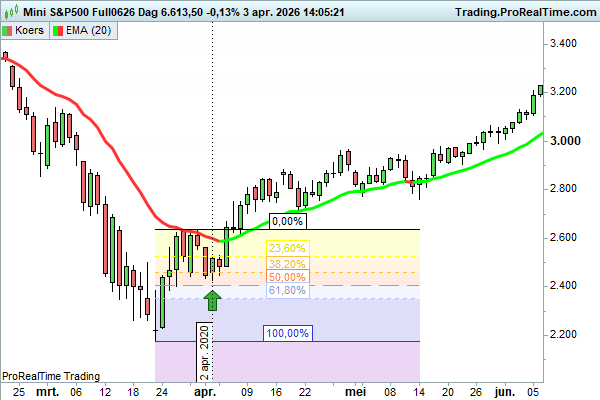

The oil market now reminds me of when prices were around $30 in March 2020. Plenty of people who never looked at oil were going long oil futures, not realising what could happen to the roll. A few weeks later prices traded negative, with a $50+ contango for WTI a day before expiry. They looked at oil futures like equity, not understanding the impact of futures roll. This time is similar, plenty of people shorting the oil market thinking the Strait of Hormuz will eventually reopen and things will go back to normal. Many are trying to call the top. Without realising they might have to roll their shorts at $30, $50, $70+ backwardation?

#MOVE INDEX

Herinner je de Nixon Shock in 1971? Vlak daarna de energiecrisis van 1973 die resulteerde in petrodollar (structurele, kunstmatige vraag naar dollars)? Dat was geen toeval; het was het startschot voor het Worst Bank Scenario dat ik al jaren blootleg: de systematische bankenfraude met derivaten en collateral die de macht centraliseert bij een paar elites. En nu? We zitten wéér midden in een nieuwe energiecrisis. Maar dit komt NIET onverwachts. Dit is geen reeks ongelukken. Dit is het logische vervolg van het trans-Atlantische plan uit 2007/2008 van VS en EU, het Verdrag van Lissabon en het strategisch concept van de NAVO: Klimaatagenda + energietransitie + pandemiebestrijding + de oorlog in Oekraïne + de push voor een onafhankelijke Palestijnse staat… het hangt allemaal samen. Het is geen redding voor het klimaat. Het is een blauwdruk voor controle: • Hogere energieprijzen om afhankelijkheid te creëren • Pandemiemaatregelen om burgers te laten wennen aan beperkingen • Oekraïne om Rusland te isoleren en de transitie te forceren • Midden-Oostenplan om de energiekaarten opnieuw te schudden Alles dient één doel: de vervolmaking van de Verenigde Staten van Europa en de band met de NAVO te versterken om de multipolaire orde te vervolmaken (dedollarisatie). Terwijl wij de prijs betalen, bouwt de elite het nieuwe financieel-geopolitieke systeem. Het Worst Bank Scenario ontvouwt zich voor onze ogen. Tijd om wakker te worden. Dit is geen samenzweringstheorie. Dit is het plan. Samenzwering in de praktijk. #WorstBankScenario #Energietransitie #TransAtlantischPlan #VerenigdeStatenVanEuropa #KlimaatAgenda #NixonShock

So let us assume Trump does wind down the US military campaign (even as it would raise the obvious question of why he has just sent thousands of American troops into the region), while the Strait of Hormuz remains closed. What, then, did those additional three or four weeks of war actually achieve? - The bulk of the nuclear threat has been neutralised in the first few days. - Iran’s Supreme Leader was killed within the opening phase of the conflict. - The Strait of Hormuz was not (effectively) closed until only a couple of weeks ago. - There is still no meaningful sign of regime change, let alone of the Iranian people being lifted out of the shadows. - Persistently high energy prices will push inflation higher and send consumer spending lower. - Central banks, now myopically focused on raising interest rates because they (deliberately?) failed during the post-COVID inflation surge, are likely to make matters worse. - Energy supplies from the Middle East will take months, if not longer, to normalise. - Tensions surrounding Israel will remain exceptionally high for years. - And Trump cannot return home claiming a clear victory that helps him ahead of the midterm elections. I'm sure a lot of people think differently, so help me out here.

One of the most influential actions of the Nixon Shock in 1971 was ending the dollar's direct convertibility into gold, leading to a free float of currencies. This caused greater exchange rate volatility, increasing the demand for repos (simply put: borrowing against collateral) as a means of managing liquidity. Simultaneously, book-entry securities trading was developed, allowing securities to be transferred via book entry. During the same period, book-entry (digital) securities trading emerged (in the Netherlands, the Dutch Book-Entry Securities Act was introduced in 1977 by Wim Duisenberg—the man who also became the first president of the ECB at the beginning of the century). In 1968, Ginnie Mae was founded, and in 1970, the first securitization (the packaging and sale of large bundles of mortgage loans) took place. Trading in book-entry (digital) securities was "born." Collateral no longer consisted of gold, but of (government) debts. Banks and other financial institutions used repos (borrowing against collateral) to manage their short-term liquidity in an environment of less predictable currency values. Central banks, including the Federal Reserve, increasingly used open market operations, including repos, to influence the money supply and interest rates. This meant that repos were not only a tool for financial institutions to manage liquidity but also became a crucial component of monetary policy. With increased volatility, managing counterparty risk in repo transactions became more important. This led to further developments in the way repos were structured, with greater attention paid to the quality of the collateral and the terms of the agreements. Swap lines (repos) were established between the Fed and the ECB starting on 9/11. In 2002, the European Collateral Directive was enacted to enable the trading of collateral within the EU. It took years for this directive to be implemented into law. The credit crisis was not unexpected and was "resolved" (disguised) by central bank repo transactions (buy-back programs) to provide liquidity to banks, which in turn used these banks as collateral for their over-the-counter derivatives (collateral upgrading). In the EU, a guarantee scheme was established in 2008 by the EC on the advice of the ECB to conceal the banks' enormous collateral shortages in over-the-counter derivatives. However, Dutch banks did not avail themselves of this state aid (the Dutch State was advised by Rothschild) at the last minute because they had secretly arranged these guarantees from the pension funds via ABP/APG and PFZW/PGGM. Through an illegal collateral carousel, the Dutch banks ABN AMRO, ING, and Rabobank were bailed out by the pension funds. Since the credit crisis, swap lines between G7 central banks have served as the foundation for the G7's developed multipolar financial (blockchain) system (as a counterpart to the BRICs and the rest). In 2022, the Securitized Overnight Finance Rate (repo rate) was introduced in the US as part of the Worst Bank Scenario. The Euribor and LIBOR frauds were as of 2008 orchestrated to trigger the transition to this repo rate. The ECB's transmission protection instrument, the TPI, was also introduced in 2022. In the Worst Bank Scenario, this is called the "Draghi Collateral Discount Window." Read Worst Bank Scenario and discover how the G20 rolled out a new Bretton Woods 2.0 with this repo market in 2008 (the pilot for the new multipolar crypto/wholesale CBDC system has been running at the Bank of England since 2021) and how our pension funds were abused for this purpose. The pension transition is part of this scenario. Gold has been purchased again by (central) banks since 2008 because it is included in the OTC and repo regulations as "eligible" collateral and is in practice used as hedge for the losses in value of the purchased bonds/packaged loans (liquidity management). The English version is available abroad via Amazon, among others.

“It is threat that created the United States of America. It is also threat that can lead to completion of the political Europe.” Attali, 2015 (2015: opkoopprogramma ECB, neg. rente, scheiding bankverzekeraars => nieuw transmissiemechanisme (2007-2022) Bankenfraude.nl