Sabitlenmiş Tweet

Congress just handed one company a legal monopoly on U.S. military optics.

Almost nobody has noticed.

$LPTH (LightPath Technologies) — ~$871M market cap.

---

**The trigger**

China controls the vast majority of global germanium refining — the material inside every U.S. military thermal imaging system. In 2023, China imposed export controls, driving a 65% price surge.

Congress responded with the FY2026 NDAA: a hard January 1, 2030 deadline requiring complete elimination of adversary-sourced optical components from all U.S. military platforms.

Every major defense prime must redesign their optical systems.

One domestically produced, NDAA-compliant, germanium-free infrared glass is qualified at scale.

LightPath's BlackDiamond™ — compounded entirely at ITAR-registered U.S. facilities.

---

**Why BlackDiamond™ wins**

Germanium's refractive index shifts with temperature, causing defocusing requiring heavy mechanical correction or cryogenic cooling.

LightPath's BDNL-4™ — exclusively NRL-licensed — has a *negative* thermo-optic coefficient. Pair it with a positive dn/dT lens and thermal shifts cancel passively. No motors. No cooling. No weight penalty.

BD6™ transmits across SWIR, MWIR, and LWIR in a single element — previously three separate systems. And unlike germanium, BlackDiamond™ is Precision Glass Moldable — high-volume, scalable, dramatically cheaper.

---

**The moat**

Exclusive rights to 14 chalcogenide glass compositions from the Naval Research Laboratory. No competitor can access them.

- Phase 1: Three formulations qualified — already replacing germanium in active programs of record

- Phase 2: Six more being qualified to MRL-9 — full high-rate production readiness

Once qualified into a defense program, a material stays for the program's entire lifecycle.

---

**Three acquisitions built the complete stack**

**Visimid (2021):** Phoenix FPGA engine — turned LightPath from component supplier into systems integrator.

**G5 Infrared (Feb 2025, $27.1M):** Long-range cooled MWIR cameras. G5 booked $100M+ in new orders since acquisition — triggering GAAP earnout revaluation, creating $12.2M in non-cash charges YTD that mask real profitability.

**Amorphous Materials (Jan 2026, $7M):** Expanded maximum optic diameter from 5 to **17 inches** — unlocking space-based payloads. Already supplies glass for the F-35 targeting system and Apache Arrowhead sensor suite.

---

**Defense programs already won**

- **Lockheed NGSRI (Stinger Replacement):** Sole-sourced. Flight tests successful. 10,000 units/year at full rate. **$50M–$100M annual revenue** over 10 years.

- **Air Force SEWADS (Counter-UAS):** $30M backlog. EdgeIR™ runs Hailo-8 AI at 26 TOPS — processes video locally, transmits only target coordinates. Unjammable.

- **L3Harris Shipboard Threat Detection:** Sole-sourced. 10-year program. $10M–$20M/year.

- **Elbit Border Surveillance:** 85–90% win probability. $20M CY2026 bookings. 14-year cycle.

- **Golden Dome (Space Satellites):** Three aerospace primes in active design review. ~$16M per satellite payload.

---

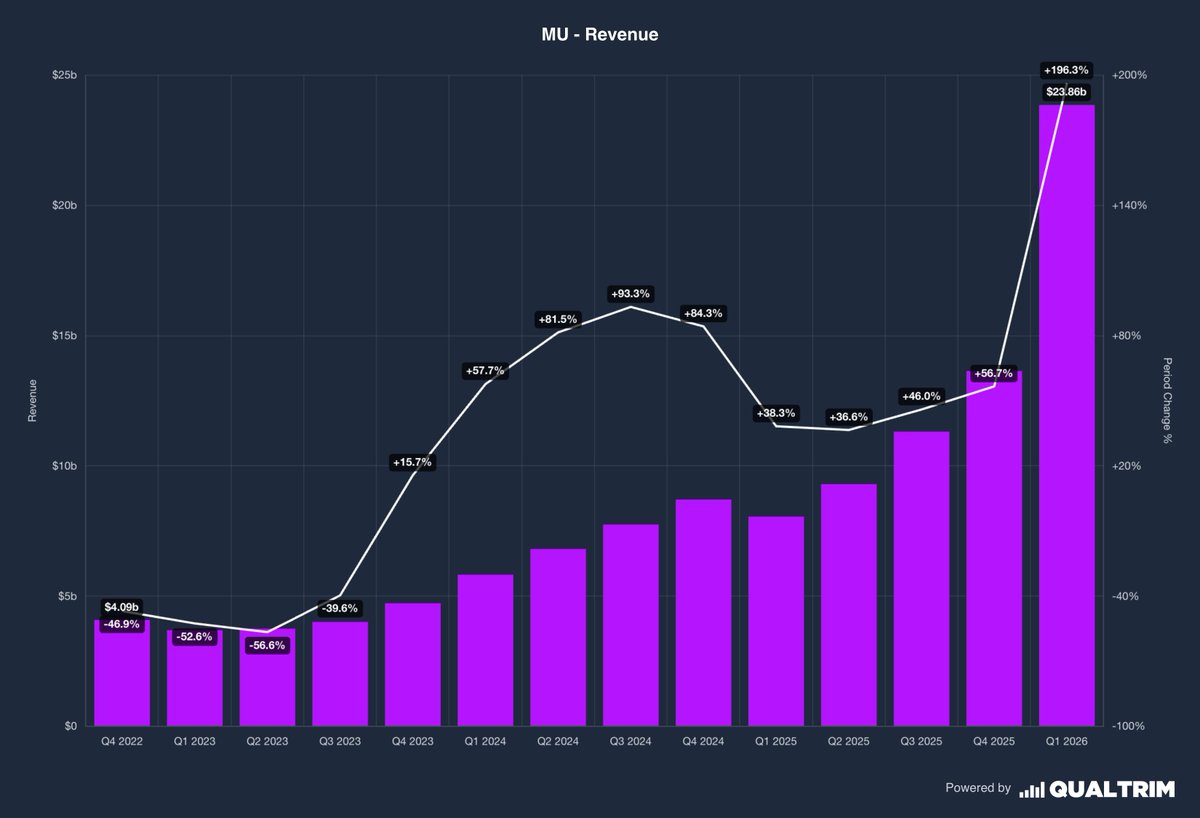

**The financials**

Q3 FY2026:

- Revenue: $19.1M — up **109% YoY**

- Assemblies & Modules: up **355% YoY**

- Gross margin: 36%, targeting 40%

- Third consecutive positive adjusted EBITDA quarter

- Record backlog: **$110.6M** — up 196% in one fiscal year

- Cash: $55.2M — up from $4.9M nine months prior

- GAAP net loss of $4.1M — almost entirely non-cash earnout revaluation

Every quant screen sees a loss-making small-cap. The loss is a direct function of G5 booking $100M+ in orders — the better the business performs, the worse the income statement looks.

That disconnect is the entry point.

---

Priced as a commodity optics company.

It is the domestic infrared monopoly the entire U.S. defense industrial base is legally mandated to use by 2030.

The deadline doesn't move. The alternatives don't exist.

---

*Not financial advice. Do your own due diligence.

English