Asymmetric ventures 🇪🇺🇪🇸 retweetledi

Asymmetric ventures 🇪🇺🇪🇸

713 posts

Asymmetric ventures 🇪🇺🇪🇸

@Value_Europe

Investor looking for asymmetric investments in Europe and North America - Not investment recommendation ⛔️ | CFA Charterholder

Spain🇪🇸 Katılım Ekim 2022

543 Takip Edilen981 Takipçiler

Asymmetric ventures 🇪🇺🇪🇸 retweetledi

Added 56 new stock write-ups to the site (pt 4):

@divfinsanalyst (earnings) - $NDAQ, $HOOD

@Delta9Echo - $NOW (overview)

@nicknemo17 - $ARCC (deep dive)

@SingularityRes - $MOD

@that_stocks_guy - $ACRM.L

@Value_Europe - $MCO

@snikhs2 (earnings) - $SPOT, $GOOG, $MRDN, $BKNG

English

Asymmetric ventures 🇪🇺🇪🇸 retweetledi

Asymmetric ventures 🇪🇺🇪🇸 retweetledi

@pobremillenial Con la edad de jubilación en los 67 y subiendo... no nos queda otra que hacer muy bien las cosas durante toda nuestra vida adulta (salud, físico y dinero), poder decir basta antes de esas edades, y poder disfrutar bien y en paz de esos últimos años!

Mucho ánimo a tu padre.

Español

@GutierrezCap_ Aunque si hay ventas forzosas, hay mas activos en el mercado, posibilitando el traspaso de activos. Interesante..

Español

@GutierrezCap_ Por otro lado está la administración de ese patrimonio - ahorro en mínimos se explica por una sociedad de consumo que prefiere el consumo actual a crear patrimonio a largo plazo

Español

Por primera vez he leído un artículo que me ha hecho cambiar mi opinión sobre la posibilidad de una recesión/estanflacion.

Decía, que el ahorro está en mínimos como resultado de la monopolización de la economía por la población más envejecida que acumula la mayoría de los activos, pero que cuando esos activos se transfieran a sus herederos el ratio de ahorro se normalizará, y con ello el consumo y la productividad debido al reparto de la acumulación del capital.

Me ha parecido interesante la idea de que no estamos en recesión, sino que estamos en una de los momentos menos equitativos de la historia de la economía.

¿Conocéis alguna otra razón por la cual debería ser bullish? Quiero asegurarme de no estar sesgado… aunque debo decir que me está costando porque no encuentro nada.

Español

Asymmetric ventures 🇪🇺🇪🇸 retweetledi

No es sostenible un mercado en máximos históricos con un petróleo completamente disparado, no se están cotizando correctamente los riesgos de inflación que inevitablemente dispararán las segundas rondas.

Español

Asymmetric ventures 🇪🇺🇪🇸 retweetledi

Mejora continua? Búsqueda de la excelencia? Atención al detalle? Civismo? Paciencia?

Eso ya no existe con la gente con los cerebros fritos y la sociedad en declive.

Español

Asymmetric ventures 🇪🇺🇪🇸 retweetledi

The name of the company… NewBird AI. It is a cutting-edge, AI-native cloud infrastructure firm out of- well, they used to be out of San Francisco making sneakers, but forget that, John- they are now awaiting imminent deployment of next-generation GPU compute clusters that have both massive enterprise and consumer applications. Now, right now, John, the stock trades on the Nasdaq at about the price of a cup of coffee. And by the way, John, our analysts indicate it could go a heck of a lot higher than that. And John- one more thing- they're up 160% just today

English

Asymmetric ventures 🇪🇺🇪🇸 retweetledi

Thanks, Altay! I really appreciate the open-mindedness.

We certainly didn't take this position lightly. My firm has spent hundreds of hours tearing down the $SKYH model. We’ve gotten to know the entire management team, met directly with the airport directors at their leased airports, and interviewed several of their ultra-high-net-worth tenants.

Interesting fact on that front: Lane Bess (former CEO of Palo Alto Networks) was actually so impressed after becoming a tenant that he went out and purchased a material equity stake in the company. When the billionaire customers love the product so much that they buy the stock, it's usually a pretty good sign!

You are 100% right to be deeply skeptical of any SPAC, but every once in a while, a SPAC actually delivers. Not all of them are garbage.

Cheers, and let me know if you ever want to bounce ideas around in the future!

English

Asymmetric ventures 🇪🇺🇪🇸 retweetledi

$SKYH

If management confirms on the Q4 call next Thursday that Miami Phase 2 is opening in April it would prove that since hiring Phil Amos last June, $SKYH is now completing locations in ~11–12 months after receiving NTP.

Based on the November press release, Salt Lake is expected to receive construction permits in the coming days of November.

If that happens, the timeline likely shifts:

• Addison: Q1 2027 → Q4 2026

• Salt Lake: Q1 2027 → Q4 2026

And if management confirms Orlando construction permits were received, that would likely pull forward:

• Orlando: Q2 2027 → Q1 2027

Execution speed is clearly accelerating.

Disclosure: I may buy or sell shares at any time. Not investment advice.

English

Initially, they were supposed to protect the world against bad uses of AI - Now, it seems they just don't care of anything but the valuation of the company

Chief Nerd@TheChiefNerd

🚨 SAM ALTMAN: “People talk about how much energy it takes to train an AI model … But it also takes a lot of energy to train a human. It takes like 20 years of life and all of the food you eat during that time before you get smart.”

English

Asymmetric ventures 🇪🇺🇪🇸 retweetledi

$SKYH

Based on the last 12 monthly construction reports, last 10q and transcript, the company is now building locations about every 11-12 months after receiving NTP. We will see a new location about every 1.9 months for 2026 and 2027. We will also see a few “pull-forward” announcements assuming NTP is received on a prompt basis from each municipality.

The first location that will prove this is Miami in April. Addison projected for Q1 2027 will be pulled from 2027 to Q4 2026.

English

How can politicians act like this. It's unbelievable how stupid these measures are and all the wealth they will destroy.

They will say they are targeting the wealthiest people in the country, but in reality, they are destroying the wealth of low and mid income citizens.

Aakash Gupta@aakashgupta

The Netherlands was forced into taxing unrealized gains. Their Supreme Court struck down the old Box 3 system in 2021. The previous framework assumed a fictional rate of return on your assets and taxed you on profits you never actually made. The court ruled it unconstitutional. That left a €2.3 billion annual hole in the Dutch treasury and no legal way to tax investment returns at all. So parliament passed the replacement with 93 votes (needed 75). Multiple parties that voted yes publicly said taxing unrealized gains was not their preferred approach. They backed it because the alternative was collecting zero on investment returns indefinitely while refunding €1.2 billion in overpaid taxes from the old illegal system. The math on what happens next is predictable. France ran this experiment for 20 years. Between 1988 and 2007, an estimated €200 billion in capital fled the country. 60,000 millionaires left between 2000 and 2017. The wealth tax cost France roughly €7 billion in annual fiscal shortfall, about twice what it actually collected. Macron killed it in 2018. The Netherlands just approved something far more aggressive. France taxed total wealth at progressive rates starting around 0.5%. The Dutch version taxes annual paper gains at a flat 36%. Your portfolio goes up €100,000 on paper, you owe €36,000 in cash. You haven’t sold a single share. The government acknowledged this liquidity problem directly, which is why they exempted real estate and startup shares. Stocks, bonds, and crypto get no such protection. The bill still needs Senate approval. Implementation targets 2028. But the EU has free movement of capital and people. Portugal, Malta, and Cyprus are a short flight away. This matters for the US because unrealized gains taxation keeps surfacing in American policy proposals. California has a wealth tax ballot initiative that’s already triggered an estimated $2 trillion in capital flight threats. The Biden administration proposed taxing unrealized gains above $100M. The Netherlands is about to become the first country to broadly implement one at scale. France spent 20 years proving the model fails. The Netherlands is about to rerun the experiment at 36%.

English

Asymmetric ventures 🇪🇺🇪🇸 retweetledi

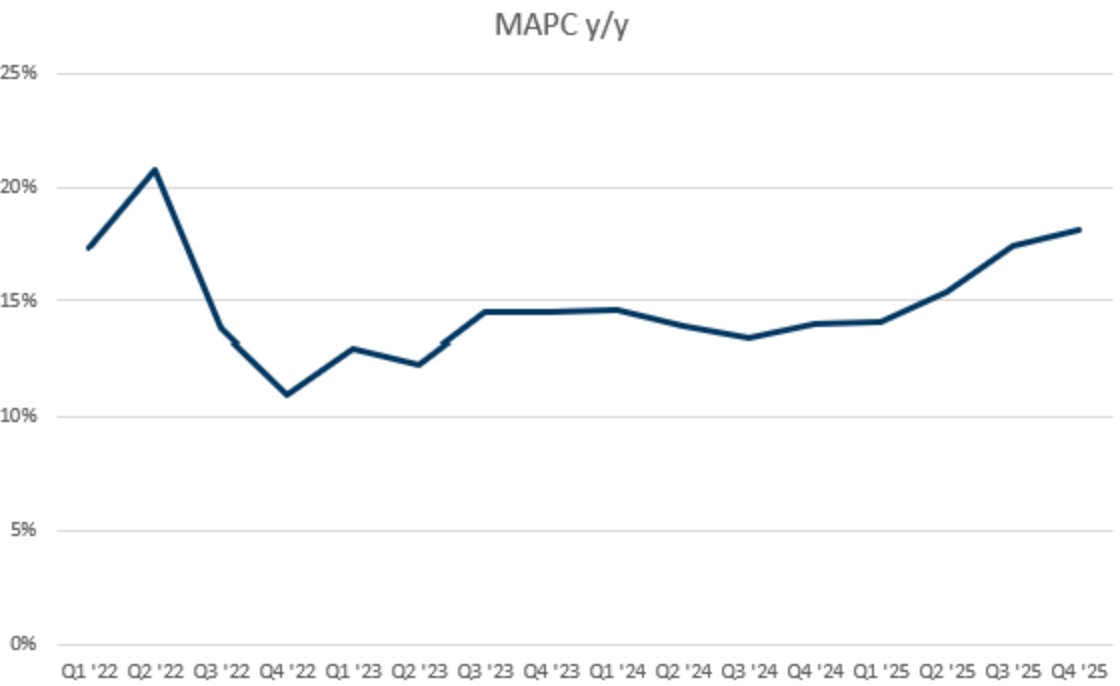

I own a material amount of $UBER, and if the wife thought she could stop hearing about it, she was WRONG. One of the first things that should jump out to you from 4Q results is that user counts were very strong. The first chart way down below is quarterly MAPC y/y, which the last several quarters has been accelerating. Not bad for a company at such massive scale and n.b. that most SS models assume MAPC growth rates decelerate, as that's a natural starting point assumption.

There are several squishy reasons one could imagine why MAPC might be outperforming. Generally speaking, two sided marketplaces benefit from liquidity so they often have accelerating returns to scale. Eats is a more luxury good so it should be later in its maturation curve. Int'l expansion. Millennials are fiscally irresponsible morons who never got drivers licenses. Etc. Given I'm a HF guy though, we'll use data.

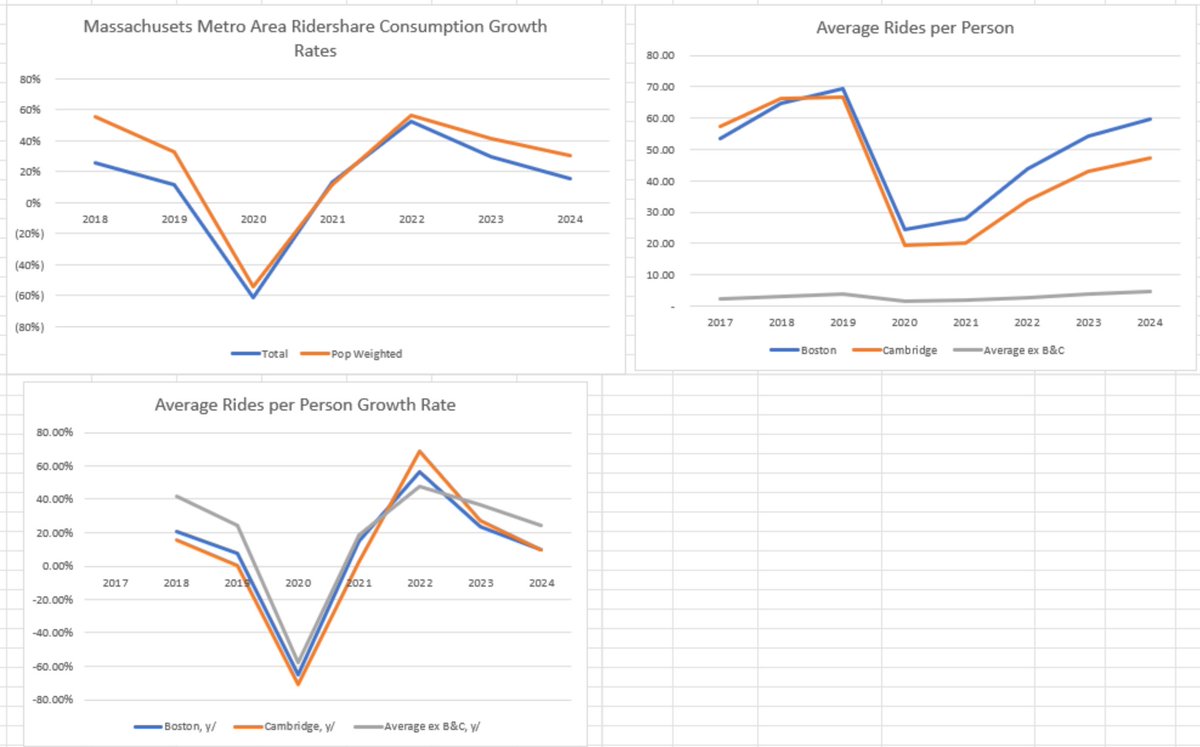

For this exploration we are going to use Massachusetts reported annual ride share data by metropolitan area, which is one of my favorite reported alt data sets I've ever seen. Just fantastic insights within it. Anyways, Massachusetts rideshare consumption rose 15% in 2024. It will not shock you to learn that many people in Massachusetts live in Boston. Boston + Cambridge are 11% of the population, and that excludes all the assoicated big suburbs like Brookline, Revere, Newton, etc all of which are ~1% each etc. It will also not shock you to learn that generally speaking, Boston is rich, and many of the out of the way parts of Masachusetts are shitholes.

If we simply decompose Massachusetts ride share consumption growth into Boston, Cambridge, and ex-B+C we see that B&C are growing ride share consumption around 10% per year. But the other regions are growing at 22%!!!! Including some real standouts. Tier 2 cities like Worcester and Lowell are growing 25% and 21% y/y. There is effectively a 12 point gap of outgrowth in the less dense areas.

We can then look at per person consumption. Boston contributes 59.6 rides per person per year. Cambridge contributes 47 rides per year. Meanwhile the average Massachusetts ex-B&C municipality contributes 4.7 rides per person per year. This is dragged down by a bunch of rural areas at ~0 per person, but the Tier 2 cities of Worcester and Lowell are at 11x and 3.7x per person per year respectively. So on an order of magnitude, ride share intensity is ~5-10x+ higher in the densest cities.

Meanwhile, per person consumption for Boston & Cambridge is growing around 9.5% (n.b. this approximates its total growth rate. This makes sense because intuitively no shit everyone in B&C has Uber installed on their phone). But the average per resident growth rate in ex-B&C areas is 24% (!!!). In our Tier 2 city examples of Worcester & Lowell it's 26% and 34%. Massachusetts regional populations are (probably) not growing 24% per year on average, so here we have our statistical indication that indeed a lot of people are still only starting to incorporate rideshare into their life in a meaningful way.

There are three primary takeaways here.

The first is that growth is effectively de-risked for the intermediate term. Waymo, Tesla, and friends could drive B&C growth to literally 0 and there would still be ~7% total growth for Massachusetts rides (51% of the total ride base growing at ~15% per year). Waymo, $TSLA, and friends are not going to drive B&C consumption to flat in 2026 given that the services don't exist yet and won't until late 2026 at the very earliest. So even in big, mature markets like Boston, double digit KPI growth is extremely likely. That's honestly amazing.

Secondly, the TAM is fucking huge. Unbelievably large. The vast majority of people in Massachusetts don't use ride share at anything approximating the usage of the urban centers, let alone the usage of a HF asshole in New York. AV will collapse a lot of urban adjacent ride share profiles towards the urban which alone is a massive usage expansion. And that's before we unlock material new use cases from AV (longer commutes, more travelign to the Cape, kids can travel unsupervised to friends', less drunk & high driving, etc).

Thirdly and perhaps most importantly, contrary to popular fears, Uber has time. The predominance of their growth is in the areas that are LEAST susceptible to immediate AV disruption by $GOOGL and TSLA. Google and TSLA very clearly in 2026 and 2027 will not and cannot reach the Worcestors and Lowells of the world, let alone the random suburbs on the Cape or Nantucket (growing 20% y/y) or even the big bulky Boston suburbs like Brookline (growing 12% y/y). Uber has many partners. LCID, May, Wayve, WeRide, Pony, NVDA, Waabi, STLA, Nuro, Motional. These are all names that are EXPLICITLY adding and going to add AVs to the Uber network.

Pick a timeline for when you believe Waymo or TSLA will be able to start meaningfully generalizing their fleets to the ex-B&C areas we've been discussing. 2027 at ealiest? 2028? 2029? Well then, as long as one or some of the above listed partners have started to scale their own AVs into the Uber network by that point, then Uber's AV internalized outlook is also extremely strong. Based on the realized progress and steps thus far, that's extremely likely. It's literally already happening. You can call a car via Avride in Dallas. May Mobility in Texas. WeRide in half the Mid East. Baidu too today. Wayve in London expected this spring. LCID allegedly going to onramp like 6k cars into the Uber network. By the time Waymo and TSLA start reaching the long tail of Uber growth & TAM expansion, all these partners will be competing too, and they'll be competing via the Uber network's liquidity.

We haven't discussed delivery at all here, but note it has a lot of the same characteristics in terms of growth that it is still a relatively a low penetration luxury good that benefits from rising marketplace two sided liquidity. And as it grows mind share it becomes stickier + perpetuates lifestyle changes that ingrain it further into consumption patterns

We also haven't discussed advertising which is 2bn sales growing 50% y/y (lol)

We also haven't discussed that Uber validly has a differentiated long term value prop via the complete integration of mobility + delivery + freight.

So we have a company that has derisked DD+ topline growth for at least two years, that trades at an ~6.5% forward FCF yield, that is buying back ~1% of its market cap per quarter, that has 9bn of investments held, that is ~0.5x levered, that has clear visibility into its TAM growing enormously, that grows EBITDA at almost 30% incremental margins, that has around 20% FCF margins, that has no Claude disruption risk, and that has a call option on being the absolute top winner in the space

Time to make some money!

English