Vin

2.3K posts

Vin

@VinTrader1

Economics/finance research; Ex-global/local banks, Macro Investor

Katılım Aralık 2019

556 Takip Edilen89 Takipçiler

market is so kind to some stocks for very long time. never understood it .. sales growth 2%, profit de growth and PAT margin less than 3% but continues to give PE over 100.

English

@Live_Well_Thee @rajuidesai And authum is now looking to exit yellow diamond (prataap snacks) that they acquired with madhu kela.

English

MIRC ELECTRONICS Ltd : CMP: 43.40

1) Mcap - 1604 Cr

2) Beautiful Sales of 750 Cr

3) FV 1, which I don't like but Mcap is too small, particularly when Authum Invst and Infra take stake.

If Authum has not taken stake, I would have not discussed Mirc here at FV 1 stock..

4) Authum entry is a trigger for me, that they will turnaround MIRC ELECTRONICS ltd, like they did with Nitco Ltd.

5) MIRC and Nitco has similarity, both have excellent sales.

6) Authum Invst stake of 21.25% is no small stake. They invested around 131 Cr when Mcap was much less....Now putting 131 Cr is not for nothing. Rs 131 Cr is big, bigger then many SME Mcap!!

Take the HINT!!

7) Co is going to raise fund via Equity, Warrants or QIP.

8) You are getting a Brand , Onida, for just 1600 Cr!!

Neighbor's Envy, Owners Pride!!

Do your DD. Take your Call!

English

@Bullish2023 Assumption being that war would get over n things will normalise

English

PPFAS in April increased holding in large cap IT stocks

TCS holding up by 28%

infosys holding up by 34%

HCL Tech holding up by 35%

Also again it started adding IGL but why?

English

Nicety should not be the response against brutality.

Prithviraj Chauhan spared Muhammad Ghori and we all know how it ended for him.

English

If you see in most European countries, People decorate their balconies nicely with flowers... these are normal average middle-class households, not utlra-rich ones.

However, in India, balconies of ultra posh residences

( costing several crores) are filled with clothes hanging for drying !!

What happened to our sense of beauty & aesthetics?

English

@PareshBabaria3 @rishibagree Sadly being leftist is fashionable in this country and also in many other parts of the world. Some of it is changing now ..

English

@rishibagree This is similar to what now raga is doing at Nicobar island , everyone medha patkar or raga wants to benefit personally at expenses of general public like us ,surprising is they are not accountable at all .why suo motto court should not take actions , stopping progress of India

English

Remember how foreign-funded 5-star activists like Medha Patkar tried their level best to deprive the Kutch region of Narmada water, until Modi called their bluff.

Today, the same dam irrigates 3 states & provides drinking water to millions of Indians

English

@Bullish2023 @jaganmsna If they have the to sellindia banks is their top holding

English

@jaganmsna why FIIs selling in this counter is little puzzling? even recent RBI annoucement of ECL has no impact on ICICI Bank.

English

whats wrong with icici bank? everything looks positive but stock down ~10% from result day. Sept 2024 it was at 1290 so 1.5 years and nothing inspite of everything +ve.. what this market doing?

English

Vin retweetledi

#Nifty can move towards the target of 24190 given yesterday, for today it’s better to use dips to 24040 & reversal on 5 mins as buying opportunity for move to 24190 - 24230 levels, support is at 23970

English

@Bullish2023 Murthy once said - share bad news upfront n good news slowly. Hcl tech did just that !!

English

HCL Tech mgmt ne dhoti phaad ke rumaal bana diya.. kya jarurat thi enta bakwaas karni ki.. waisse hi IT sector ke sitaare gardish mein chal rahe hai aur upar se kharab result pe bakwaas commentary... esse kahte hai...bacche ki jaan lena... ab to Oct tab ka hisaab kar diya..

हिन्दी

@KutnitiFNDTN @TVMohandasPai To his credit he tried writing on local issues of Singapore n HK earlier but failed miserably.

English

📜BIOGRAPHY OF Andy Mukherjee

Background: Indian

Position: Opinion Columnist for The Bloomberg

Based in: Hong Kong

Education: Delhi University, Bachelor of Journalism (Hons.), Mass Communication (with minor concentration in economics and political science)

🏅Honors: Member of the 0%er Club of India by Kutniti Foundation - Club of journalists dedicating their life to write about India but never anything good

English

Andy Mukherjee is NOT your traditional anti-India journalist

They write against Indian Society

He writes against Indian Economy

And for Bloomberg, the most critical financial media

🇮🇳 188 ARTICLES about INDIA in 3 years (5 per month!)

🟢95% Negative 🟡4% Neutral 🔴1% Positive

English

@EmergingRoy @menakadoshi Bmberg has some desis who for the longest time can only think unidirectional - disparaging india simply coz that narrative sells nicely in west n more recently also to chinese audiences. These guys hv built careers on it!! Ask them to write on any other topic n they fumble!!

English

@menakadoshi ???

Samir Arora@Iamsamirarora

What really upset me last week was this article on Bloomberg professional which casually mentioned something like: Due to weak INR, RBI/govt can restrict capital outflows by FIIs. I asked them the source of this and obviously there is no response beyond acknowledgement of my message. This has never happened and any India watcher would know this as being totally outlandish but it was casually put into the article on FX outflows without further explanation.

QAM

Vin retweetledi

@Karansamal @AlgoTest_in Great job! Let's connect if looking to scale up.

English

2 Years📊

Capital deployed: ₹21 Lakhs

Gross: 57.7%

Net: 43.3%

One of the three family accounts I am currently handling.

Pure algo trading in Nifty & Banknifty options using @AlgoTest_in

Always open to working with serious traders & discussing ideas🤝

DM to collab

#algotrading

English

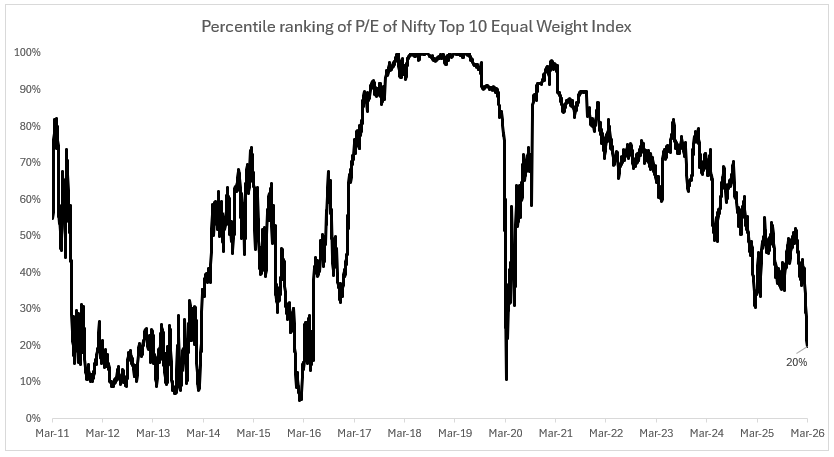

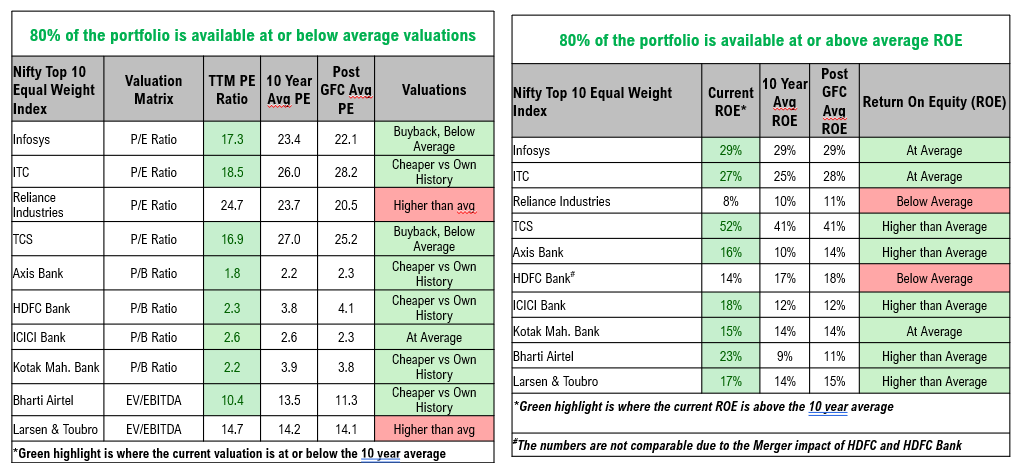

Markets often test conviction the most when narratives turn negative.

Currently, the Top 10 stocks are trading at valuations that are among the lowest seen in the past decade. On a percentile basis, the P/E of Nifty Top 10 Equal Weight Index stands at 20th percentile (data considered since March 2006), a level last observed in 2016, a period marked by heightened pessimism and muted growth expectations for these businesses. However, these are the businesses which have seen these business cycles time and again, emerging stronger over time.

That said, the real challenge for investors is behavioural, not analytical. When sentiment is weak and narratives are unfavourable, acting on opportunity becomes inherently difficult. Yet it is precisely during such phases that disciplined allocation tends to be most rewarding. The opportunity is visible.

The question remains - can we act when the opportunity comes?

English

@kyalashish Visit other cities of Rajasthan also jodhpur udaipur n jaisalmer

हिन्दी

#Nifty is showing clear selling pressure as a large bearish weekly candle has formed. For a possible reversal, watch the Supertrend(10,3) on the hourly chart. The key date is 17 March, and the 11:00 AM time cycle on Monday should be observed closely for intraday moves.

English

Hard to believe the extent of fall in some of these stocks!!

The entire auto anc pack has completely crashed, valuations started to look attractive

Personally I like -

Lumax twins

Sansera

Pricol

GNA axles

Jamna auto

-----

Will start to add slowly and finish by end of March..

English

Timepass talk on Sunday

Based on feedback that the ‘Timepass Talk on Sunday’ felt a bit long, I’m streamlining it to 5 concise updates

1. Cables & Wires - Wires that are absolutely on fire!

You remember the Havells tagline: “Wires that don’t catch fire.” Ironically, right now the entire C&W sector is on fire, but for the right reasons.

Apparently, it's the new frontier of DC and AI story! India is estimated to build ~8–10 GW of data-center capacity by 2030, and cables are not a small line item in that build-out.

According to Anil Gupta (CMD, KEI Industries), cables & wires account for ~3–5% of a data-center project’s cost. That translates to roughly ₹3,500–4,000 crore of cable demand for every 1 GW of capacity.

With ~11–13% market share, KEI management believes it can capture ₹2,500–3,000 crore of revenue from this segment over the next 5–6 years!

In the latest concall, the company also guided for “20%+ CAGR over the next 3–4 years.”

And this isn’t just a KEI story, the tailwind applies across most organised cable manufacturers.

The opportunity is real. The growth visibility is improving.

But the market already knows this, and valuations definitely reflect it!

2. GRSE - the revenue cycle is getting bigger

Just to understand the scale change:

FY22 revenue: ₹1,754 crore (then a record year); Q3FY26 revenue alone: ₹1,896 crore

They are likely to close FY26 at ₹6,500+ crore revenue.

So, revenues have moved from ₹1,754 crore → ₹6,500+ crore in ~4 years, and the stock price has broadly followed, rising ~6–7x.

GRSE is expanding it's capacity, building JVs/Partnerships and the company expects to end FY26 with an order book of ~₹50,000 crore.

What the next cycle looks like:

FY27: Peak revenue year (P-17 Alpha execution); FY28: a bridge year between two shipbuilding cycles; FY29-35: Next cycle

If P-17 Bravo and other orders come thru, we would then be looking at another FY22-26 sort of growth (and returns).

The investing takeaway: GRSE is not a linear growth story. It is a cycle-driven compounding story.

Buy during weak phases → hold through the build cycle → earnings catch up later.

Another name in this space is Swan Defence and Heavy Industries!

3. Axiscades - from billing hours to building missiles

Why is Sansera stock price running away? Because market is doing the re-rating in anticipation of product mix change (Auto to ADS) but the revenue share of ADS is still low. Yet, market is recognizing the future event.

For Axiscades, revenue mix today is 61% services / 39% products, but they expect it to flip by FY27. That matters because services earn ~18% margins, while product solutions earn 25–30%+ margins.

Accordingly, consolidated EBITDA margins may rise from ~17% to ~20%, with management guiding 40–50% EPS growth in FY27.

If Axiscades can walk the talk, they are cheaper than Dynamatic, Azad and even perhaps Sansera. At 45% growth for FY27, it's currently at 38 P/E FY27.

4. Aditya Infotech - The CCTV guys

Many industry researchers such as Frost & Sullivan, Mordor Intelligence and Fortune Business Insights estimate that the global CCTV camera market would grow in double digits and Indian market should grow in high teens.

Why? Primarily two triggers: 1) Govt and Institutional mandates and 2) Per-capita growth

We often hear how rising per-capita income drives incremental demand for healthcare and premium consumption.

In many ways, security behaves similarly to healthcare. As incomes rise, a portion of incremental earnings inevitably gets allocated to protection and peace of mind - CCTV cameras, dashcams, home surveillance systems, and related solutions.

Likewise from the government and society front, security mandates continue to increase. For ex: CBSE issued mandates about usage of CCTV deployment in classrooms, corridors, etc. Likewise State Education Depts, RBI, Railways, Road Transport, Local bodies, Hospitals and more importantly, Home Ministries have all issued mandates.

Aditya Infotech is perhaps the #1 player in India and the owner of the flagship brand CP PLUS. Valuations aren't cheap but here are enough reasons for you to study the company:

1) They are guiding to grow 30-35% in FY27 with margin expansion; 2) Capacity increasing, 3) Backward integration is in progress, 4) R&D ecosystem is getting better (incorporated an R&D center in Taiwan), 5) Entered in a strategic partnership with Qualcomm Technologies to build AI-enabled insight-driven video security solutions, 6) Strong distribution moat (800+ distributors in 500+ Cities) and 7) Structural industry tailwinds in the form of STQC certification norms, which are pushing out non-compliant imports and consolidating demand toward domestic players like CP Plus.

An alternate name in this space is Prizor Viztech!

5. Influx Healthtech

At a recent industry event, an FSSAI official made a striking observation: India’s nutraceutical opportunity could grow even faster than pharmaceuticals.

As per-capita income rises, consumer behavior changes. Healthcare spending doesn’t just increase, it shifts. People move from “treat illness” to “prevent illness.” That’s where nutraceuticals come in.

China offers a useful precedent. Around 2010, when China’s per-capita income was ~$4,500, its nutraceutical market was roughly $10–12 billion. Today, with per-capita near $14,000, the market has expanded to an estimated $70–90 billion. Rising disposable income tends to create a structural tailwind for preventive health.

Influx Healthtech operates as a CDMO across nutraceuticals, cosmetics, petcare and homecare, with ~90% of revenue still coming from nutraceuticals. Its customer base has increased from 538 in FY23 to 636 in FY25.

FY25 revenue stands at ~₹105 crore, while management is targeting ₹450–500 crore by FY29. The company is debt-free, expanding into higher-margin cosmetics and fast growing veterinary segments, and pursuing international certifications to enable exports.

Whether this translates into multi-fold growth is the real question, the opportunity is visible; the conviction has to be yours.

That's all for today! Have a great Sunday!

English

@kyalashish Excellent analysis. I always look out for ur videos n updated before taking trades

English

Vin retweetledi

#Nifty is retesting #Gann level 25361 but not a single hourly close below it so far! If it breaks short term pressure else another classic opportunity for intraday traders, check in this short video

#AKTradingGurukul

English

@Niteish_14 @grok which is this pattern according to technical analysis?

English