@danroberts0101 @NVIDIAGTC I sense their is a hidden message wrapped in these words. Curious to see what $IREN is going to announce soon 🙏

English

Vincent Janssen

629 posts

@VisionVince

Investor. Creator. Father. Building the future: BTC, AI, human dev, fin sovereignty, new ways of working. Speaker: AI, education, designing life for what’s next

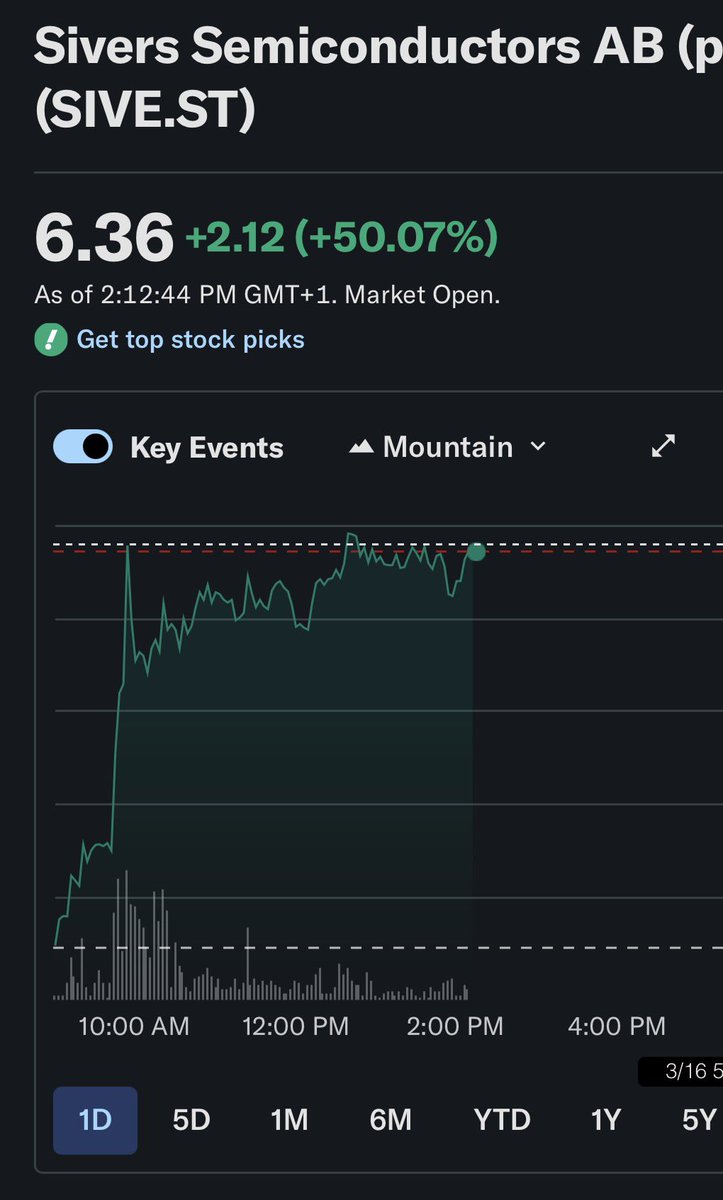

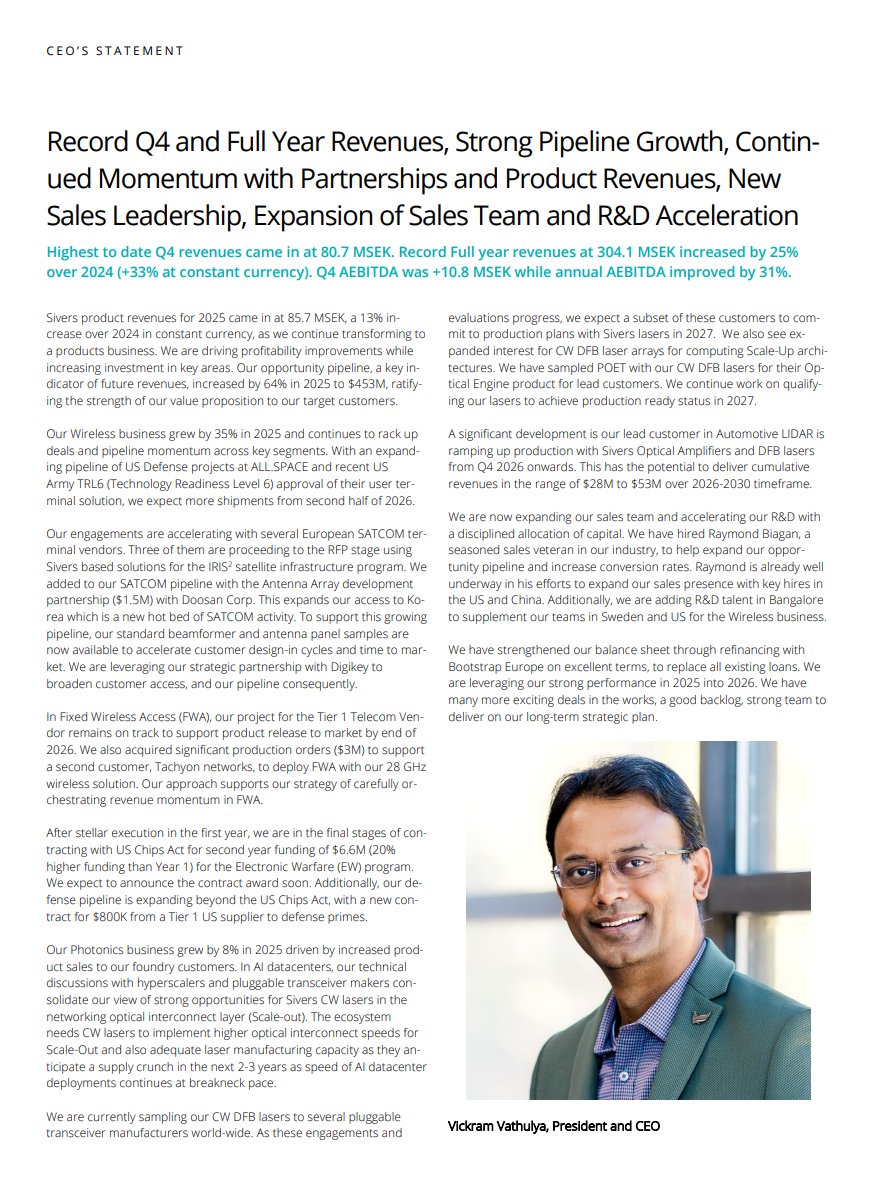

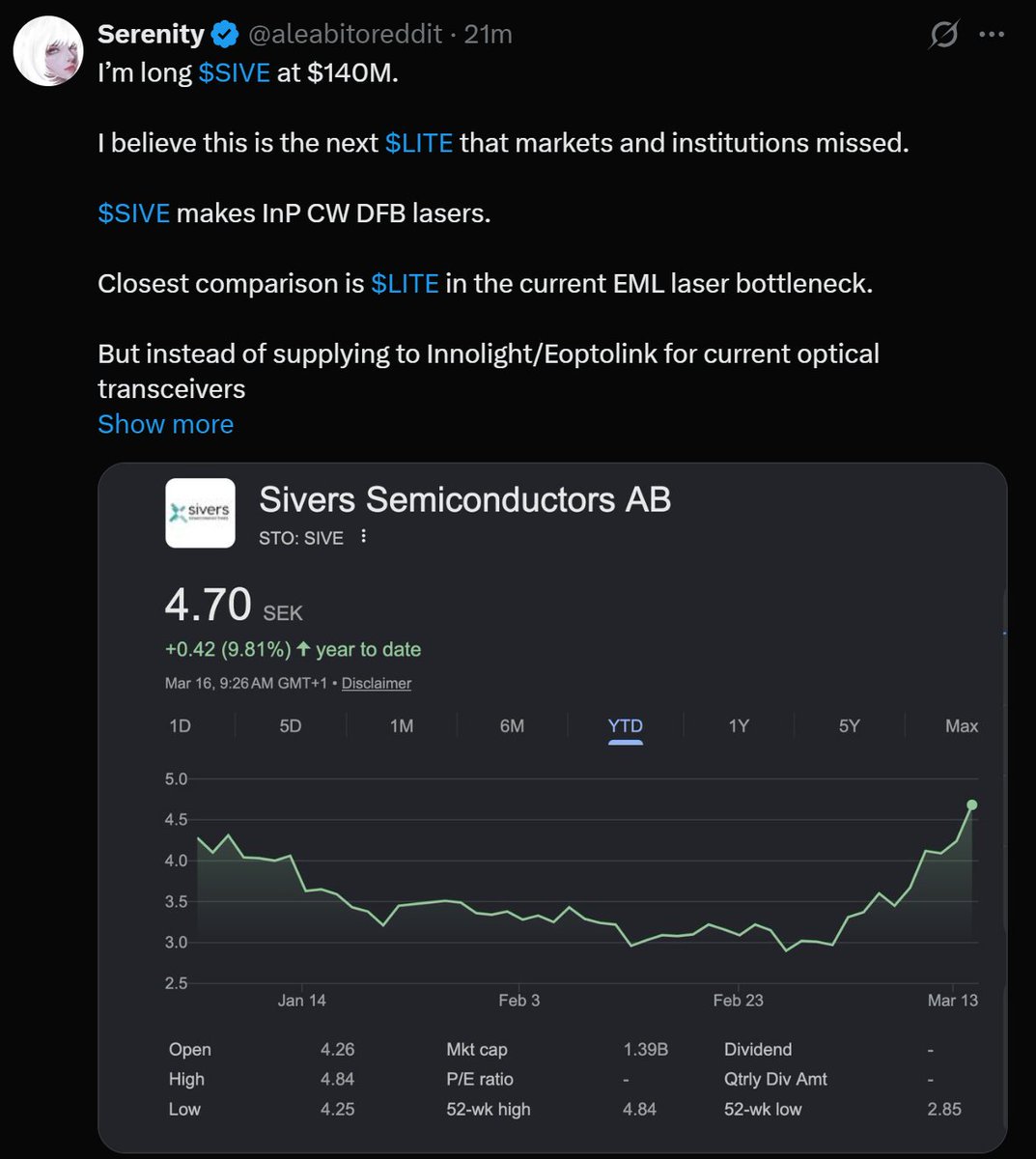

I’m long $SIVE at $140M. I believe this is the next $LITE that markets and institutions missed. $SIVE makes InP CW DFB lasers. Closest comparison is $LITE in the current EML laser bottleneck. But instead of supplying to Innolight/Eoptolink for current optical transceivers cycles. They supply the lasers to $POET Starlight, Ayar SuperNova. And others for the future CPO/silicon photonics architectures spearheaded by $NVDA. Current valuations make 0 sense to me personally. $POET is advanced packaging for $SIVE type lasers… But $POET commands worth 11x+ more than the company making the laser itself? It’s feels like valuing a more advanced $FN (~$20B) packaging at $400B when $LITE is valued at $40B. So now at $130m: - - You have a likely mini $LITE like laser supplier to Marvell Celestial + hyperscalers through $POET. - Laser supplier to Ayar ( $NVDA, $INTC ), though they do multi source with $LITE, Sumitomo, $MTSI. And other potential up and coming suppliers potentially like Lightmatter that they’ve name dropped (eg. Q2 2023 earnings). This is unconfirmed but supply chain BOM is confidential. On top, for revenue, they expected $453M "pipeline next few years”. And, they have capacity expansion through WIN: “Win Semi foundry qualification in progress for volume production from Laser designs from Sivers." Sivers feels the silicon photonics/CPO version of $LITE, with actual rapidly growing customers like Celestial through $POET, Ayar, with more to come. I wouldn’t have liked it last year, but just 3 weeks ago, they refinanced all their debt successfully to $12M convertible loan (10.85%) and a $5M term loan (12%), which cleans up debt. It’s $17m total, which feels like nothing to US markets when $AAOI is doing a $500m ATMs every other week. Best of all, this is their pure play inp laser segment for silicon/photonics + cpo. Their Lidar segment is ramping up and they have $53-138M projected revenue coming in. Downside risk: - execution (as always) - dilution to scale up capacity to compete with $LITE and others. - $LITE, $COHR competition on scale after $NVDA just gave them $4B - CPO ramp gets delayed. I have no clue how, $LWLG, a pre-revenue science project with $TSEM, is valued at $1B+ MC. Or how $POET, is worth ~9-10x more than its laser supplier. When $SIVE, the mini $LITE equivalent for CPO/Silicon photonics, is valued at $140M. I do believe this is largely undiscovered by institutions, since this is some random company in OMX Nordic Exchange (similar to micro $AXTI before I started posting about the inp substrate bottleneck). But I do think it will get a lot of institutional attention as Celestial and Ayar scale up. Especially if $POET and $SIVE gets qualified with other customers. If CPO completely replaces pluggable transceivers in the next generation of hyperscaler architectures. Sivers, with possible WIN Semi qualifcation and if they become the multi-source lasers for NVIDIA, Marvell, Intel, and Broadcom architectures, can be strongly rerated. Just as how $LITE did today going from $16 -> $622. This is just my personal thesis I'm sharing, DYOR/NFI. TLDR: InP Lasers are the current bottleneck in photonics as seen with $LITE valuations. $SIVE looks like the mini $LITE for the upcoming CPO/Silicon Photonics ramp. I personally took long position in $SIVE, as I believe they’re a large beneficiary of the upcoming silicon photonic/CPO architectural changes by $NVDA (with GTC cataylst). The upside here just way too compelling for me personally as the next possible $LITE.

I’m long $SIVE at $140M. I believe this is the next $LITE that markets and institutions missed. $SIVE makes InP CW DFB lasers. Closest comparison is $LITE in the current EML laser bottleneck. But instead of supplying to Innolight/Eoptolink for current optical transceivers cycles. They supply the lasers to $POET Starlight, Ayar SuperNova. And others for the future CPO/silicon photonics architectures spearheaded by $NVDA. Current valuations make 0 sense to me personally. $POET is advanced packaging for $SIVE type lasers… But $POET commands worth 11x+ more than the company making the laser itself? It’s feels like valuing a more advanced $FN (~$20B) packaging at $400B when $LITE is valued at $40B. So now at $130m: - - You have a likely mini $LITE like laser supplier to Marvell Celestial + hyperscalers through $POET. - Laser supplier to Ayar ( $NVDA, $INTC ), though they do multi source with $LITE, Sumitomo, $MTSI. And other potential up and coming suppliers potentially like Lightmatter that they’ve name dropped (eg. Q2 2023 earnings). This is unconfirmed but supply chain BOM is confidential. On top, for revenue, they expected $453M "pipeline next few years”. And, they have capacity expansion through WIN: “Win Semi foundry qualification in progress for volume production from Laser designs from Sivers." Sivers feels the silicon photonics/CPO version of $LITE, with actual rapidly growing customers like Celestial through $POET, Ayar, with more to come. I wouldn’t have liked it last year, but just 3 weeks ago, they refinanced all their debt successfully to $12M convertible loan (10.85%) and a $5M term loan (12%), which cleans up debt. It’s $17m total, which feels like nothing to US markets when $AAOI is doing a $500m ATMs every other week. Best of all, this is their pure play inp laser segment for silicon/photonics + cpo. Their Lidar segment is ramping up and they have $53-138M projected revenue coming in. Downside risk: - execution (as always) - dilution to scale up capacity to compete with $LITE and others. - $LITE, $COHR competition on scale after $NVDA just gave them $4B - CPO ramp gets delayed. I have no clue how, $LWLG, a pre-revenue science project with $TSEM, is valued at $1B+ MC. Or how $POET, is worth ~9-10x more than its laser supplier. When $SIVE, the mini $LITE equivalent for CPO/Silicon photonics, is valued at $140M. I do believe this is largely undiscovered by institutions, since this is some random company in OMX Nordic Exchange (similar to micro $AXTI before I started posting about the inp substrate bottleneck). But I do think it will get a lot of institutional attention as Celestial and Ayar scale up. Especially if $POET and $SIVE gets qualified with other customers. If CPO completely replaces pluggable transceivers in the next generation of hyperscaler architectures. Sivers, with possible WIN Semi qualifcation and if they become the multi-source lasers for NVIDIA, Marvell, Intel, and Broadcom architectures, can be strongly rerated. Just as how $LITE did today going from $16 -> $622. This is just my personal thesis I'm sharing, DYOR/NFI. TLDR: InP Lasers are the current bottleneck in photonics as seen with $LITE valuations. $SIVE looks like the mini $LITE for the upcoming CPO/Silicon Photonics ramp. I personally took long position in $SIVE, as I believe they’re a large beneficiary of the upcoming silicon photonic/CPO architectural changes by $NVDA (with GTC cataylst). The upside here just way too compelling for me personally as the next possible $LITE.

I’m long $SIVE at $140M. I believe this is the next $LITE that markets and institutions missed. $SIVE makes InP CW DFB lasers. Closest comparison is $LITE in the current EML laser bottleneck. But instead of supplying to Innolight/Eoptolink for current optical transceivers cycles. They supply the lasers to $POET Starlight, Ayar SuperNova. And others for the future CPO/silicon photonics architectures spearheaded by $NVDA. Current valuations make 0 sense to me personally. $POET is advanced packaging for $SIVE type lasers… But $POET commands worth 11x+ more than the company making the laser itself? It’s feels like valuing a more advanced $FN (~$20B) packaging at $400B when $LITE is valued at $40B. So now at $130m: - - You have a likely mini $LITE like laser supplier to Marvell Celestial + hyperscalers through $POET. - Laser supplier to Ayar ( $NVDA, $INTC ), though they do multi source with $LITE, Sumitomo, $MTSI. And other potential up and coming suppliers potentially like Lightmatter that they’ve name dropped (eg. Q2 2023 earnings). This is unconfirmed but supply chain BOM is confidential. On top, for revenue, they expected $453M "pipeline next few years”. And, they have capacity expansion through WIN: “Win Semi foundry qualification in progress for volume production from Laser designs from Sivers." Sivers feels the silicon photonics/CPO version of $LITE, with actual rapidly growing customers like Celestial through $POET, Ayar, with more to come. I wouldn’t have liked it last year, but just 3 weeks ago, they refinanced all their debt successfully to $12M convertible loan (10.85%) and a $5M term loan (12%), which cleans up debt. It’s $17m total, which feels like nothing to US markets when $AAOI is doing a $500m ATMs every other week. Best of all, this is their pure play inp laser segment for silicon/photonics + cpo. Their Lidar segment is ramping up and they have $53-138M projected revenue coming in. Downside risk: - execution (as always) - dilution to scale up capacity to compete with $LITE and others. - $LITE, $COHR competition on scale after $NVDA just gave them $4B - CPO ramp gets delayed. I have no clue how, $LWLG, a pre-revenue science project with $TSEM, is valued at $1B+ MC. Or how $POET, is worth ~9-10x more than its laser supplier. When $SIVE, the mini $LITE equivalent for CPO/Silicon photonics, is valued at $140M. I do believe this is largely undiscovered by institutions, since this is some random company in OMX Nordic Exchange (similar to micro $AXTI before I started posting about the inp substrate bottleneck). But I do think it will get a lot of institutional attention as Celestial and Ayar scale up. Especially if $POET and $SIVE gets qualified with other customers. If CPO completely replaces pluggable transceivers in the next generation of hyperscaler architectures. Sivers, with possible WIN Semi qualifcation and if they become the multi-source lasers for NVIDIA, Marvell, Intel, and Broadcom architectures, can be strongly rerated. Just as how $LITE did today going from $16 -> $622. This is just my personal thesis I'm sharing, DYOR/NFI. TLDR: InP Lasers are the current bottleneck in photonics as seen with $LITE valuations. $SIVE looks like the mini $LITE for the upcoming CPO/Silicon Photonics ramp. I personally took long position in $SIVE, as I believe they’re a large beneficiary of the upcoming silicon photonic/CPO architectural changes by $NVDA (with GTC cataylst). The upside here just way too compelling for me personally as the next possible $LITE.

If you don’t have the full photonics map yet, get it here: yiazou.com/photonics Upstream: materials like $AXTI, $SOI, $IQE.. Foundries: $TSEM, $GFS, $STM.. Components: $COHR, $LITE. Modules: $AAOI, $AVGO, $MRVL feeding $NVDA AI datacenters. and moving downstream..

I’m long $SIVE at $140M. I believe this is the next $LITE that markets and institutions missed. $SIVE makes InP CW DFB lasers. Closest comparison is $LITE in the current EML laser bottleneck. But instead of supplying to Innolight/Eoptolink for current optical transceivers cycles. They supply the lasers to $POET Starlight, Ayar SuperNova. And others for the future CPO/silicon photonics architectures spearheaded by $NVDA. Current valuations make 0 sense to me personally. $POET is advanced packaging for $SIVE type lasers… But $POET commands worth 11x+ more than the company making the laser itself? It’s feels like valuing a more advanced $FN (~$20B) packaging at $400B when $LITE is valued at $40B. So now at $130m: - - You have a likely mini $LITE like laser supplier to Marvell Celestial + hyperscalers through $POET. - Laser supplier to Ayar ( $NVDA, $INTC ), though they do multi source with $LITE, Sumitomo, $MTSI. And other potential up and coming suppliers potentially like Lightmatter that they’ve name dropped (eg. Q2 2023 earnings). This is unconfirmed but supply chain BOM is confidential. On top, for revenue, they expected $453M "pipeline next few years”. And, they have capacity expansion through WIN: “Win Semi foundry qualification in progress for volume production from Laser designs from Sivers." Sivers feels the silicon photonics/CPO version of $LITE, with actual rapidly growing customers like Celestial through $POET, Ayar, with more to come. I wouldn’t have liked it last year, but just 3 weeks ago, they refinanced all their debt successfully to $12M convertible loan (10.85%) and a $5M term loan (12%), which cleans up debt. It’s $17m total, which feels like nothing to US markets when $AAOI is doing a $500m ATMs every other week. Best of all, this is their pure play inp laser segment for silicon/photonics + cpo. Their Lidar segment is ramping up and they have $53-138M projected revenue coming in. Downside risk: - execution (as always) - dilution to scale up capacity to compete with $LITE and others. - $LITE, $COHR competition on scale after $NVDA just gave them $4B - CPO ramp gets delayed. I have no clue how, $LWLG, a pre-revenue science project with $TSEM, is valued at $1B+ MC. Or how $POET, is worth ~9-10x more than its laser supplier. When $SIVE, the mini $LITE equivalent for CPO/Silicon photonics, is valued at $140M. I do believe this is largely undiscovered by institutions, since this is some random company in OMX Nordic Exchange (similar to micro $AXTI before I started posting about the inp substrate bottleneck). But I do think it will get a lot of institutional attention as Celestial and Ayar scale up. Especially if $POET and $SIVE gets qualified with other customers. If CPO completely replaces pluggable transceivers in the next generation of hyperscaler architectures. Sivers, with possible WIN Semi qualifcation and if they become the multi-source lasers for NVIDIA, Marvell, Intel, and Broadcom architectures, can be strongly rerated. Just as how $LITE did today going from $16 -> $622. This is just my personal thesis I'm sharing, DYOR/NFI. TLDR: InP Lasers are the current bottleneck in photonics as seen with $LITE valuations. $SIVE looks like the mini $LITE for the upcoming CPO/Silicon Photonics ramp. I personally took long position in $SIVE, as I believe they’re a large beneficiary of the upcoming silicon photonic/CPO architectural changes by $NVDA (with GTC cataylst). The upside here just way too compelling for me personally as the next possible $LITE.

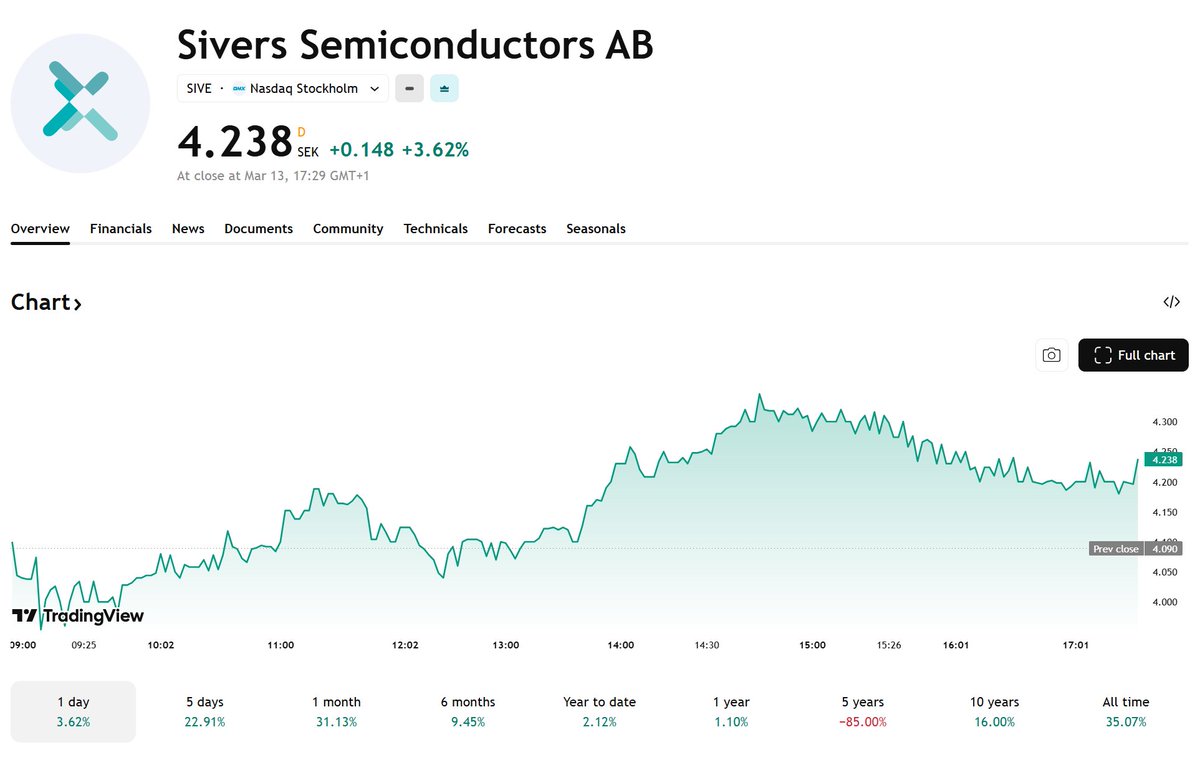

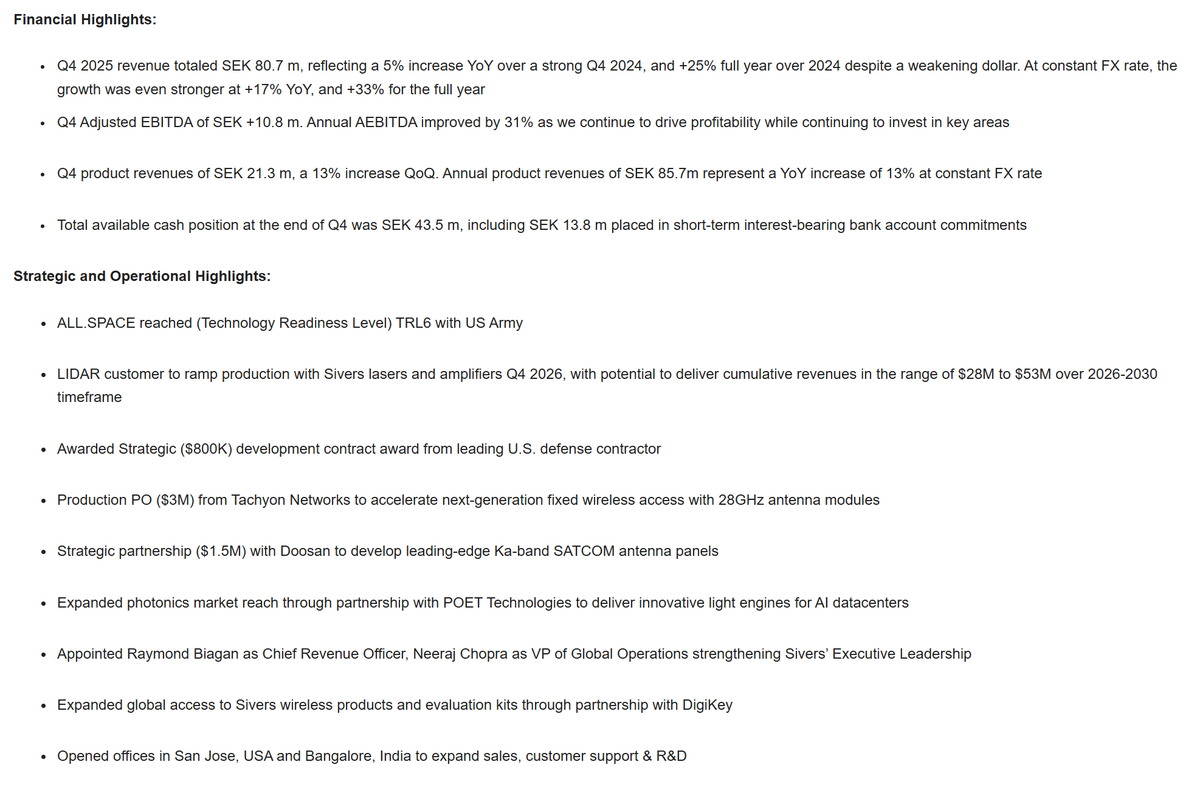

$SIVE Sivers Semiconductors: The Photonics Inflection In the semiconductor world, real alpha is found where physics hits a wall. Today, that wall isn’t GPU compute power - it’s interconnect bandwidth. As we transition to 1.6T networking, copper is dying, and light is taking over. Sivers Semiconductors ($SIVE) is no longer just a "Swedish tech hope." It has officially transitioned from an engineering research house to a high-volume product company. 1⃣ The 1.6T AI Bottleneck: Indium Phosphide (InP) AI clusters are only as fast as the links between them. Silicon Photonics (SiPh) is the solution, but silicon cannot emit light efficiently. It needs an external "engine." ➡️The Moat: Sivers is one of the few global players capable of mass-producing InP CW-WDM laser arrays. These are the "spark plugs" for the next generation of AI transceivers. ➡️Proof of Concept: Partnership with $POET is hitting a critical milestone. Prototype External Light Source (ELS) modules for 1.6T architectures are sampling in H1 2026. ➡️The Pivot to "Standard Products": CEO Vikram Vathulya recently confirmed a strategic shift. Sivers is moving away from low-margin custom engineering toward Standard Products. This will drastically shorten "time-to-revenue" and scale margins by serving multiple customers with the same high-spec chips. 2⃣ Hard Evidence: The 2026 Contract Ramp-up Investors have long criticized Sivers for a "paper pipeline." That changed this month (March 2026): ➡️LiDAR Breakthrough: A strategic LiDAR customer (winning in both Automotive and Industrial) is ramping up in Q4 2026. Cumulative revenue potential: $53M to $138M. ➡️SATCOM & IRIS² Momentum: The Wireless division grew 33% in 2025 (constant FX). Crucially, three terminal vendors for Europe's IRIS² satellite constellation have moved to the RFP stage and are currently building prototypes using Sivers technology. ➡️US Chips Act: Sivers is using Chips Act funding not just for cash, but to accelerate the integration of their tech into US Defense "Electronic Warfare" (EW) programs. 3⃣ Financial De-Risking & The "Uplisting" Catalyst The biggest drag on $SIVE has been its balance sheet. That drag is being cut: ➡️Debt Refinancing (Feb 2026): Secured a $17M facility from Bootstrap Europe, consolidating all debt and providing a clear runway to the Q4 2026 ramp-up. ➡️The 2027 Line in the Sand: Management has set a firm target to reach full break-even/positive cash flow by the end of 2027. ➡️The US Nasdaq Spin-off: With 80% of Photonics revenue coming from the US, the plan to spin off Sivers Photonics into a US-listed entity remains the primary "valuation unlock" to capture US-style multiples (think Lumentum or Coherent). 4⃣ 2026 Guidance: The Roadmap to Pavement ➡️Opportunity Pipeline: Stands at $453M (up 64% YoY). ➡️Profitability Pivot: Q4 2025 delivered a positive Adjusted EBITDA of $1.14M. Expect this to stabilize as "Foundry Customers" (SME base business) provide a recurring revenue floor while waiting for the "Big Elephants" (AI & Auto) to join. ➡️OFC Los Angeles (March 15-19, 2026): Currently underway. Industry leaders are vetting Sivers' laser arrays. Success here is the catalyst for large-scale datacenter deployment. 👇Final Verdict Sivers is no longer a "story" stock; it is a "delivery" stock. As 1.6T networking becomes the standard for AI datacenters, the demand for Indium Phosphide laser sources is set to explode. Sivers is one of the very few companies sitting on the right IP at exactly the right time. What’s your take on the Silicon Photonics race? Are you betting on the massive, vertically integrated giants like Broadcom, or do you see the "pick-and-shovel" specialists like $SIVE capturing the real alpha in the 1.6T transition? Drop a comment below with your thoughts or ask me anything. I'm here for you. #Investing #Semiconductors #AIInfrastructure #StockPicking #Sivers #Photonics