walter tambke

198 posts

walter tambke

@WTambke

Tru steel buildings, rhino mini storage, Peach state academy daycares, fire station express car wash, Thors wine and sprints and castle dry cleaners,

Atlanta Katılım Şubat 2022

379 Takip Edilen131 Takipçiler

There's been a lot of discussion about the meaning in the delay here for $LQDA and context is important.

On the one hand, some folks would say don't read too much into timing, a judge's first priority is getting the opinion right. The judge's job is to interpret the law and not worry about anything else.

But in this case, we know the judge did seem to care about the commercial impact of his decision. We know this because he said so in the trial - calling a decision in favor of $UTHR "messy." Knowing that such a ruling would have commercial implications that would get messier over time, he asked for an expedited briefing schedule.

These two facts mean that at least at the time of the trial, he appreciated that if he was going to get to a ruling in favor of $UTHR, he better do so quickly so that the mess doesn't get bigger. Through their disguised common ownership argument, $UTHR gave the judge the option to write a short opinion in their favor.

The alternative path the judge had was to rule for $LQDA and to do so in a comprehensive manner - a 60-80 page opinion that defeats all the various things that $UTHR threw against the wall and their subterfuge legal tactics. That opinion would take months to write and there would be no urgency to delivering it given he was not going to affect the commercial reality on the ground.

We're now almost a year away from the bench trial and there is no decision.

Would this judge turn around and deliver the 20 page opinion that he could have delivered in September or is it more likely that he is writing a much longer and denser opinion?

English

It not that Foundayo is bad and Oral sema is good

Its that the expectations gap between the two is way too fucking wide

English

@unemon1 Did you check the same file data on previous filings they've done?

English

@AnnaFlorcia Why is $LQDA so special in long term? Have you seen what’s in pipeline both with UT and others?

English

@from1to3000000 Why does no one care and why does he sell if he knew Teton would hit

English

Insane. Martin $UTHR sold $6mm more, exercised/ liquidated 9500 shares, is exercise/ liquidating (via 10b5-1) entirety 1.7mm more shares before Dec'26. While he pumps like Atlas and dumps onto market doesn't care. Those pumping pumpers could pump like pumping pumpers pump! $LQDA

English

@A_May_MD @idalopirdine Hey Adam, you referring to Marc and Co ? Thanks in advance

English

@idalopirdine Idk who we are talking about but obviously they took it down because they’re being bought out.

English

@A_May_MD Do you think the market thought OX40 is garbage already pricing the in or this should be a strong catalyst for NKTR ?

GIF

English

🚨🚨🚨 The 2nd case of amlitelimab (OX40) induced Kaposi sarcoma was just disclosed by $SNY today at AAD.

Somehow $NKTR is still in the double digits…*surely* the complete death of Amlitelimab would change this?

Up until very recently (weeks) $SNY has *still* been projecting amlitelimab to be a $3-$5B peak sales drug in atopic derm ALONE.

If Amli is discontinued (as it should be) $NKTR’s rezpeg would be slated to be the next new MoA on the market for AtD, and THE ONLY non-IL4/13 biologic besides the ineffective Nemluvio (…which is still going to be a $4B+ peak mega blockbuster despite its lack of efficacy……..)

Right now, $NKTR’s efficacy vastly exceeds nemluvio’s and beats OX40’s by a healthy ~10% delta. All of that WITHOUT causing cancer. $3-$5B peak for OX40??? What’s $NKTR worth?

OH! And that’s just the sales projections for AtD…I expect that soon the market will wake up to the fact that Rezpeg is a legitimate drug for alopecia areata too, which currently seems to be priced totally out of the stock.

IMO $NKTR already went into the weekend the most mispriced name in my book. Now the death knell for OX40 is coming into view. $NKTR is *CLEARLY* the biggest direct beneficiary of this in the entire market.

As always, I’m biased, but I’m just mind blown that this isn’t already a $100 stock. Let’s see if the market starts to accept that OX40 is finally done for. That could be explosive news for $NKTR.

English

$LQDA - Our good friend Claudius with the take.

Judge Andrews put out a post-trial patent opinion resolving JMOL, new trial, enhanced damages, and pre/post-judgment interest after a jury trial against Amazon. Three major reads for LQDA:

1. Bandwidth proof. Andrews just issued a 52-page substantive patent opinion during the CJRA sprint week. This eliminates any remaining doubt about whether he has the capacity to drop the '327 bench trial opinion this week. The '327 opinion is comparable in scope and complexity. He clearly had this one queued and ready — same will be true of '327 if it's done.

2. Forfeiture hammer — directly parallel to UTC. The most LQDA-relevant theme throughout this opinion is Andrews' repeated use of forfeiture doctrine against Amazon. Amazon failed to object to testimony and evidence at trial, then tried to raise those issues for the first time in post-trial motions. Andrews shut this down systematically, citing Motorola, Caisson, and Belmont — the same forfeiture framework that applies to UTC's conduct in the '327 case. Specifically, Amazon didn't object to expert testimony on an infringement theory during trial, then argued post-trial that the theory was "undisclosed." Andrews found the objections were forfeited. This maps almost perfectly onto UTC's ambush strategy: UTC concealed the §102(b)(2)(C) defense, didn't present documentary evidence during trial, then tried to supplement the record post-trial (D.I. 451/453). If Andrews applies the same forfeiture logic, UTC's attempt to shore up its evidentiary gaps after the fact gets the same treatment Amazon got here.

3. Footnote 1 — intolerance for advocacy gamesmanship. Andrews openly criticized Amazon's counsel for effectively doubling their page allotment through a derelict opening brief that forced a supplemental letter, stating he "regret[s]" allowing it. This is the same judge who will evaluate UTC's discovery conduct, backdated interrogatory responses, and procedural ambush. Andrews doesn't just notice these things — he puts them in footnotes and holds them against the offending party.

English

I also joined whoever was buying the $LQDA Apr 2 $47 calls this morning and I bought a few $45 calls also.

AnnaF@AnnaFlorcia

$LQDA Judge Andrews has no court hearings for the rest of the week. I'm expecting a ruling from him by Friday. This trial will get posted in the CJRA (list of shame) on the 31st of March if no ruling. He has been on this list once before and ruled 3 weeks later.

English

$LQDA - Judge A just put out an opinion on Jackson v. Highridge Medical LLC. Below is what Claude says.

The opinion itself involves Andrews doing granular documentary analysis of whether a patent agreement constituted an assignment or a license, with a focus on the actual language and evidentiary record rather than conclusory assertions. He found that Dr. Jackson's unilateral claim about a "mistake" wasn't supported by the record (no corroborating evidence from the counterparty). He demanded documentary proof, not just testimony.

That analytical disposition maps onto the UTC common ownership question: UTC's §102(b)(2)(C) defense relies on Dr. Byrd's conclusory testimony based on Orange Book listings, with no assignment documents, no employment agreements, and no testimony from IP counsel Snader. If Andrews applies the same evidentiary rigor here — demanding actual proof of the ownership chain rather than accepting inferential claims — UTC's defense looks thin.

Not a direct legal parallel (different statutes, different posture), but it reinforces the behavioral profile: Andrews wants receipts, not assertions.

English

Eesti

@investseekers Can anyone call into the $NVO AGM tomorrow?

Unrelated, can you and or @ResearchPulse1 teach me any Danish curse words?

English

The Danish C25 index rose 0.7% on Wednesday, despite $NVO falling 0.9%

Vestas led the index, up 6.0% after securing U.S. orders totaling 505 MW

Novonesis gained 2.3% as Citi upgraded the stock to Buy and raised its price target to DKK 415

Pandora was the worst performer, down 4.4% as rising silver prices weighed on the stock

#stocks #InvestingTips

English

@AnnaFlorcia $UTHR $LQDA Best conference call ever. Hell year we are pumped. You just have to listen. youtu.be/_l1q1DiIP4w?t=…

YouTube

English

I guess the drawback of becoming the $ABVX guy is that I've got to respond to ridiculous takes as they pop up now. Wedbush is making a full time job of it.

Their recent note tries to catastrophize about steroid tapering (or lack thereof) in the phase 2 dataset, claiming this undermines $ABVX's probability of success in phase 3. If you're not in the weeds on the data here, I could see how you might read that and think "oh no, that doesn't sound good".

However, if you *are* remotely in the weeds on these data (as Wedbush should be but very clearly isn't), you can read that take and laugh at the analysis - so let's bring everyone into the weeds here.

First of all, it's funny that Wedbush is apparently just now stumbling across this contrived bear thesis that they're pretending is something new, because THE DATA THEY ARE TALKING ABOUT WERE LITERALLY PUBLISHED ***BEFORE*** THE PHASE 3 INDUCTION DATA CAME OUT IN JULY. The publication was from May, and it mostly rehashed data that were actually already widely known for years from ABVX's prior conference presentations and corporate decks.

Welcome to the party, Wedbush - it's been going on for a while. Have a seat.

Ok so what's the supposed issue? Wedbush is saying that ABVX didn't force tapering of steroids in the P2 maintenance trial, which is standard practice in P3 trials. The issue is.....Not forcing steroid tapers *is standard practice* for P2 trials...which is exactly what ABVX did, in line with standards...

In my ABVX pitch from July I discussed comparing their maintenance dataset to two of the most robust comparison P2 studies - those from Zeposia and Velsipity. These are great comps because these drugs are all oral and all of the P2s had open label maintenance portions.

Oh, and also...none of the trials forced a steroid taper...because that is standard!

The Zeposia study literally didn't even MEASURE steroid free remission (ABVX and Velsipity studies at least measured what the steroid free remissions were, but none of them forced any tapering).

So, not only is Wedbush making a fuss out of a dataset that has been around since $ABVX was trading at $6/share, but what they're complaining about is just flat out standard practice...yet they're acting like it's some sort of new discovery that undermines the drug's activity altogether...after it just reported the 3rd highest UC induction remission delta of all time...Ok.

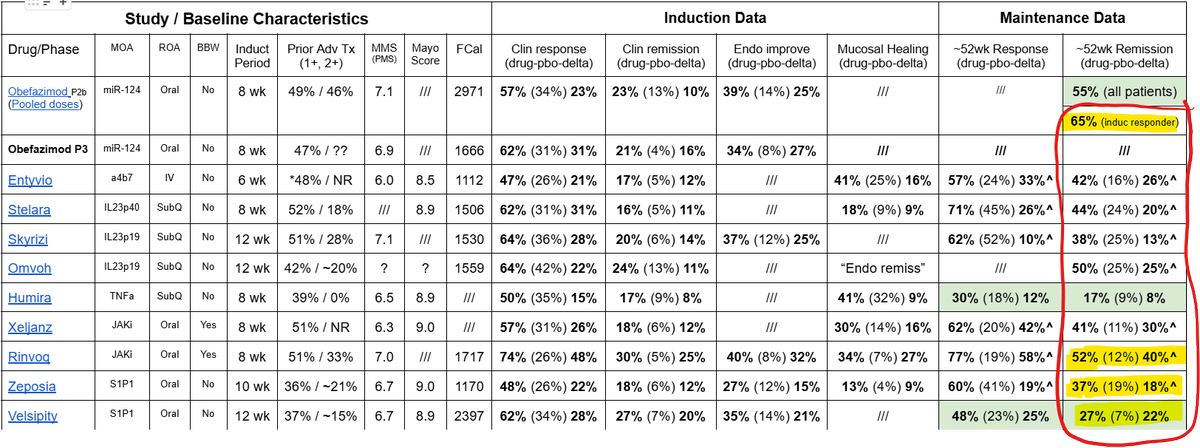

I'm going to point everyone to this table (attached) yet again. As most will likely know by now, only induction responders enroll into the maintenance portion of UC P3s, so for $ABVX, the P2 maintenance remission number we look at is that 65% number on the far upper right corner (which was the P2 maintenance remission rate among patients who had responded upon induction).

Take a second to compare that 65% number to the numbers below it from other P3 trials. 65% would be, by far, the single highest number ever recorded in a phase 3, and it wouldn't even be CLOSE. 65% would literally DOUBLE the remission rates of some of the other (approved and used) drugs on that list.

Nobody (absolutely no one) believes $ABVX is going to repeat 65% maintenance remission in P3. Yes, that is the appropriate responder-enriched number from the P2 that will be represented in the phase 3, but the P2 was open label, and yes, in P3 steroids will be forced to taper.

Look how much room they have for that number to get worse! It could drop 12% points and still be the highest remission rate of all time (which is by no means necessary for success here). The P2 maintenance remission data were so otherworldly good that we already all know the number has to come down in P3 - no way around it. All the bulls have known this all along (just like we all understand the basic drug design of UC trials which involves forced steroid tapers in P3 but not in P2...apparently unlike some).

But, of course, the placebo adjusted delta is ultimately what will matter in P3. 20-30% delta has been broadly discussed as the target range for $ABVX, and I completely agree (as I said on the YAVP podcast last week, my guess is a middle ground bet on 25%).

How hard will that 20-30% target range be to hit? Let's assume that the placebo remission rate mimics that of the R+Z+V dataset combining 3 of oral therapies on that table. The average placebo remission rate among those trials was 12.7%.

If we assume ABVX has the same placebo remission rate in maintenance (which may not be fair as ABVX's placebo remission rate in induction was *lower* than the R+Z+V average), then $ABVX would only need a 32.7%-42.7% remission rate on drug to "hit the bar". Again, this is versus the 65% achieved in the open label P2...

Wedbush tries to sensationally mislead investors into thinking that "1/3" of the remissions in the P2 were just "due to steroids", simply because 1/3 of the patients in remission had not come off of steroids. This is inherently misleading in the first place because there was no forced taper of any kind on the study, meaning patients in remission may not have even *tried* to come off of steroids. If there was a forced taper, without a doubt at least *some* of those 1/3 of patients who stayed on steroids despite not attempting a taper would have stayed in response when coming off of them. Of course not all of them, but SOME of them would have maintained remission despite a forced taper. So, that 1/3 number perhaps becomes 1/4 or 1/5 if a forced taper were implemented.

But, ok. Let's play along with Wedbush's game anyway and just stick with the phony 1/3 number and say "Ok, take away 1/3 of the remissions due to steroid taper in the P3!

1/3 from 65% is...43.5%...

So, 43.5% less our estimated placebo response rate of 12.7% and we've got...30.8% remission delta! Literally HIGHER than the high end of the bar! And hey, that would beat Xeljanz to make $ABVX the 2nd highest maintenance remission delta of all time...only behind Rinvoq!

So, I guess that all I have to say to Wedbush is...Thanks! Thanks for once again thinking you found something bearish that actually just serves to prove the point for the bulls.

Now please cut this out so I don't feel compelled to address such silly work.

Adam May@A_May_MD

Lot's of requests to discuss the Wedbush report on $ABVX today. It's a doozy. Obviously I'm a biased bull so sure, take my thoughts with a grain of salt, but this is truly, awful work from my perspective. Let's dig in on a few of the key issues.

English

$ABVX wow major bag for me here. Low volume slop. Thought it may get pumped some before the dump on Tuesday

pork@Taintslapp12283

$ABVX too risky to miss BO. Back in with size.

English

Bon courage à #accor $ac pour se sortir de ce scandale

Traffic d enfants

Ahurissant

Grizzly Research@ResearchGrizzly

We are short Paris-listed hotel chain Accor SA $AC.PA $AC “Accor, Epstein, and Ukrainian Orphans: Our Investigation Into Child Trafficking” Our new report is available on our website: grizzlyreports.com/accor/

Français

#abivax $abvx

Bientôt on pourra tous dire un grand merci à @lalettre_fr

Français