Sabitlenmiş Tweet

WeaponX₿T

24.5K posts

WeaponX₿T

@WeaponXBT

“Bitcoin is our peaceful weapon of choice against central bank driven time theft” - Ross Stevens

メタプラネット Katılım Mayıs 2009

2.4K Takip Edilen1K Takipçiler

WeaponX₿T retweetledi

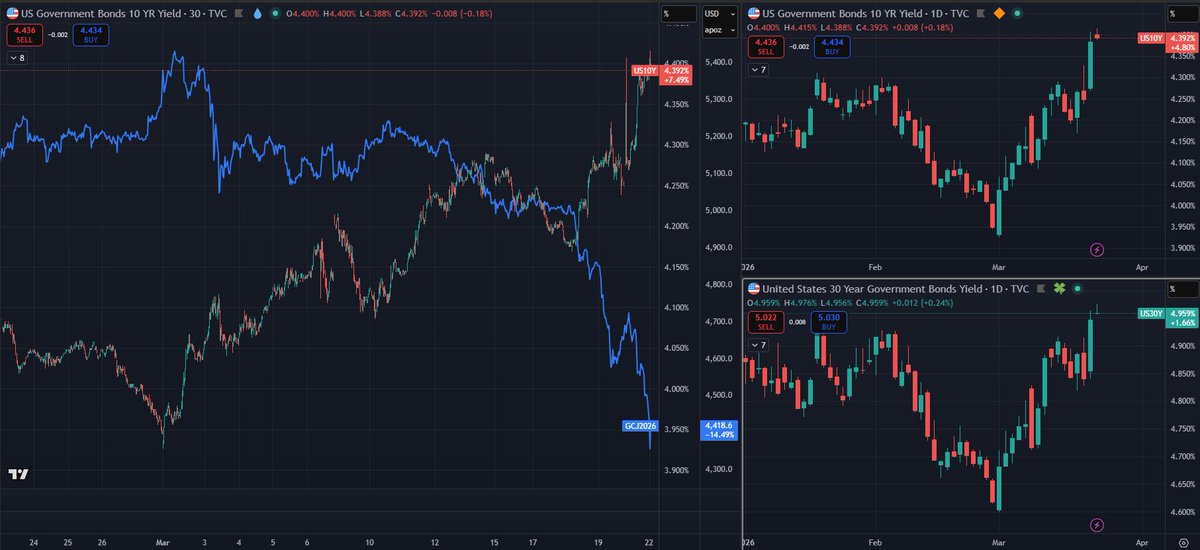

#Gold has returned to its 200-day moving average for the first time since 2023, as the Middle East conflict triggers a broad macro shock and forces a repricing across global asset markets.

In this environment, gold has emerged as one of the more exposed assets, driven by a combination of long liquidation, and now also stop-loss selling, and investors raising liquidity—partly through gold sales.

Once the dust settles and the current wave of selling runs its course, gold is likely to stage a strong rebound.

English

WeaponX₿T retweetledi

#Gold is falling because yields are rising.

Non-yield-bearing assets generally don't do well when yields rise.

Imho, this gives us a setup to load up on gold at bargain prices in the near future.

English

WeaponX₿T retweetledi

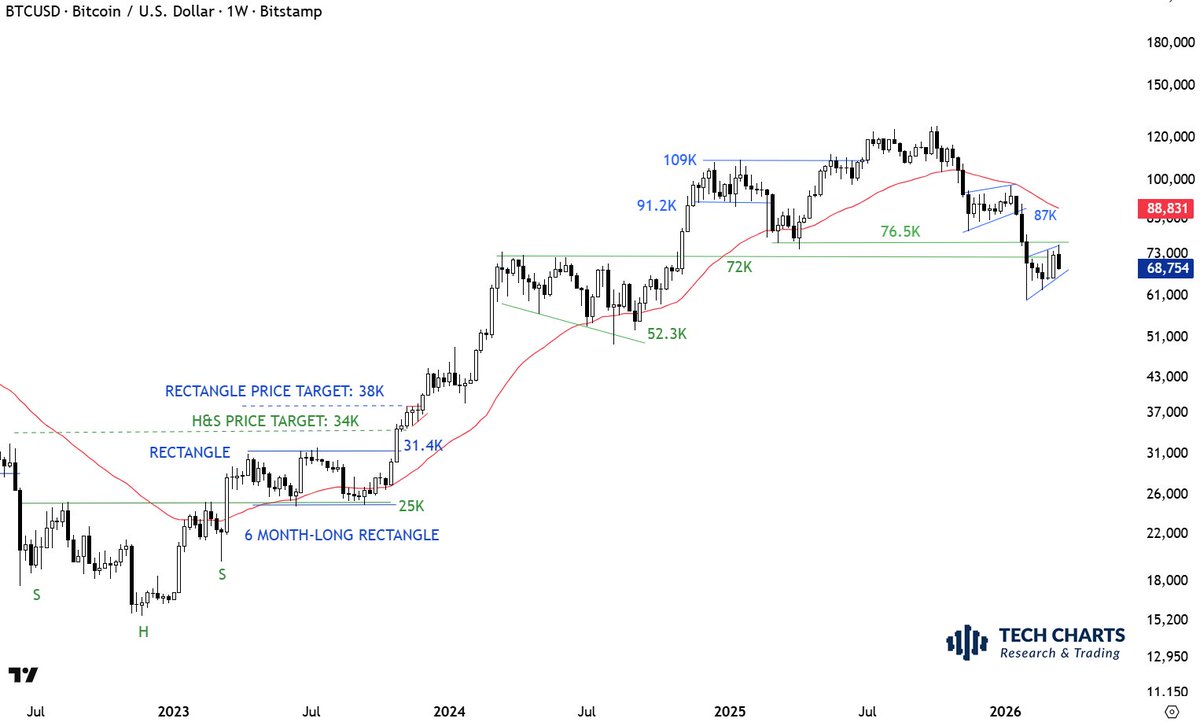

No better time to highlight the importance of long-term averages as a trend filter.

After breaking down the year-long average around 100K, the first rising bearish wedge found resistance at the average.

The second possible bearish wedge is having difficulty to breach the resistance area between 72K-76.5K.

Conclusion: once you establish a trend below long-term average, chances are high you are sitting on a weak price action that is exposed to more surprises on the downside. $BTCUSD

Aksel Kibar, CMT@TechCharts

From the days when I worked in the MENA, managing funds. My CIO and CEO @LongArcNews one day stops by to reassess the market conditions after significant weakness. He tells me Aksel, you wake up in the middle of the night, go to the kitchen and see a cockroach... You don't question, where did it come from, how did it come... You kill it first, then question. There is likely to be more of those. This is called cockroach theory in a nutshell. So, if more and more stocks are breaching their 200-day averages... it is time to pay attention and take action.

English

WeaponX₿T retweetledi

This is a quarterly long-term chart of #GOLD. If it closes March (1st quarter) with a long upper wick like this, it will not look good on this parabolic advance. Take note. Let's revisit end of March.

English

@BLachl88128 @MacroBombastic @BobLoukas 2028 cycle top unless we manifest another parabola with haste

Gary Savage@garysavage1

Ever since gold completed its last 8 year cycle low it's been a bad idea to sell when the weekly charts have dipped to oversold levels. This will continue to be the case until the 8 year cycle tops. But it's still too early for that. If we can rebuild the wall of worry then the 8 year cycle isn't likely to top before 2028. If this slingshots back up once the bottom is struck and we start a second parabolic phase then the top would come later this year or more likely in the spring of next year. Either way it's too early for the 8 year cycle to top, plus in the case of silver there's just no precedent for a breakout from a 45 year base only rallying for 2 months and a pitiful 140% increase. A base that big should produce a 500-1000% increase before a major secular top.

English

@MacroBombastic @BobLoukas If this is a base building year do you think the real expansion starts right after or takes longer than expected

English

Nothing unusual about gold selloff. Profit taking a 3yr move and raising cash as we go risk off. Think it spends most of the year building the next base.

English

@Tradermayne Cool to see you looking at cycles and not just price action 🤝

English

WeaponX₿T retweetledi

Consumer Staples are hitting new 6-week lows today relative to the S&P500. That's not something I'd expect to see if the stock market was about to collapse.

English

WeaponX₿T retweetledi

We know from history that correlations have converged to 1 during times of stress. That is indeed happening within the equity markets.

English

WeaponX₿T retweetledi

WeaponX₿T retweetledi

Metaplanet published a great detailed breakdown of their recent raise and warrant issue. Let's take a deeper look.

What stands out to me is not so much the top line figures, but what deal structure and guidance revisions suggest about the current fundraising environment and adaptations to it.

Firstly, it should come as no surprise that with a bitcoin bear market in full swing, it is currently a much more challenging environment to raise capital in.

We see this directly reflected in both deal structure and MSW guidance.

1) Embracing volatility traders.

Prior messaging had been that Metaplanet wished to pursue long only investors and avoid convertible bonds, in part due to the deleterious effects on share price of convert short hedging.

Nonetheless, the equity + warrant deal is a pseudo-CB structure designed for volatility traders. The dip subsequent to deal announcement suggests short hedges being placed.

However, unlike convertible bonds, the equity + warrants structure introduces no new debt, maturity risk, or senior claims to Metaplanet's bitcoin. This keeps the balance sheet pristine for preferred share issuance.

In effect, this raise represents something of a compromise in order to increase the bitcoin collateral base in advance of preferred share listings.

And, for a reality check on current market conditions, bitcoin treasuries looking to raise capital now are likely limited to volatility traders as potential institutional investors.

2) Deal pricing is lower than might be expected.

Equity + warrants provide far less downside protection than a convertible bond with guaranteed return of principal. So naturally, the pricing would be expected to be lower than a convertible bond.

The weighted average across pricing is roughly equivalent to issuing a convertible bond at a 9% premium.

As some noted, the warrants were priced at a significant discount to Black-Scholes pricing. However, institutional deals are never priced at full IV. Strategy's convertible bonds, for instance, were typically priced at 50%+ discounts to implied volatility.

Even so, and bear market conditions notwithstanding, I can't help but feel warrant pricing could have been higher. Management's own statements indicate the deal was priced favorably as part of relationship maintenance with investors who are under water on prior institutional raises. Which makes sense to a point, but under water retail investors unable to avail themselves of the same deal understandably have some misgivings.

3) Revised mNAV guidance.

The target range of 3x-7x mNAV for MSW exercise has been phased out in favor of a >1x mNAV mandate. Which is formally codified into the MSWs with a requirement to only be exercised when share price exceeds 1.01x mNAV.

This represents a significant downward revision, but also requires a reality check for current market conditions. At time of writing, Metaplanet stock trades at ~1x mNAV and is unlikely to trade at higher multiples until bitcoin re-enters a bull market.

If you want Metaplanet to raise at 3x-7x mNAV here, it's simply not happening. It's not a management issue, it's a time point in the bitcoin cycle issue.

As it stands, I think it is to Metaplanet's benefit to continue increasing the size of its balance sheet even if at 1x mNAV (i.e., net accretion is zero) for two reasons:

1) The total amount of capital needed to be raised to increase bitcoin holdings is significantly lower at current bitcoin prices.

2) A larger bitcoin collateral base paves the way for increased preferred share issuance. When preferred shares become the main strategy, common stock issuance has to be viewed as one leg of the pref trade. This is exactly the same thing I have been saying about Strategy.

Of course, the larger question is, "When are preferred share listings coming?"

Metaplanet has already issued shares of Mercury via private allotment, but it is really the public listing of MARS (Metaplanet's equivalent of $STRC) that is key. Public listing allows for proper price discovery and broader participation through increased liquidity and public access.

A listing any time in 2026 would likely enable Metaplanet to fund bitcoin at very attractive prices.

In sum, I am not going to say that Metaplanet's raise was a slam dunk, because it is not. But I do see the rationale for Metaplanet continuing to expand its bitcoin collateral base in the context of broader strategy, and shareholders need to have a much more sober view of what fundraising terms are possible under bitcoin bear market conditions. It's a buyer's market.

That said, it's worth noting that Metaplanet is one of only a handful of BTCTCs that has been able to raise any capital at all in the past 6 months. This will change when bitcoin re-enters a bull market. But this is where are right now.

English version of Metaplanet's presentation here: t.co/YTNrxsM06s

Metaplanet Inc.@Metaplanet

第三者割当増資等に関する補足説明資料 contents.xj-storage.jp/xcontents/3350…

English

I’m skeptical of the inflows remaining high. 2 weeks ago the big buyers of STRC were Strive and OranjeBTC. We don’t really know who bought last week and whether it represents true adoption or just more moves by other BTCTC’s managing their treasuries or even something else. I hope Strategy can keep it going

English

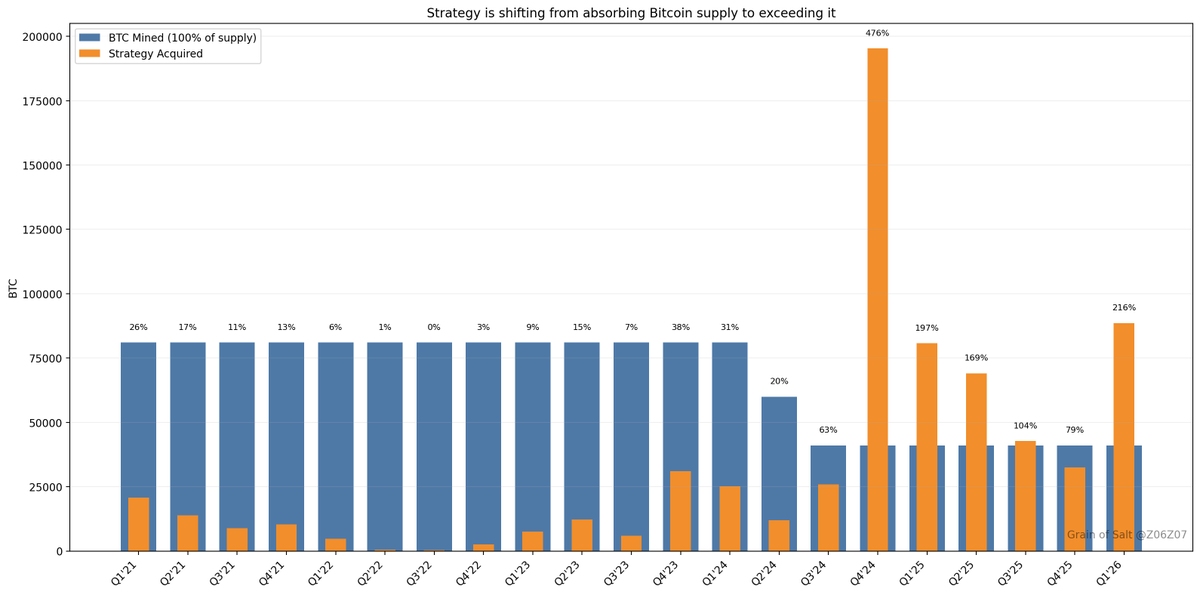

Study this chart carefully courtesy of @Z06Z07. What you will notice is that in this current bear market (Bitcoin down approx 50% from it's high in October 2025) @Strategy has been accumulating Bitcoin as a "significantly" faster pace. (Q1 2026 is the second best quarter ever. Approx 85,500 BTC so far).

Why? $STRC is now making this possible. The demand for STRC is remarkable allowing the company to use proceeds to buy Bitcoin.

You'll have to ask yourself how much more Bitcoin will Strategy be able to accumulate in a bull market. This is where Grain's hockey stick implication comes into play. Within a few quarters Strategy may very well have accumulated a total of over 1M BTC. This will make major news with the countdown to 1M creating a lot of buzz.

At some point we should approach escape velocity where the scramble (demand) for Bitcoin will outstrip supply and new issuance. Time will tell but the signs point to massive repricing upward in the not too distant future.

English

WeaponX₿T retweetledi

See my analysis at the time of the previous bearish wedge pattern. A similar pattern might be developing.

Not a prediction.

Breakdown of the lower boundary will be the signal for a possible move towards 52.5K. $BTCUSD

Aksel Kibar, CMT@TechCharts

The consolidation below the long-term average. With cryptocurrencies I'm taking the 365 day EMA. With equities I take 200 day EMA as my year-long average trend filter. So far $BTCUSD respected the year-long average. This is part of the chop and search for a base. The pattern can become a rising wedge, usually bearish in an attempt to test 73.7K-76.5K support area.

English

@Mr_Derivatives Maybe I can be redeemed here x.com/BigCheds/statu…

Cheds Trading@BigCheds

Wow look at this terrible call by me

English

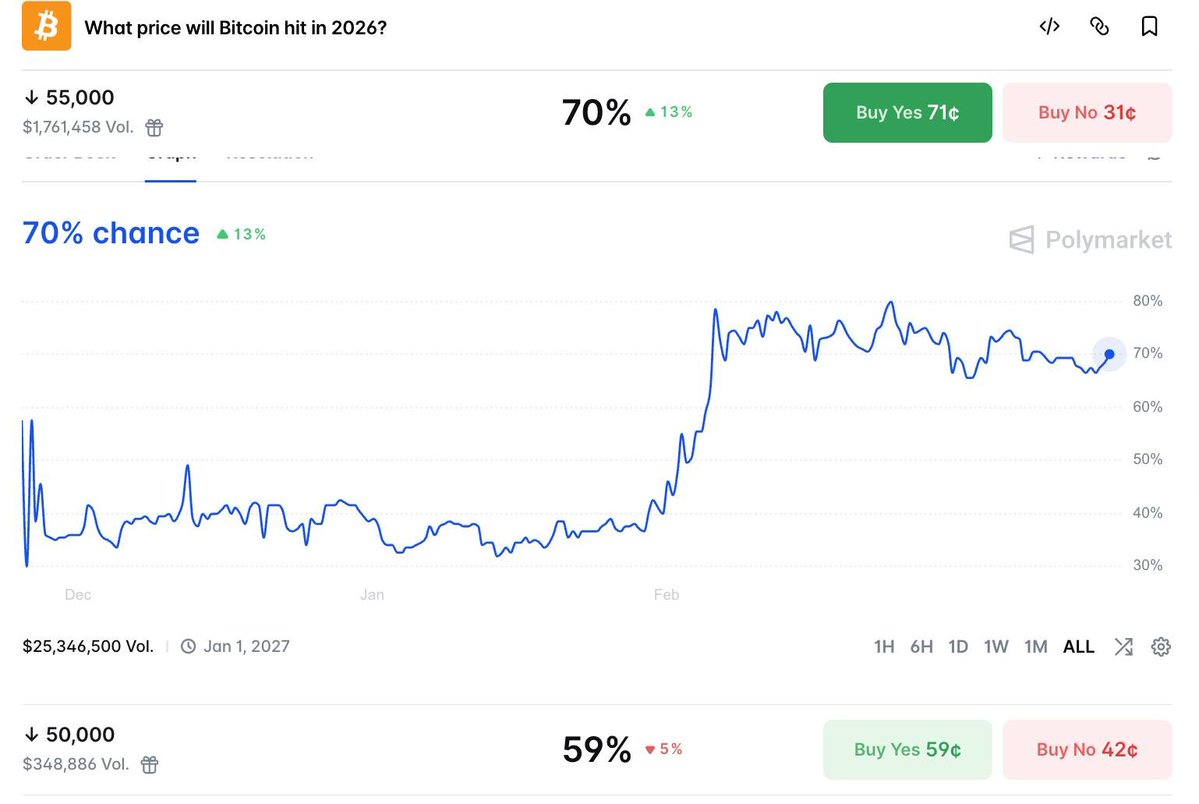

Current $BTC odds of hitting $40,000-$55,000 still very high based on the predictions market…

Gulp.

English

Price just did a failed breakout, its not that "people" have turned bearish, the price did

English

Chat what do we think

il Capo@CryptoCapo_

Now that most turned bearish again, it's time to send it much higher.

English

WeaponX₿T retweetledi

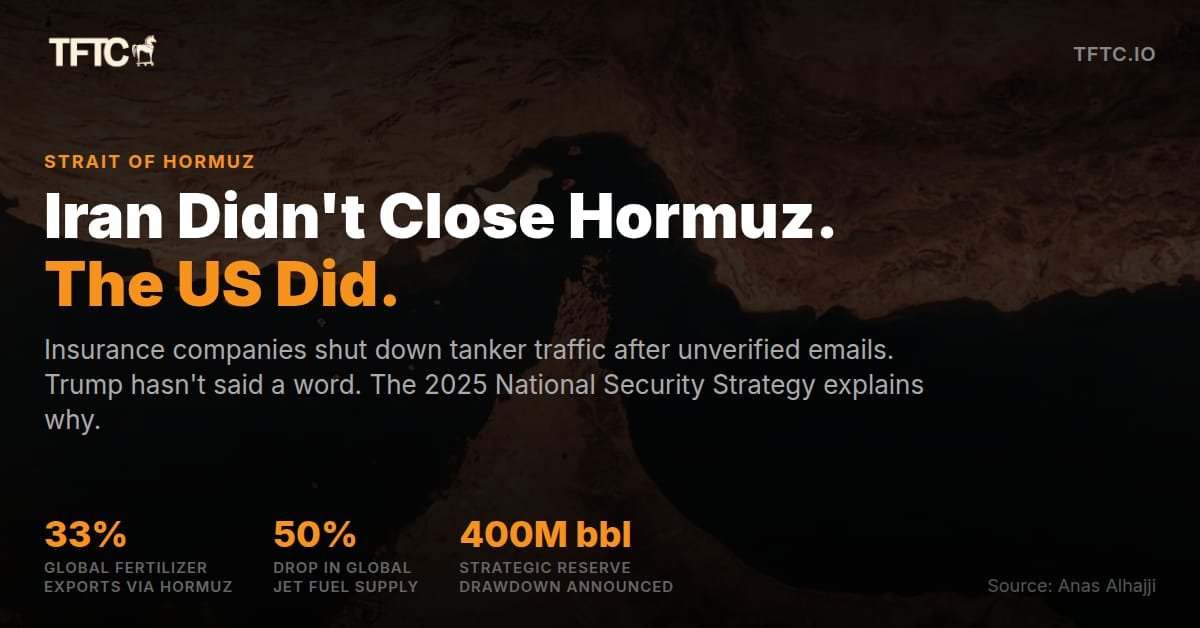

The US didn't just attack Iran. It closed the Strait of Hormuz itself, and nobody's talking about the real reason why.

@anasalhajji, one of the most respected energy analysts in the world, just published an extraordinary breakdown of what's actually happening in the Strait of Hormuz. The short version: Iran didn't close it. Insurance companies did. And the US has every incentive to let it happen.

Here's what actually occurred. Emails were sent to oil and LNG tankers claiming to be from the IRGC, saying the strait was closed. No official Iranian statement backed this. Nobody knows who actually sent the emails. But within hours, European insurance companies canceled policies or jacked premiums so high that tanker operators couldn't move.

Cargo ships and container vessels passed through fine. Nothing happened to them. Only oil and LNG tankers were affected. Why?

Notably, the administration has not criticized the insurance companies or pushed back on rising oil prices, a departure from its usual stance of vocally opposing anything that raises energy costs for American consumers.

Meanwhile, Venezuelan oil was pre-positioned in US ports before the crisis began, specifically to replace Iraqi crude that would be cut off by a Hormuz closure. That doesn't happen by accident.

The 2025 National Security Strategy document lays out the framework:

US dominance runs through AI, and AI runs through cheap, abundant energy. The strategy is to make energy cheap domestically and expensive for competitors. To do that, you need control of global chokepoints: Panama Canal, the Red Sea, Greenland's Arctic passage, and now Hormuz.

The Hormuz disruption accomplishes several goals at once. It forces Asian companies to abandon long-term LNG contracts with Qatar and the UAE in favor of American suppliers. It cripples competitor access to fertilizer exports (33% of global supply transits Hormuz). It drives chip manufacturers to reshore to the US. And Trump's offer to provide Navy escorts and US-backed insurance for tankers gives America indirect control over the strait indefinitely.

The biggest beneficiaries of a closed Hormuz are the US and Russia. The biggest losers are Europe, Asia, and the Gulf states themselves.

Iran is the excuse. Energy dominance is the goal.

English

English

@TechCharts Take this chart and add

200W MA

LTH realized price

where those 3 lines converge

that's the most trustworthy level to act on

English

If you got in with a chart signal, you should get out with the chart signal. $BTCUSD

Aksel Kibar, CMT@TechCharts

Pattern negation level reached. Sidelines... Equities have PPT (Plunge Protection Team) that steps in and frequently saves the market. If $BTCUSD doesn't have its own PPT, the weekly candle can get longer.

English