Yield retweetledi

Yield

113 posts

Yield

@Yield_of_Parth

Views are mine and not financial advice. Retail Investor. Always DYOR.

Katılım Temmuz 2015

1.8K Takip Edilen2.1K Takipçiler

Yield retweetledi

Another round of on-site recruitment. Seems like they really want/need to get this staffed up urgently

LatentValue@latent_value7

Recently on 104 (jobsite), HIMX posted a job ad aggressively recruiting operator/packaging workers to Fab 2 via both scheduled and walk-in interviews. No experience required, day/night/overtime shift structure, aggressive retention bonus. Suggests CPO efforts moving forward now?👇

English

Yield retweetledi

Sweetwater 1 has been successfully energized – a key milestone in the development of the broader 2GW Sweetwater campus.

@danroberts0101, Co-Founder and Co-CEO of $IREN commented:

“Delivering Sweetwater 1 substation energization on schedule reflects our disciplined execution, the strength of our supply chain relationships and the efficiency of our vertically integrated development model. It is another example of our ability to design and construct large-scale infrastructure reliably and at speed to meet market demand.”

Learn more: iren.gcs-web.com/static-files/d…

English

Yield retweetledi

$IREN energized its 1.4 GW Sweetwater 1 data center site in Texas, connecting the substation to the ERCOT grid and marking a key step in building out its 2 GW Sweetwater campus. The company said power will ramp as data centers are commissioned.

English

@philliplyle410 I reject the premise that there's no market for D2D in suburban gray zones where millions of people pay for spotty coverage. Classic loser mentality. Jensen put it well:

English

@Yield_of_Parth It's going to be a while before D2D supplements any areas where existing service is simultaneously present. Wifi calling for indoors, and if you have any bars at all outside then that's what will be prioritized.

x.com/Tim_X94/status…

Alexander@AlexfromBabylon

$ASTS Verizon CRO sees direct-to-device satellite as a niche add-on, not a switch driver. Sees low demand & no major churn threat from T-Mobile's Starlink beta, despite competitor's customer targeting. Consider's T-mobile pricing a bit rich. ($15/$20) Interestingly highlights from Verizon CRO: > On narrowband D2D with Skylo: "When we surveyed our customers, we see that there is a demand for it, but it's very niche. > On T-mobile's switching offer: Based on customer service D2D is a complementary service, it's an add on, but not a reason to switch providers. Also saw insignificant volumes of customers inquire about satellite via customer service or in stores. > Pricing from T-mobile is considered rich, given low demand of the service ($20 AT&T / Verizon clients, $15 T-mobile clients) > On using $GSAT via Apple: It is emergency alerts, so very rare. It's more a peace of mind feature. > On broadband D2D With $ASTS: Expect a bit more demand, but again niche, significantly smaller then our international roaming. TDLR: Less bullish on the service then AT&T, but important to keep in mind: > Verizon currently has not finalized the DA yet with AST Spacemobile > Verizon has better network coverage then AT&T, but every network has small pockets of connectivity loss, which are fustrating for users. Management is not going to downplay quality of their service publicly. > There is the threat of T-mobile Starlink switching campaign, currently Verizon only has Skylo so there is no point in touting the service, so downplaying is logical. That said I think it's fair to say that expect on this interview Verizon expects like a 5-10% adoption rate. If I use Nomadbets model, that's still a $700 million net revenue contribution for AST.

English

$ASTS Only Tim would extrapolate demand from a broken product. That's like judging the demand for satellite consulting from his

Tim Farrar@TMFAssociates

AST's delays will allow the #cluelesscult to continue living in denial for at least another year. But this is reminiscent of George Gilder in 2000 claiming that Iridium's failure was positive for Globalstar because it removed the competition and CDMA was inherently superior

English

Yield retweetledi

Your mistake is assuming the parabolic inflection of Claude Code and then Codex over the last four months was a one-off instead of understanding that each form of knowledge work will have a similar capability tipping point and subsequent race to adopt.

English

Yield retweetledi

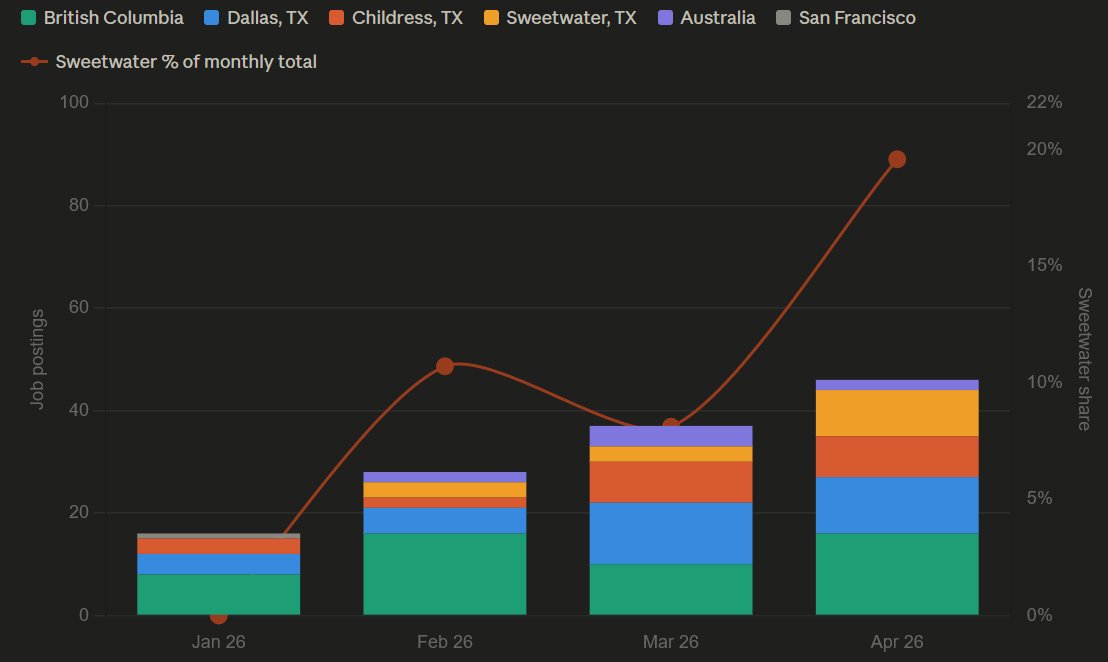

The two most verifiable signals for $IREN are (i) job postings, & (ii) construction progress. Both are real $ going out the door w/ lead time - only way to justify is w/ deals. Been disappointed to-date this year w/ % of hires going to Sweetwater - glad to see that ramping up.

English

@philliplyle410 Thr irony is I'm a Verizon customer who lives in a suburb outside a major city where cell service barely works. It’s this exact experience that made me look into $ASTS. Extrapolate that.

English

@Yield_of_Parth Demand matches what Verizon has stated it expects as well. You can keep fantasizing.

English

Yield retweetledi

$ASTS $AMZN: 🚨AMAZON VALIDATES "LARGE DEMAND" FOR D2D

"The last thing I'll say about it is, you know, your question about Globalstar. Increasingly what we're finding with our customers and enterprises and governments is that they don't like to have any periods where they don't have connectivity. It upsets whatever customer experience they are going through, even in metropolitan areas. We all hit certain parts of the highway or certain roads where you can't get connectivity or you're hiking or you're skiing. We see very large demand for consumers to have direct-to-device. That was really the impetus for our acquisition of Globalstar. They have unusual and scarce global spectrum that's required to provide direct-to-device."

- Andy Jassy @ajassy, President & CEO of @amazon

English

Yield retweetledi

Where power becomes intelligence.

NVIDIA GB300s arriving at Childress for our Microsoft Horizon deployment. Big effort from the team. $IREN

Childress, TX 🇺🇸 English

Yield retweetledi

Those selling the stock after reading the WSJ article on OpenAI fall into two categories:

1.Those who had been looking for an excuse to sell and are using this as the opportunity; and

2.Those who are simply dumb enough to follow the mood.

Why do you think Sam Altman declared “code red” last year? Obviously, it was because they were falling short of their targets.

If turning something everyone already knew into a sensational story counts as a skill, then I guess that is a skill.

English

Yield retweetledi

The demand for intelligence is unlimited. OAI is objectively on track to blowout what sellside was modeling for 2026 revenue…by a lot. Panicans are retarded.

English

Yield retweetledi

Yield retweetledi

$WULF is approaching important resistance at 22.26 at the Ichimoku cloud top.

English

Lots of interesting circumstantial evidence building around $HIMX and their role in the CPO supply chain. Fab 2 repurposing, patent overlaps/sleuthing, aggressive hiring - the mosaic is forming.

Underappreciated angle: the fab is already built and paid for. If/when the CPO revenue hits, incremental margins should be meaningfully higher than a greenfield build.

3% position for me, ~$9 cost basis.

LatentValue@latent_value7

$HIMX In 2017 the company built Fab 2 specifically for WLO capacity. This was for a 3D sensing partnership with Qualcomm for FaceID for Android phones, but that failed to get traction leaving Fab 2 largely idle with unused capacity. 👇

English

Yield retweetledi

Yield retweetledi

$IREN

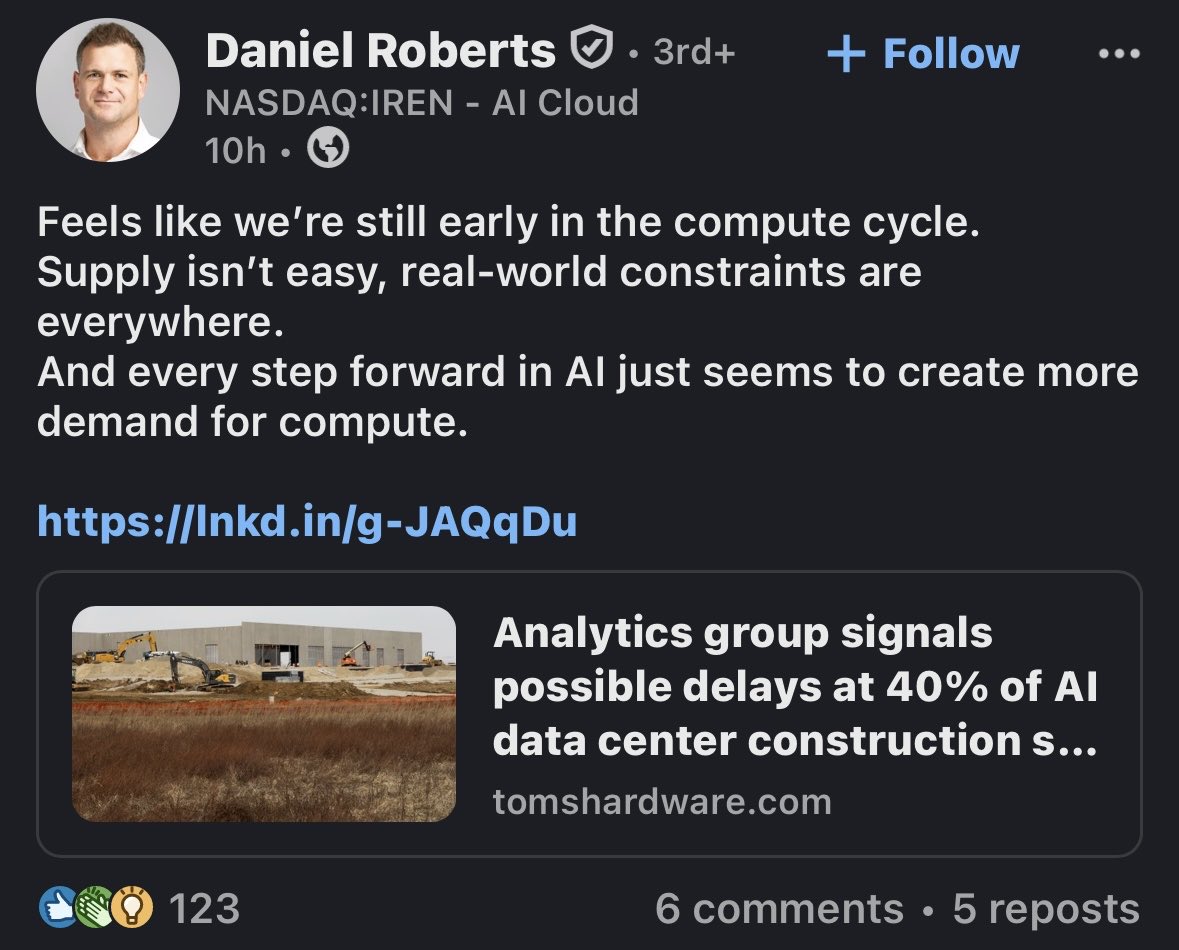

Dan posted the same thing on LinkedIn but he attached this article with

(Link in thread)

Daniel Roberts@danroberts0101

Feels like we’re still early in the compute cycle. Supply isn’t easy, real-world constraints are everywhere. And every step forward in AI just seems to create more demand for compute.

English

Yield retweetledi

$IREN & $NBIS investors now vs both in a couple of years when they finally realise they both served an extreme bottleneck.

Hyperscalers are buying all the power available. So as long as you have a company in your portfolio who can provide this, you’ll be fine.

English

Demand for intelligence is infinite. Long compute (in its various forms) will be the trade of the decade imo.

tae kim@firstadopter

@AIadventure3 My sense is that is more a 2027-2028-2029 thing at the earliest. Google internally is out of compute for their OWN ENGINEERS.

English