Lo¥15 retweetledi

Lo¥15

1.9K posts

Lo¥15 retweetledi

@_Encorelouis @InvestFreedom05 $FSLY , $CRNT for network , Energy $IPWR $ATOM , coating $SOTK

English

Which sector of the stock market will go on a massive bull run next like memory and semiconductors did?

English

$BZAI offering getting gobbled up, about 27% of the float but only about 15% of the outstanding shares. Contracts/Earnings improvement next catalyst. GL

English

@EmotionMarkets @DudeWhoInvests I m interested in $SMCI BUT all the story about this company, still worth it to buy?

English

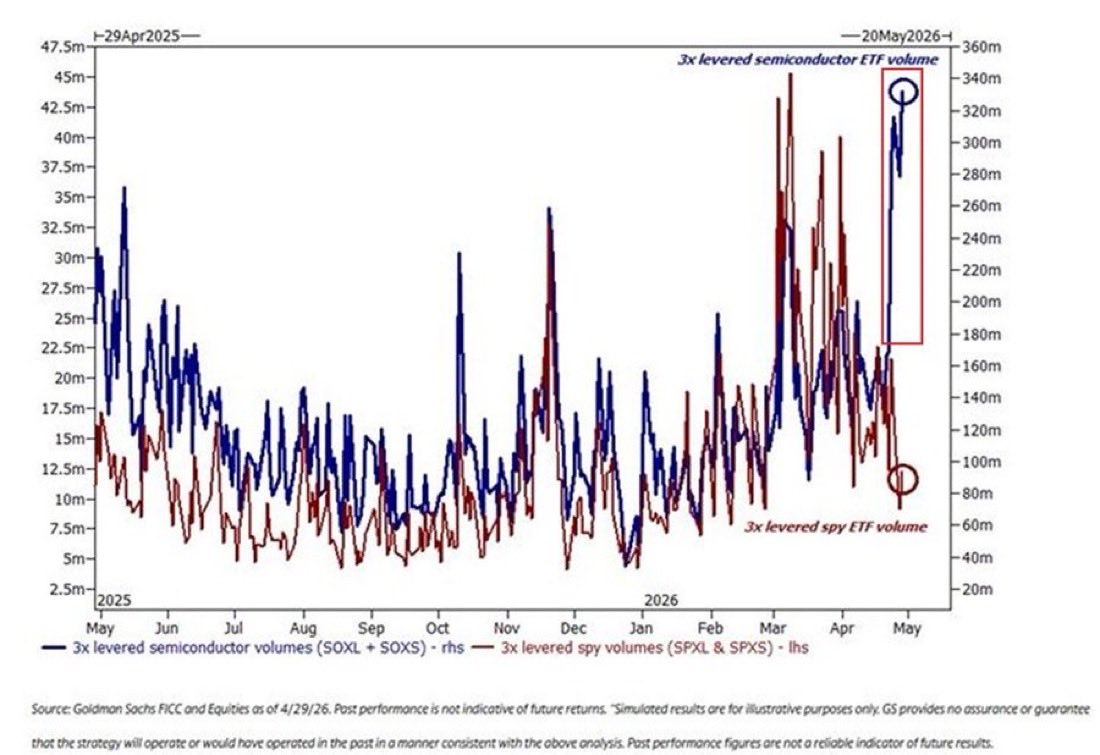

If I had to pick one area from the SETA tape, it is the semiconductor proxy rotation.

$SMCI just reclaimed the #1 Narrative Leader spot at 0.443 Coherence while crowded AI anchors remain harder to trust underneath the surface.

That is the signal.

The market is not abandoning AI infrastructure.

It is looking for cleaner ways to express it.

$SMCI is one of the names showing that migration.

English

What stock are you buying the most of right now?

English

Lo¥15 retweetledi

New study finds that Gen Z prefers buying levered semiconductor ETFs over having sex

(Per @Yale)

English

@randadtrade @adfigg So you thinks $BZAI can get a good momentum soon?

English

@adfigg Have been working $KOLD from 20, about to bank it again, I need a big pop in natgas to short it again. $BZAI new spec trade may pop in couple weeks (earnings)

English

@randadtrade ~ what’s on your radar today?

I’m stalking $SGMT, $AKAN, $MARA & $NEO at the moment.

English

Lo¥15 retweetledi

Don’t worry, you haven’t missed it. Lots of <$5B MC semis companies that you can buy before they’re all $100B

English

Lo¥15 retweetledi

letting a 22-year-old Deloitte analyst with ChatGPT tell a Fortune 500 company how to cut costs

English

@StocksDaily Lfggggg I been waiting for more news on this bad boy. I want a crazier run though lol.

English

$BZAI Blaize Holdings just dropped a major contract today.

Up to $50M deal with NeoTensr to deploy co-branded AI edge data center infrastructure across Asia Pacific. Builds on a $20M+ order from Q4 2025 — total contracted value with NeoTensr now up to $70M.

Each server handles 200+ simultaneous camera streams. Runs computer vision, LLM inference, and VLM analytics on a single hybrid edge architecture. Smart cities, industrial automation, logistics, security.

Rosenblatt maintaining Buy with $6 target. Also announced a Winmate partnership today for rugged edge AI in defense and critical infrastructure.

52-week range: $1.00 to $6.76. Currently around $1.69. Earnings May 20.

Revenue last quarter: $23.78M, beat by $1.8M. EPS beat by 81%.

Not financial advice.

English

They’re still there.

It’s just hard to say anything….

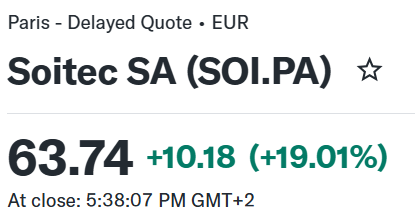

When all my recent thesis posts from $HPS.A, $IQE, $AXTI, $SIVE, $AAOI, $LITE, $NBIS, Win, Shunsin, $AEHR, $TSEM, $SOI, and many many others I call out.

Just hard outperforms the market.

Year to date of +1,116.29% isn’t too bad, right chat?

strictrope@strictrope

@aleabitoreddit Your haters seemed to have disappeared!

English

$SOI is my biggest positions, up a magnificent 20% today, and the market continues to underestimate its business as legacy verticals hide SiPho potential.

Every SiPho will need a SOI wafer, and $SOI owns the technology to manufacture them in scale.

The stock is up ~30% since I shared my detailed write up on its technology and why the market will eventually wake up to this opportunity 👇

wealthyreadings.com/p/the-photonic…

The Few Bets That Matter@WealthyReadings

Spent the last few days writing the most comprehensive photonics review possible. The need, the technology, the supply chain, bottlenecks & opportunities, from SiPho to III-V passing by CPOs. SiPho. Wafers - $SOI EDA Simulation - $SNPS Ansys SiPho design - $AVGO $MRVL Foundry etching - $GFS $TSEM $TSM III-V. InP substrate - $AXT Sumitono Epitaxy - $IQE $COHR $LITE $AAOI Visual Photonics Laser Chip Fabrication - $COHR $LITE $AAOI $SIVE CPO. Packaging $FN Testing and validation $AEHR $TER $FOR If there is a name you haven't heard off or a concept you do not understand, this is the write up to read. This is the next large vertical for AI datacenter and a sector which could run for quarters/years as the technology scales. Droping in 12h for subscribers, link's in bio.

English

@poppythetoppy @Gubloinvestor 2k share I hope sell at 5-6$ I believe in this company, good result , strong momentum.

English

Lo¥15 retweetledi