Sabitlenmiş Tweet

radicand

231 posts

@edgeville easily park hyatt niseko; right at the base of hanazono super nice and new property, make sure you eat the croissants

English

@pleyuh settlement/tokenization is the “industrial” use case (that, like gold, only supports a small fraction of the market value)

BTC cannot magically find an industrial use case without such a use case being inherently built into the asset

x.com/pleyuh/status/…

limzero@pleyuh

Without commenting on the argument I will add this: I'm surprised people still have ETH in their portfolios. I cannot see why anyone who manages money would need a position in ETH. what is the thesis for holding ETH in 2026 at 3k. Both timing and price are off

English

Call your favourite whale— we need to break this POC with force.

English

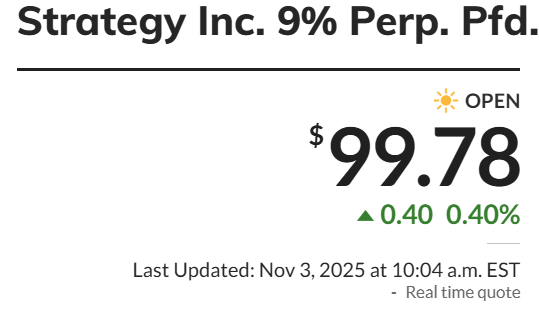

@ZeMirch (now over 99 and sustaining with daily volumes growing)

x.com/_radicand_/sta…

radicand@_radicand_

STRC hit >$99 last week, meaning the ATM facility is in play if tomorrow's numbers are materially larger than the peashooter $20mm buys the past few weeks and the STRC ATM shows significant usage the saylor bazooka may soon be returning

English

Strategy is offering $STRE (“Stream”), our first ever Euro-Denominated Perpetual Preferred Stock, to European and global institutional investors. $MSTR

English

$STRC is so close to $100.

This could be the week Strategy finally starts utilizing the $STRC ATM.

IMO, they’re probably just a 25–50 bps dividend hike away from consistently holding $100.

English

@lazyvillager1 @90 not really sure what you mean as I think you mistook supporting BTC for supporting STRC

merging the rest here

x.com/_radicand_/sta…

radicand@_radicand_

@lazyvillager1 @90 You are referring to the present situation. I am referring to future outcomes, which ultimately is what is considered when considering purchasing STRC. Ultimately it hinges on Saylor’s credibility in targeting 100. With little issuance, tapping common for buybacks is credible

English

What? So you think this is an actual lever.

Tapping the equity to support BTC, so that some invisible universe is satisfied & will then provide at least 1:1 equivalency in support around purchasing BTC???? And somehow this isn’t a value chain as you claim where STRC is directly linked to the risk of MSTR? Not to mention you can just spend the $$ directly from the common to buy BTC in the first place????

English

STRC hit >$99 last week, meaning the ATM facility is in play

if tomorrow's numbers are materially larger than the peashooter $20mm buys the past few weeks and the STRC ATM shows significant usage the saylor bazooka may soon be returning

Michael Saylor@saylor

Orange is the color of November.

English

@lazyvillager1 @90 You are referring to the present situation. I am referring to future outcomes, which ultimately is what is considered when considering purchasing STRC. Ultimately it hinges on Saylor’s credibility in targeting 100. With little issuance, tapping common for buybacks is credible

English

What. The comment I am responding to is YOUR statement around keeping the issuance manageable. That implies something active is taking place. Why would the initial tranche even be relevant in a discussion of “keeping it manageable”? Saylor sold as much as he could @ 90 to whoever would give him a dollar. This is why the pref ended up being upsized beyond the initial launch…

English

@lazyvillager1 @90 tap the common, buy STRC (mentioned in the policy statement)

hence, manageable levels

English

@_radicand_ @90 What exactly are the mechanisms to push it to 100 if it’s trading below? Buybacks? Where? Issuance only pushes it down. Yield chances are an effect, not a cause

English

@lazyvillager1 @90 I assume you are referring to ATM issuance, not total issuance including the 2.5B IPO. Again, that has been (sensibly) self-restricted until the 99 level. Mkt knows his issuance plan, yet STRC has floated up to 99 now. We are only now seeing >1 day of >99 for the ATM facility

English

@_radicand_ @90 STRC issuance is at 0. What do you mean keeping it at manageable levels? What is trading is just what is on the open market. The fact Saylor has not been able to issue is directly in line with the confidence of the product

English

@lazyvillager1 @90 I didn’t say a that. In the case of STRC, it is targeted/soft pegged to $100 through policy actions e.g buybacks, issuance, yield changes. Policy impacts pricing. As for your other pt, have already addressed that yield is not the bottleneck; new-ness is

English

Do you think "catastrophe" is a binary idea? You keep bringing up this LUNA/UST example and that makes me think you have an imperfect understanding of how credit instruments actually re-price real time

What is under pinning your belief that a credit concern doesn't "significantly show up until catastrophe"? Yield is not free. STRC is 10% right now and volume is low. That is the market's way of saying 10% is not attractive relative to the risk-reward here. If MSTR's credit/solvency risk grows, STRC may reprice downward (say 70/80) and yield would be ~15% then. Risk exists on a spectrum

English

@lazyvillager1 @90 Worth pointing out that Saylor has several policy levers to pull to maintain confidence as well, as long as STRC issuance is kept at manageable levels (remember, UST suffered multiple crises of confidence that were recovered with buybacks as well in earlier days)

English

@lazyvillager1 @90 Again, liken this to LUNA and UST/Anchor; was it risky? Yes (to say the least). Did the two attract different classes of buyers? Also yes

You are correct they are linked; my point is simply that the linkage doesn’t significantly show up until catastrophe; the everyday is diff

English

@lazyvillager1 @90 so to clarify, your view more or less is that STRC is a strictly worse neutered version of MSTR with all the same risks but with a muted 10% yield instead of the upside and therefore you don’t think there will be any significant demand for it

English

@_radicand_ @90 That is equivalent to saying a corp bond exists in a different risk universe than the underlying issuer paying out the yield. U have lost me on this. They are not just catastrophically linked. They are fully linked in every vein & every dimension

English

@lazyvillager1 @90 You are comparing the volumes of assets after their flywheels got going to an asset that is only just starting to hit its stride, though, which is not an apples-to-apples comparison. How much volume was MSTR doing in 2023 vs 2024/2025?

English

Price at 99 on thin volume is completely irrelevant. It opened up at 90 to effectively give a free 10% to initial investors. This is a thinly owned asset with no sellers (for now) to push price down. This says nothing about the novelty of demand today, nor future demand increasing

Do you realize how little volume STRC is trading on? STRC has averaged $350M per week for 14 weeks

MSTR, the equity, turns that over by more than 40x in a single DAY. BMNR does 3-5x that in a day. SBET - which is incredibly anemic - is doing $150-200M of volume per day.

English

@lazyvillager1 @90 same parent =/= same risk; in the tail, yes, STRC is catastrophically linked to MSTR and BTC. But otherwise low beta (compare current correlations btw STRC and MSTR/BTC), hence a different buyer mandate. To be clear, am not saying STRC is a t-bill, but risk is a spectrum

English

@_radicand_ @90 How exactly is STRC "worlds away" from MSTR when MSTR must pay the dividend (which is a return on capital one; in other words MSTR must continue to raise capital in the future to pay the existing dividend outstanding), and MSTR is a BTC holding company? Not even 1 degree away

English

@lazyvillager1 @90 this is where it becomes more subjective :) imo STRC is worlds away from MSTR in terms of “btc exposure”; direct exposure =/= collateral risk (and STRC does have some seniority over the collateral)

but subjective viewpoints aside, price at 99 reflects demand that exists today

English

@_radicand_ @90 I don't think STRC meets the investor mandate/goal for pretty much anyone. Any exposure to BTC must have an x return handle to it; sub-that = bad

The exception is when it is truly no impairment risk or if you have a claim on the collateral. Hence the basis trade or secured loans

English

@lazyvillager1 and STRC did raise $2.5B in its IPO (@90, so eff. yield of ~11–12%) it is just saylor’s own policy to not issue more <99. the path up from 90 to 99 now reflects existing demand, so allocators have been “in”

English

@lazyvillager1 attribute that to simply being a new product (yield comps irrelevant); new products take time to develop credibility/clarity/liquidity (and this shows in the steady march to 100 in the chart)

anchor didn’t get to $15B in deposits overnight (nor was it linear growth from day 1)

English