@Nobody_But_M3 When you use AI with Gilles de la Tourette syndrome.

English

Ace Global Value

1K posts

@aceglobalvalue

Value investor. International focus, special situations, micro/small caps. "Show me the incentive and I'll show you the outcome."

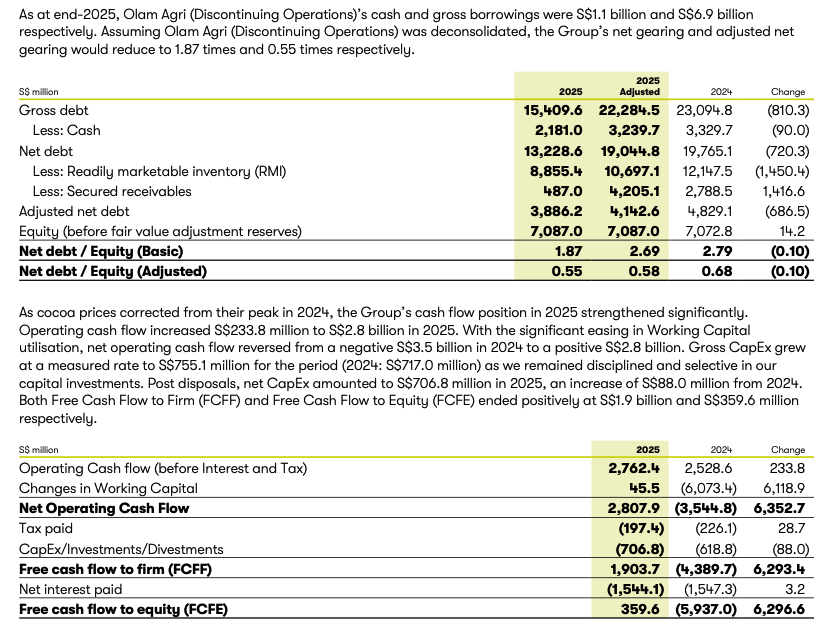

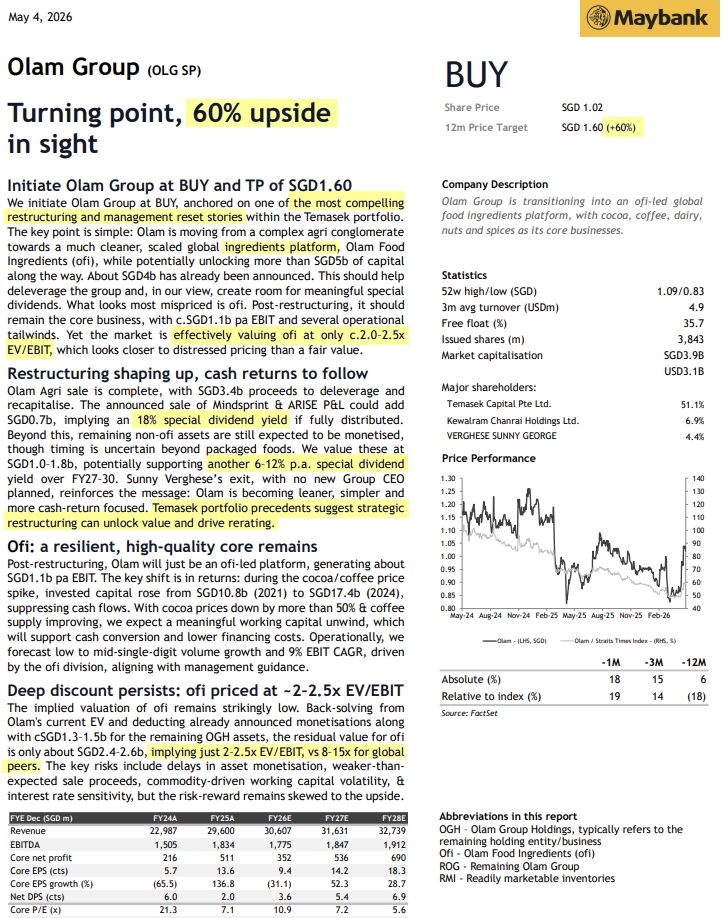

Olam Group's $VC2.SI rather aggressive divestment of everything non-core (everything except OFI) in preparation for an IPO or sale, looks quite interesting TBH. Anyone done any work on it? Global #2-3 in several food verticals. If (if!) they succeed, it's a bagger.

$SLYG In a company owned at 60% by insiders, I didn't expect to have to deal with shenanigan, but here we are. We may debate the A/R til we're blue in the face, but this is clear as day: switching revenue recognition from delivery to shipping in the dead of night. No longer long.

Que risas se pegó mi coleguita Jordan cuando le comenté en la zona de 24€ que llevaban semanas distribuyendo en newlat newprinces $NWL. Llevo meses riéndome yo , y más me voy a reír cuando llegue a su objetivo en 12€. Fintuit está lleno de "gestores" con mucho ego y poca idea