Dan

677 posts

Dan

@alchemysidda

25 years in Enterprise Software. Here for Technology, AI, Semiconductor, Investment ideas. Support American Founding values of freedom, Innovation, Abundance.

USA Katılım Ekim 2022

1.9K Takip Edilen173 Takipçiler

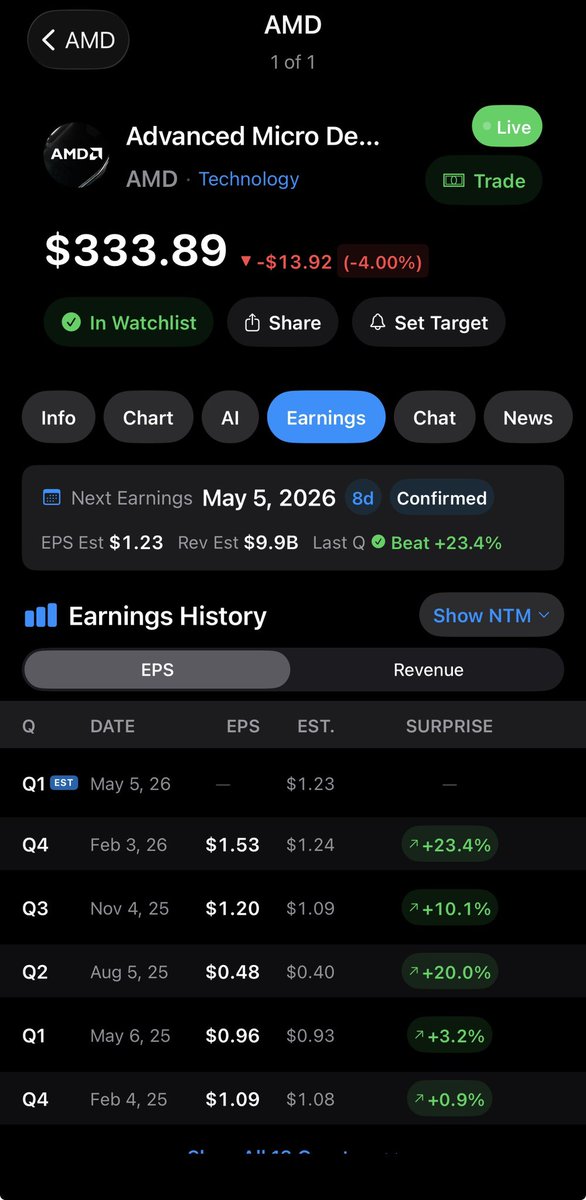

Some color from the $AMD call that wasn't in the release.

-Server CPU TAM revision. From ~18% annually (FAD November baseline) to >35% annually, reaching >$120B by 2030. This is a structural reframe.

-Q2 server CPU revenue guide: >70% YoY.

-Q1 server CPU revenue: >50% YoY. Cloud and enterprise each up >50% YoY.

-Fourth consecutive quarter of record server CPU revenue.

-2H Gaming revenue to decline >20% vs 1H on memory and component costs. Concrete negative warning.

-2H Client outlook framed cautiously on memory/component pressure, but AMD still expects YoY growth and to outperform the market.

-Data Center segment operating margin: 28% vs 25% a year ago. Segment-level number.

-Embedded design wins up double-digit % YoY, with "billions of dollars" in new wins.

-ROCm cadence acceleration via "agent-based coding workflows."

-CFO-only Q2 guide details: Non-GAAP OpEx ~$3.3B, OIE +$60M gain, tax 13%, diluted share count ~1.66B.

Picking apart the Q&A...

Patrick Moorhead@PatrickMoorhead

Yup. $AMD delivered a clean beat-and-raise. Data center is the entire story, of course. Client was up and embedded bottomed. Q1 2026: -Revenue $10.25B vs $9.84B Street, BEAT by 4.2% -Non-GAAP EPS $1.37 vs $1.28 Street, BEAT by 7.0% -Data center $5.78B vs $5.56B Street, BEAT by 3.9% -Non-GAAP GM 55%, Q2 guide steps to 56% -Q2 guide $11.2B vs ~$10.65B Street, BEAT by 5.2% 5 takeaways: -Data center up 57% YoY is sequential growth on a tough Q4 comp. EPYC and Instinct both contributing. Operating leverage is no longer aspirational. -Client up 26% YoY against the "PCs die on memory costs" thesis. Mix to higher-ASP parts plus share gain off Intel's tight client supply. -Q1 GM of 55% is the clean run-rate without the Q4 MI308 inventory reversal benefit. Q2 guide of 56% is real margin expansion off a normalized base. Mix is rotating to higher-margin server. -Embedded $873M, up 6% YoY. Off the cyclical bottom. No longer a drag. Can't wait for the call.

English

@BenBajarin @LisaSu increase of gross margin for Q2 to 56% is also good news. Deployment of First GW of MI450 would be bigger moment though.

English

$AMD @LisaSu conviction that CPU server TAM 35% YoY driven by agentic.

This is actually going to be more fun to track than GPU/ASIC volumes YoY :)

English

@PatrickMoorhead I would be looking for confirmation of AI related CPU demand increase and commentary on MI450 release date. MI300 series is a test bed for fixing software compatibility issues and overcoming CUDA moat and I won’t worry about MI300 sales.

English

$AMD reports after close. Consensus ~$9.84B / ~$1.30 EPS (+32% rev, +35% EPS). Stock up 74% in April sets a high bar. I think they will beat.

I’m watching a few things: MI355 ramp, MI400/Helios timing, Meta 6GW progress, EPYC share, and Q2 DC GPU guide. Guide and 2H exit rate matters most.

English

Pat’s Law of Always strikes again. This is more than “considering”. There’s likely real work, real tests, real assets deployed.

Jukan@jukan05

Whoa! BBG: Apple is considering using Samsung Foundry and Intel Foundry.

English

@PatrickMoorhead Ehh it was a nut, a gasket, three screws and 2 compression fittings.

English

@BenBajarin @cerebras @tenstorrent @AMD @intel I thought this was main reason nvidia aquiring Groq. What ever compute that Groq had via fabs was useful for them.

English

I maintain my thesis that all viable compute (in this context accelerators) has a chance of being adopted by hyperscalers and frontier labs. Hence why @cerebras is getting more attention and now @tenstorrent.

BUT, @AMD has more upside, and maybe we don't count out @Intel + @SambaNovaAI?

English

I've started to broadly map out the power space with some good posts by @NuttyCLD

First thing to understand is that the transition to 800V requires datacenters to be built from the ground up for true HVDC support.

The mid-term approach will be to use power sidecars to handle large power levels per rack with high voltage. Longer term, datacenters will distribute power = no sidecars.

The whole power situation can be monitored by looking at four umbrellas

1. WFE (Aixtron, Veeco)

2. Power Devices (Infinion, TI, Navitas, Power Integrations, ST, ON, Wolf)

3. Box builders (eaton, vertiv, schnieder electric)

4. Hardware providers (APH, TEC, Rosenberger)

Most interestingly, the EV supply chain now has a massive AI DC pivot, and a lot of them will be looking to pivot.

English

@kyle_e_walker Why not build desktop apps now. I used claude to convert web app to macbook app and it has much better experience.

English

"Why is your web map so slow?"

This is one of the worst things any geospatial developer can hear from a client.

You've spent tons of effort building a web application to their exact specifications based on a sophisticated analysis.

It worked great "on your machine" in local demos.

But now that you've deployed it? It's practically unusable.

I've been there. This was my motivation for developing {freestiler}, an R / Python framework for creating vector tiles.

Vector tiles solve the "slow web map" problem for large datasets, but they haven't always been the easiest to create.

freestiler can create PMTiles straight from your R / Python objects, @duckdb databases, or even shapefiles.

Host your tiles on @Cloudflare R2 and you'll have a low-cost vector tile solution ready to go. Use a Worker and make it even faster.

This is the exact stack that powers my "146 million US jobs" map.

I can confidently deploy web maps displaying millions of features now without worrying about performance lags.

Solving the "but it worked on my machine!" problem.

---

Check out the live web map: #5.1/39.8/-98.5" target="_blank" rel="nofollow noopener">walker-data.com/freestiler/lod…

And learn more about freestiler: walker-data.com/freestiler

English

Dan retweetledi

The 1st two pictures here show the visible difference between the older wrapped satin gold and the new glossy deep gold Cybercabs. Such a big difference the new finish makes!

As you can see, @Cybertruck production is also ramping quite nicely today … perhaps getting ready for resumed big deliveries to customers in late-May or early June the lower cost AWD version.

English

My reasons for investing Intel in 20s is simple. China take over of Taiwan is close. America needs its own high end Chip maker. Intel has invested billions and was verge of 18A production. Stock price was at its lowest because multiple. sometimes we dont need to over think.

English

Dan retweetledi

AMD will beat earnings by 25% or more. I wont be surprised if they even hit 2$ EPS. CPU demand and price increases will drive the profits

English

@BenBajarin Following company details product line time lines and competitive moat very closely has helped multiple 5 baggers. X has helped in this case as i follow mutiple niche experts

English

The perils of only being able to analyze balance sheets and not technology as well.

Polymarket Money@PolymarketMoney

Nvidia’s market cap has now increased by more than $2.15 trillion since Michael Burry began shorting the stock.

English

@mzuhair123 14A client announcement will be big. I also think Sambanova inference partnership has some surprise cooking.

English

Interesting…

According to GSR, Intel has told Chinese CSPs that CPU supply will be extremely tight over the next two quarters, but should stabilize toward year-end. However, Chinese CSPs reportedly view that timeline as overly optimistic and are preparing for a prolonged CPU shortage.

English

@danielnewmanUV Yes. Bought in to the stock today. They already shipping ARM cpu for laptops. It should not be hard for DC.

English

$QCOM should get a boost from launching a DC CPU. A much needed one. 💪🏻

Jukan@jukan05

Rumor: Qualcomm’s ARM data center CPU is scheduled to launch in June.

English