Ankur Shrivastava

1.8K posts

Ankur Shrivastava

@ankoors

Seed VC @mvcapitalvc | Co-founder @globevestor | Investor @ Springboard, Agnikul, Chakr, GHC + 40 more | @bcg @iitbombay

Toronto, Ontario Katılım Ağustos 2009

553 Takip Edilen1.5K Takipçiler

@anushkaa3011 Bumrah for impact, Abhishek for fun, Pant for X factor. But Virat’s still there!

English

Ankur Shrivastava retweetledi

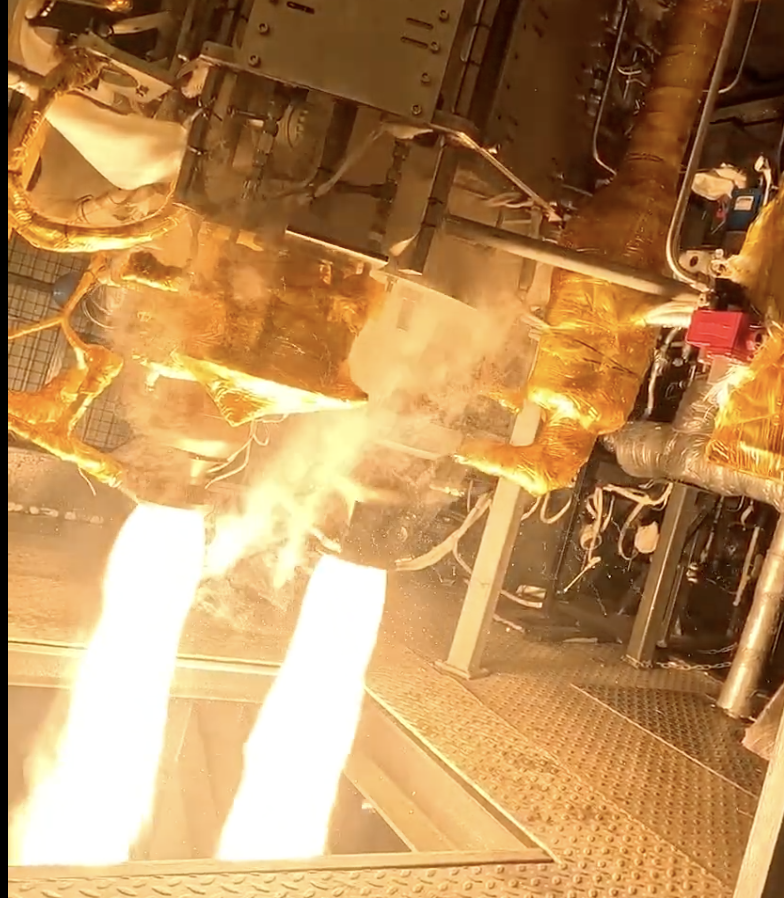

Humbled to announce that we have raised $17M in our latest funding round — supported by amazing partners including Advenza Global Limited, HDFC Bank, Pratithi Investments, Artha Venture Fund, and several others.

Rewinding a bit - the response to our controlled ascent test launch has been both energising and overwhelming. Multiple customers have expressed interest in riding with us to space. This momentum has inspired us to move faster and challenge the conventional boundaries of launch technology.

As the global launch market rapidly evolves, with the support from ever inspiring @isro & the always enabling @INSPACeIND , we are committed to building a future where no part of our rockets are wasted. Reusability will no longer be a distant goal — but an objective in our very next mission.

With this funding, we will now start our expansion at the recently allocated land near the upcoming Kulasekarapatnam launchpad. Thanks to the continued trust of the Tamil Nadu State Government.

We have come a long way but there is a lot more to be done to democratize space access. Getting to orbital velocity looks more attainable than ever with this new Dollar DeltaV infusion!

@srinathr155 | @moin_spm | #SatyaChakravarthy

@iitmadras | @iitmrp | @IITMIC | @startup_mission | @IndiaDST | #TDBIndia | @ANRFIndia | @Guidance_TN | @TN_SIPCOT | @TIDCO_1965

#Agnibaan #Agnikul #AgnikulCosmos #StartupIndia #MakeinIndia

#madeinIndiaForTheWorld #resuability #newspace #kulasekarapatnam #deeptech #rockets

English

Ankur Shrivastava retweetledi

Excited to announce @mvcapitalvc's investment in Beyond Renewables! ☀️

Solar power is usually linked with zero emissions, low maintenance & long life. That’s indeed true, but only up to a point. Solar PV panels have a lifespan of 25-30 years, though some break sooner (weather, defects, bad installation). And for the first wave of solar power adoption, that end of life is now on our doorstep. As millions of these panels reach end of life, a solar recycling crisis is emerging — one we’re ill-prepared to handle, globally.

Why aren’t we recycling solar panels? They're designed to be durable & difficult to take apart. A panel includes tightly bonded layers of glass, silicon, metals (aluminum, copper), precious metals (silver), polymers, and hazardous metals (cadmium, lead, antimony & tin). It takes a lot to disassemble these bonded layers without destruction. Today, India relies on mechanical extraction (largely informal sector), which can economically recover only low-value aluminium, glass & copper. The rest is sent to landfills, where toxic materials can permeate the environment. It’s also highly wasteful & inefficient.

In India, the government has proposed rules to handle end-of-life PV recycling & thrust EPR responsibility on producers. But due to the absolute lack of recycling tech & infra, many producers/developers are a host to unending heaps of broken/used panels now, just waiting for someone to recycle them properly.

Manhar, Vedant & team are confronting this problem directly with their proprietary, eco-effective recycling process that achieves over 95% recovery of high-value materials from panels. Their innovative thermal-chemical treatments extract aluminum, glass, silicon, copper, and precious metals like silver with high purity. Bharti, Atharva & I are proud to back them on their mission to lead the way in changing the solar recycling paradigm in India. And happy to have Oorjan Cleantech, Gautam, IIMA Ventures and other like-minded investors on board.

@entrackr announcement: lnkd.in/gZexX7MW

#climate #solar #recycling #circularity

English

@dineshpaii Appreciate the work you guys are doing in supporting ideas that transform the world for good.

English

Venture capital has always been about building the future. Channelling capital into bold ideas and backing bets that radically improve existing solutions. Yet, somewhere along the way, it became an assembly line focused mainly on returns. Seed investors seek signals to attract Series A, Series A investors look forward to Series B, and the cycle continues. There’s nothing inherently wrong with this approach, but it’s worth remembering that the true essence of venture is in chasing radical outcomes, not just IRRs.

A frequent discussion within the team at @Rainmatterin is how sectors like manufacturing, deep tech, and others with moonshot potential require a different kind of approach. One with lots of patience. Instead of simply hunting for the next round’s signals, investors should ideally back ideas capable of shaping tomorrow’s world.

To be fair, we’re starting to see such a shift. We’ve met investors lately who are underwriting risks they wouldn’t have considered 4-5 years ago. We are meeting individual contributors building communities that founders can benefit from. But we need more of this. Returns are certainly important, but it should be the byproduct of making a meaningful impact, not the sole objective.

It makes me wonder how we have an opportunity as a country to really support moonshots, entrepreneurs who deserve an opportunity, and those who truly attempt to build the future.

English

Ankur Shrivastava retweetledi

Ankur Shrivastava retweetledi

Why we invested in Focal 🔦

Focal is an innovative startup with a vision to heat people, not spaces. It creates smart, high-efficiency, electric, spot heating systems that provide personalized warmth to people in all environments. Think spotlight, for heat!

English

Ankur Shrivastava retweetledi

India, Canada to collaborate on renewables, industrial decarbonisation, plastic pollution, chemicals management & sustainable consumption. Also to promote investment in clean fuels, grid modernisation & clean tech, incl. green hydrogen & carbon capture. 🙌

tribuneindia.com/news/world/ind…

English

@IndiaQuotient @Goyal4Gagan @anandlunia @sinhamadhukar @kanika_agarrwal @sahilmkkr @mohmit2706 @MadhavMalani11 @ShahKanupriya Congrats @Goyal4Gagan and team!

English

We have raised a new $129 Mn Fund 5!

Since 2013, we’ve held onto one simple belief: Indians can build the best products for Indians.

For too long, the narrative was: India is too complex. Indians don’t pay. Indians won’t change. Indians only love imported products.

We have always disagreed. The insights, grit, and ingenuity to solve these problems come from founders with a high IndiaQuotient.

We will continue to back founders long before their ideas become “sectors.” This has been true from the early days of India social, brands, content, digital lending, India software, agritech, and many more. We were the first investors in ShareChat, Sugar Cosmetics, Lendingkart, Kuku FM, and Vyapar.

We want to invest very early.

Before you launch.

Before you make a deck.

Before you get an idea.

Before you leave your job. (Okay, not this one!)

As we start investing from our Fund 5, here is Our Manifesto:

1. Embrace risk. Be the first one to invest.

2. Play the long game. Make money only through long-term company success.

3. Back the founders at every step. Bridge funding, pro rata or whenever they need us.

4. Cut the fluff. No monthly decks, no big meetings, no wasted founder time.

5. No pressure for up rounds, high dilution, or early liquidity.

6. Focus on PMF. Not on vanity metrics.

7. Be very selective. Every deal is very important to the firm.

8. Always be available. No secretaries, no calendars.

9. Patience. Moral support and empathy in tough times.

10. No conflicts. No competing investments, and if a situation arises, always be transparent.

With the new fund, we are also expanding our leadership team with Kanika Agarrwal and Sahil Makkar joining Anand Lunia, Madhukar Sinha, and Gagan Goyal as Partners—to do more deals, bolder and crazier!

If you’re a founder with the ambition to build a lasting institution, we want to hear from you.

Idea/ deck/ prototype/ beta—it’s never too early to reach out to us.

Write to us at [first_name]@indiaquotient.in

English

Ankur Shrivastava retweetledi

Ankur Shrivastava retweetledi

When you have a hammer, everything looks like a nail.

When you’re a VC, everything looks like a capital problem.

In the early days of Valar, a lot of VC’s passed on us because they didn’t believe we could raise the money. In one way, they were totally right. We raised less than a lot of our compatriots.

But in a much more fundamental way, they were very wrong.

You see, capital is not the only advantage a team can have. A team that is moving twice as fast needs half the operating capital per milestone. A team with intimate knowledge of the industry can spend a third of the CAPEX to get to the same place.

Weirdly, I believe that this dynamic is more true in hard tech than software.

A lot of software dollars end up going to sales and advertising, which is a really tough space to innovate on. You may occasionally see breakout successes with teams who know how to work the channels of earned media and vitality, but it rarely ever passes out of a normal band of acquisition cost.

In this lens, the market capture advantage of having an extra $200 million in the bank begins to overshadow everything else: the details of the product, the quality of the team, etc., especially as software gets increasingly easy to build.

I believe this has trained investors to overweight the importance of capital advantage. Particularly in deep tech, there’s a minimum amount of money needed to get to the next lamp post. Adding tens or hundreds of millions on top of this is a marginal benefit, and is generally not enough to offset more fundamental dynamics.

I’m reflecting on this as I think back to some of the early partners I wanted to get on board and could not because of this capital advantage fear. I was a young upstart out of nowhere with very well funded competition.

But in the last two years, the Valar team has made insane progress on 1/10th the capital we were told it would take. Now, because of that, we’re getting to a place where capital is easy to access too. Pretty soon we will have that advantage as well, as well as all the others. (I still don’t think it will be the most important).

I think I feel compelled to write this out because it feels important to the soul of what makes the American tech ecosystem so great to course correct away from this. The argument can be made very selfishly: Valar will be a fund returner for those early believers, and there are others like it just getting started. But more fundamentally, the whole *idea* of tech investing is to find the Davids who are building slings. The fact that the Goliaths are more capitalized is what makes them juicy targets.

VCs are beginning to sound more like bankers and less like pirates. This seems bad. We should figure out how to course correct from that.

My favorite investor consistently reminds me: “There’s a lot of money in the world. You can have as much money as you want. Is that actually what’s blocking you right now?” Usually it’s not.

English

Ankur Shrivastava retweetledi

"In the early days of Valar, a lot of VC’s passed on us because they didn’t believe we could raise the money."

Yes, VCs will pass on a company out of fear that other VCs will pass on it. This is institutionalised insecurity.

Venture capital emerged from opportunity of frontier technologies; huge idiosyncratic risk, huge upside potential. Power law meets portfolio strategy.

Today it is dominated by low-agency herd animals that have traded that opportunity away for easier personal enrichment and job security.

Instead of independent judgement, and the implicit accountability, they outsource to the collective via market signals that manifest in everything from round pricing to discourse online.

This exposes venture capital to major systematic risk, unmanageable via portfolio design, exacerbating the boom-and-bust nature that leg-sweeps the market every few years.

That's a taste of how problematic this behavior is. It gets much worse.

The influence of signals fundamentally erodes the quality of decisions and the competence of investors.

This basic economic principle is described by Keynes in "The General Theory of Employment, Interest and Money", and Abhijit V. Banerjee, in "A Simple Model of Herd Behavior", both cited in the article below.

tl;dr — At some point, if signals are a significant driver of activity, and incentives aren't well designed, the market becomes a snake eating its own tail. All that matters is a mindlessly recursive consensus.

Thus began the financialisation of venture capital; the point at which the opportunity mutated from chasing great investments to chasing pools of LP capital with "venture banks" as the brokers.

This is why from 2010 to 2022, a period of generational abundance, venture capital produced increasingly bloated B2B SaaS companies and monkey JPGs. Technological stagnation.

Capital that could have gone to reindustrialisation, to energy or biotech, was instead recycled through fragile ARR-printing machines into bigtech profits.

Farming markups to raise more capital to farm more markups — progress be damned.

This is all a direct result of the incentives.

Indeed, these incentives are powerful enough to manifest as market capture:

Implicitly, the VC media playbook that has emerged over the last decade allows firms to develop influence over signal-driven activity.

Explicitly, research looking at VC activity indicates that firms who refuse to play along are strategically frozen out of capital networks.

Evidence of this behavior is everywhere. Most investors have never known anything else.

The following sentiments are all gateways for this financialisation and the associated market capture:

- Venture capital is a relationship business

- Access is all that matters

- The best deals are competitive

- Entry price doesn't matter

- Consensus is good, actually

Indeed, many established practices (like pricing on ARR multiples) are symptomatic of this problem, reflecting a goal of exploiting badly designed incentives (concentrating capital and power) rather than chasing outlier outcomes.

Venture capital will continue to fail entrepreneurs, innovation and LPs (especially in times of abundance) until these incentives are addressed.

There are exceptions, such as the early believers in @isaiah_p_taylor, but those exceptions should not make the industry complacent about glaring structural flaws and obvious failure.

Frustration with this issue led me to write "Why venture capital should be consensus-averse", at around the same time @valaratomics was getting started:

Isaiah Taylor - making nuclear reactors@isaiah_p_taylor

When you have a hammer, everything looks like a nail. When you’re a VC, everything looks like a capital problem. In the early days of Valar, a lot of VC’s passed on us because they didn’t believe we could raise the money. In one way, they were totally right. We raised less than a lot of our compatriots. But in a much more fundamental way, they were very wrong. You see, capital is not the only advantage a team can have. A team that is moving twice as fast needs half the operating capital per milestone. A team with intimate knowledge of the industry can spend a third of the CAPEX to get to the same place. Weirdly, I believe that this dynamic is more true in hard tech than software. A lot of software dollars end up going to sales and advertising, which is a really tough space to innovate on. You may occasionally see breakout successes with teams who know how to work the channels of earned media and vitality, but it rarely ever passes out of a normal band of acquisition cost. In this lens, the market capture advantage of having an extra $200 million in the bank begins to overshadow everything else: the details of the product, the quality of the team, etc., especially as software gets increasingly easy to build. I believe this has trained investors to overweight the importance of capital advantage. Particularly in deep tech, there’s a minimum amount of money needed to get to the next lamp post. Adding tens or hundreds of millions on top of this is a marginal benefit, and is generally not enough to offset more fundamental dynamics. I’m reflecting on this as I think back to some of the early partners I wanted to get on board and could not because of this capital advantage fear. I was a young upstart out of nowhere with very well funded competition. But in the last two years, the Valar team has made insane progress on 1/10th the capital we were told it would take. Now, because of that, we’re getting to a place where capital is easy to access too. Pretty soon we will have that advantage as well, as well as all the others. (I still don’t think it will be the most important). I think I feel compelled to write this out because it feels important to the soul of what makes the American tech ecosystem so great to course correct away from this. The argument can be made very selfishly: Valar will be a fund returner for those early believers, and there are others like it just getting started. But more fundamentally, the whole *idea* of tech investing is to find the Davids who are building slings. The fact that the Goliaths are more capitalized is what makes them juicy targets. VCs are beginning to sound more like bankers and less like pirates. This seems bad. We should figure out how to course correct from that. My favorite investor consistently reminds me: “There’s a lot of money in the world. You can have as much money as you want. Is that actually what’s blocking you right now?” Usually it’s not.

English

Ankur Shrivastava retweetledi

Why we invested in CarbonStrong.

CarbonStrong is a novel advanced materials co that's on a mission to decarbonize concrete w/o impacting performance, via its innovations in CO2 injection in concrete & engineered cement substitute binders.

Read more: mvcapital.vc/carbonstrong-w…

English

The second level effects of climate change — Australia's rainforests are releasing more carbon than they absorb, warn scientists bbc.com/news/articles/…

#climatechange #rainforests

English

Another approach to increase wood strength, arguably the strongest yet. At scale does this save steel emissions or lead to deforestation or make sense with sustainable forest management — remains to be seen. cnn.com/science/superw…

English

Ankur Shrivastava retweetledi

Excited to share that @confidohealth has raised its $10M Series A led by @BlumeVentures! They are on a mission to reduce the huge workload of healthcare workers using AI, and have made big strides in the past year. Wishing them lots of further success! 🚀

English

Ankur Shrivastava retweetledi

🚀 Transforming US Healthcare: Confido Health Raises $10M (~₹85Cr) Series A

@confidohealth (Fund V) has raised $10M in Series A funding led by us at Blume Ventures. The round saw participation from new investors Schema Ventures and Vicus Ventures, along with existing investors Together Fund, DeVC, and Medmountain Ventures. Strategic healthcare operators @innovaccer and @memorahealth also joined the round.

Founded by Chetan Reddy and Vichar Shroff, Confido Health is transforming patient communication in US healthcare through AI-powered autonomous voice agents. The company specialises in handling patient scheduling calls, which comprise 30-40% of all healthcare provider inquiries, achieving a remarkable 95% resolution rate without human intervention.

The fresh capital will fuel the development of new use cases and accelerate growth initiatives. The company has demonstrated impressive traction, growing revenue 10x this year and expanding its patient base from 150,000 to over 1 million since December.

"It almost feels like a landgrab out there right now," says Chetan Reddy, CEO of Confido Health. "Our round will fund the development of new use cases and enable us to pursue growth as quickly as possible."

Sanjay Nath, Partner at Blume Ventures says, “It is clear to us that healthcare especially in the US is ripe for AI-led transformation, given the widespread administrative staff shortages, and Confido is well positioned to 10X the patient experience.”

As healthcare providers struggle with staffing challenges, Confido Health is emerging as a transformative solution, significantly reducing patient wait times and streamlining healthcare communication. Their AI-powered platform is revolutionizing how healthcare providers interact with patients, making healthcare access faster, smoother, and less stressful for everyone involved.

Read the full press release here: forbes.com/sites/davidpro…

@BKartRed @AshishFafadia @sajithpai @sanjaynath

@arpiit @riashroff @saritaraichu @mehtaalok @mitul_am @SeekingN0rth @DeepikaDakuda @gauthamsiv @ray_elton99 @vikramg05 @sumangalv @shreyshah2301 @sameeraculous

English

Just heard at Toronto Climate Week -- Yes, AI is hot. You know what else is hot? The planet. 🙂 #torontoclimateweek

English