Sabitlenmiş Tweet

🚨 First Substack drop!

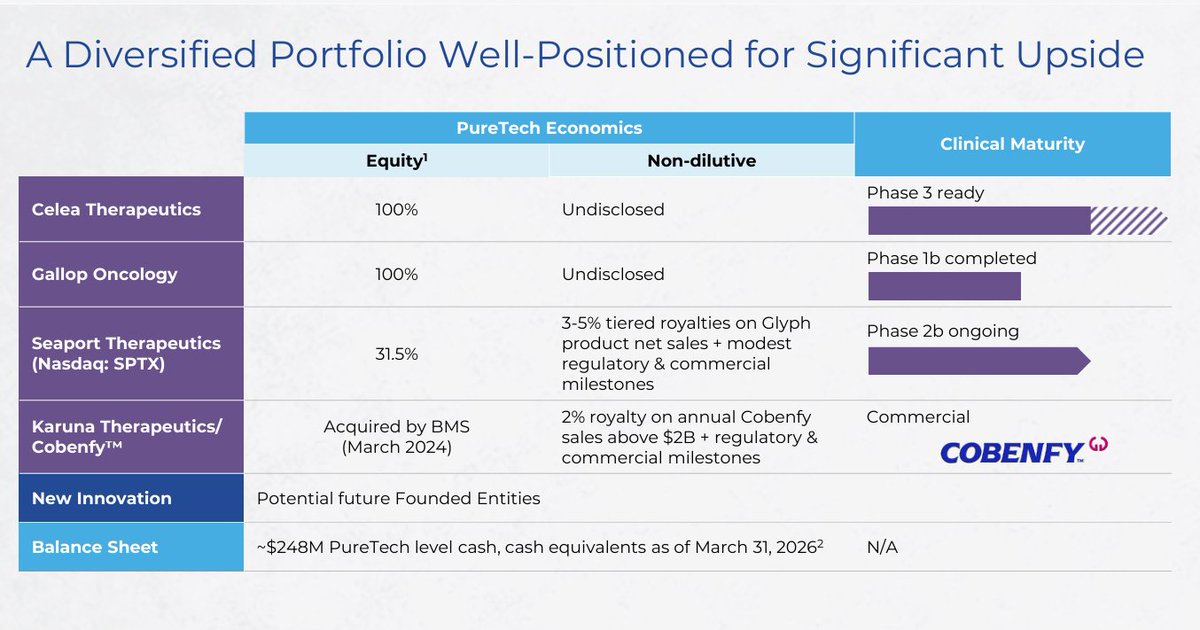

$PRTC.L #PRTC PureTech Health

💰Cash runway to 2028+ portfolio of 3 mid & late stage multi-bn dollar assets priced at ZERO.

🚀Why this biotech disconnect screams opportunity:

#biotech @SeaportTx @daphnezohar @PureTechH

open.substack.com/pub/mrchrisarc…

English