0xZach

244 posts

The May #silver OI is going the wrong way.

It needs to approach zero in the next two weeks and it grew yesterday.. 46,877 contracts represents 234m oz. of silver.

Across all contracts theres 118,370 contracts representing 590m oz. of silver.

There is 76m in registered silver.

English

CL

makes sense to own a bit of the back end and barbel it with a combination of XLE (for the majors) and (more operationally leveraged) smaller swing producers for more beta factor

English

English

Here are the Q4 2025 earnings release dates for SILJ's top 10 holdings (as of Feb 6, 2026):

1. Hecla Mining (HL): Feb 17, 2026

2. First Majestic Silver (AG): Feb 19, 2026

3. Coeur Mining (CDE): Feb 18, 2026

4. Wheaton Precious Metals (WPM): Mar 12, 2026

5. Endeavour Silver (EXK): Mar 10, 2026

6. KGHM Polska Miedz (KGH): Mar 25, 2026

7. Perpetua Resources (PPTA): Mar 18, 2026

8. Boliden AB (BOL): Feb 3, 2026 (reported)

9. Pan American Silver (PAAS): Feb 18, 2026

10. Buenaventura (BVN): Feb 26, 2026

Dates may vary; check official sources for updates.

English

SILJ

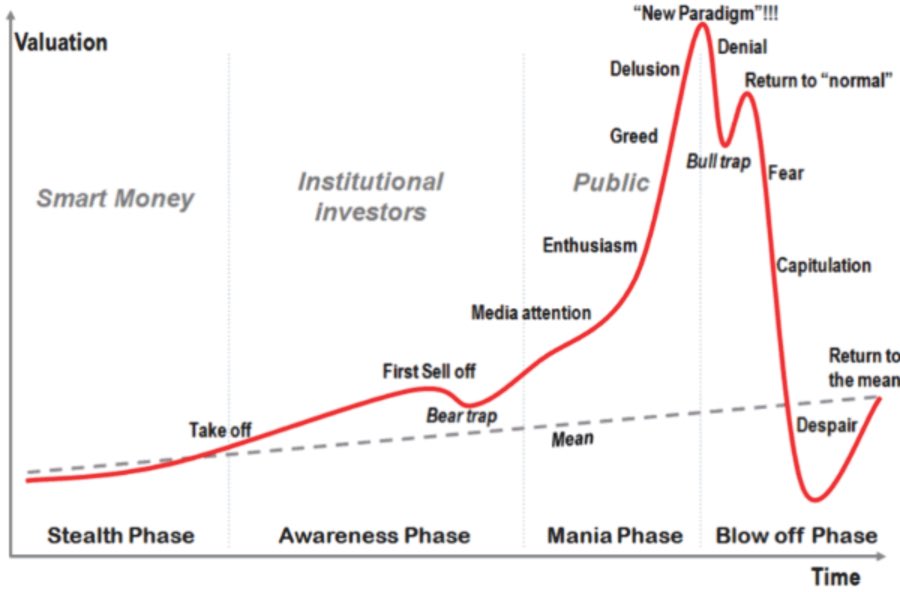

THE FACTS THAT EVERYONE IS MISSING:

Less than a year ago, average silver AISC ≈ $20/oz.

At $25 silver, miners earned $5/oz.

A 10M oz producer = $50m in annual operating profit.

At $85 silver?

Same producer’s Margin = $65/oz.

Same producer’s operating profit = $650m.

That’s a 1,200% increase in cash flow on a 240% move in the metal.

This is operating leverage in its purest form.

HISTORY IS CRYSTAL CLEAR:

2002 - 2011 silver bull market (facts):

Silver: $4.60/oz in 2002, peaking at $47.94/oz in April 2011. Approximate gain of +900% at the peak.

Pan American Silver (PAAS): approximately $3-$4 per share in 2002, peaking around $40-$45 per share in 2011. Equivalent to roughly 10-12×, or +900% to +1,100% at the peak.

Silver miners (sector wide): historically ~3× the performance of the metal at cycle peaks, driven by operating leverage and earnings re-rating.

Yet in 2025:

Silver +300%

SILJ ~+200% (relative underperformance)

WHY?

Analysts are still modelling $35-40 silver using backward looking val methods.

That changes imminently as miners report earnings at today’s price during Q4 earnings.

First Majestic is the textbook case: high beta, primary silver exposure, cost base largely fixed. Every $1 move in silver now drops disproportionately to free cash flow.

Silver lags gold.

Silver miners lag gold miners.

That lag is not permanent.

Physical demand is visible:

Absolutely nobody can buy physical for $75

This is not a “trade”.

This is a cash flow repricing event.

When earnings print, the equity gap closes violently. That’s what I expect…

Silver miners won’t just catch up after Q4 earnings… They are more than likely to overshoot and possibly lead during the next leg of this silver bull market

English

0xZach retweetledi

0xZach retweetledi

Metaplanet Q2 Earnings Results:

- Revenue ¥1.239B ($8.4M) +41% QoQ

- Gross Profit ¥816M ($5.5M) +38% QoQ

- Ordinary Profit ¥17.4B ($117.8M) vs. -¥6.9B

- Net Income ¥11.1B ($75.1M) vs. -¥5.0B

- Assets ¥238.2B ($1.61B) +333% QoQ

- Net Assets ¥201.0B ($1.36B) +299% QoQ

English

0xZach retweetledi

0xZach retweetledi

I think will be 15555 BTC next 😉

Metaplanet Inc.@Metaplanet

*Metaplanet Issues 30 Billion JPY in 0% Ordinary Bonds to Purchase Additional $BTC*

English

@ActuallyClimber @global_hodl Appreciate the reply and explanation. Cheers Climb.

English

@attaksz @global_hodl It essentially is. They’ll get paid for the exercised warrants (at least 30m shares around $10 a piece) tomorrow. They front ran that with a bond. It’ll all be easier to keep track of once the plan truly begins.

English

Gotta update more charts! MetaPlanet had 5k bitcoin when I bought in less than 2 months ago, and now has 11,111. More than a double. Get ready for another double soon, likely in July if I had to guess 📈

English

@ActuallyClimber @global_hodl Just realised that the fully diluted share count remained at 759mil in the disclosure.

Meaning this 1111BTC isn't part of the 555mil Plan?? @ActuallyClimber am i analyzing it right??

Omg means that there's a lot more to come?

English

@global_hodl lol you blinked.

They got 1111 more announced an hour ago.

English

0xZach retweetledi

Haters will say this isn't biblically accurate.

English

0xZach retweetledi

#moonbubu is live!

ca- CgzuFAhXZxfj2jnDJ3YMcqZnDueztL3mzzEW4x2Vpump

10,000,000 $moonbubu will be equally distributed among first 555 to retweet and drop wallets !

English