Income Tax India@IncomeTaxIndia

KIND ATTENTION TAXPAYERS

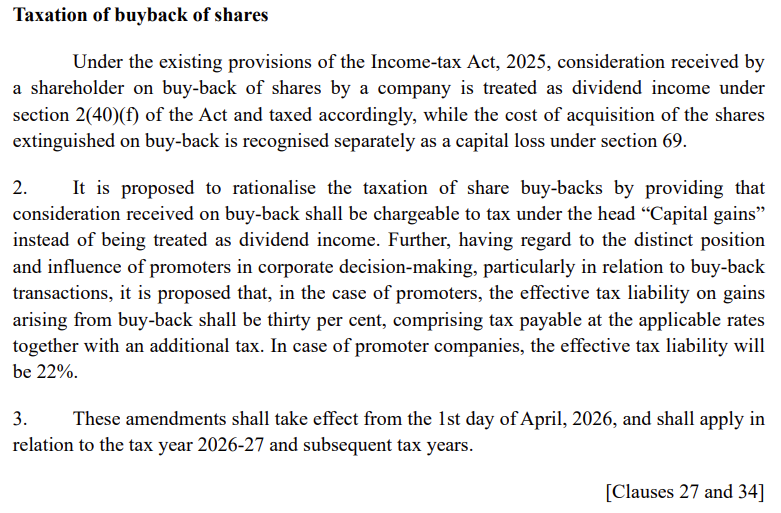

1. Buyback was presently taxed as dividend but extinguishment of share was treated as capital loss.

2. This posed problems to small shareholders who had no capital gains to set off the loss.

3. Also, buyback conceptually is in nature of capital gains.

4. Therefore, in Finance Bill 2026, buyback treatment is changed to capital gains.

5. Shareholders other than promoters will pay tax on such gains at the applicable capital gains tax rate. That is 12.5% for long term capital gains, listed and unlisted. 20% on short term listed, and applicable rate on short term unlisted.

6. However to prevent promoters from misusing the buyback, they have to pay additional income tax.

7. Where domestic company is a promoter, they will pay effective tax of 22% on gains on buyback.

8. Where promoter is other than domestic company, they will pay effective tax of 30% on gains on buyback.

9. This scheme will be beneficial for small shareholders.

10. For promoters, the tax liability will largely remain similar if it is taxed as dividend in their hands.

11. On the whole, the buyback taxation has been simplified with benefits to small shareholders.

@nsitharamanoffc

@officeofPCM

@FinMinIndia

@PIB_India