@Bubblebathgirl It’s a cult worshiping pedos, slave owners and killing. Who gives a fuck about this moron.

English

Befreeandwealthy

865 posts

@befreenwealthy

Value / growth focused. Long time $TSLA shareholder. Focused on $OPEN and other companies misunderstood by the market.

President @realDonaldTrump and @SecScottBessent, and @pulte, I have a simple idea on how to lower mortgage rates and spreads: One of the unique features of U.S. conventional mortgages is that they are prepayable at any time without a penalty. While this feature is attractive for homeowners, it comes at a significant cost as buyers of mortgage backed securities (‘MBS’) require a significant increase in spread to compensate them for giving the borrower the option to prepay at anytime. Why don’t Fannie and Freddie also offer non-prepayable mortgages where if the borrower wishes to prepay the loan, he would have to pay a prepayment penalty? I asked one of my friends who is an expert and large investor in MBS what the estimated savings today would be on a 30-year Fannie/Freddie mortgage if the borrower would be locked out from prepayment other than by paying a penalty? He estimated that the savings would be about 65 basis points. So a borrower could have a choice: Obtain a 30-year prepayable mortgage at today’s ~6% rate, or at a 5.35% rate, but with the obligation to pay a prepayment penalty if he/she refinanced in the future. The loan could also be made to be portable so that if the home is sold, the new borrower could assume the loan and no prepayment penalty would be owed on a sale. While the ability to prepay is a valuable option, locking in the 65 bps savings upfront over the life of the mortgage may be the difference between the borrower being able to afford the home and not being able to. You could imagine that there could be different versions of this product where the lock out would be for 5 years, 10 years etc. (with different levels of savings for each, the longer the lockout, the greater the savings) and the borrower could custom design the mortgage and its prepayability to meet their life plan. As you know, commercial mortgages work this way. Why couldn’t the same approach be used for home loans?

$ANGX ANGEL ACHIEVES TWO MILLION GUILD MEMBERS MILESTONE stocktitan.net/news/ANGX/ange…

🍳 Special dishes take time — this isn’t instant ramen. @nejatian & team still cooking $OPEN.

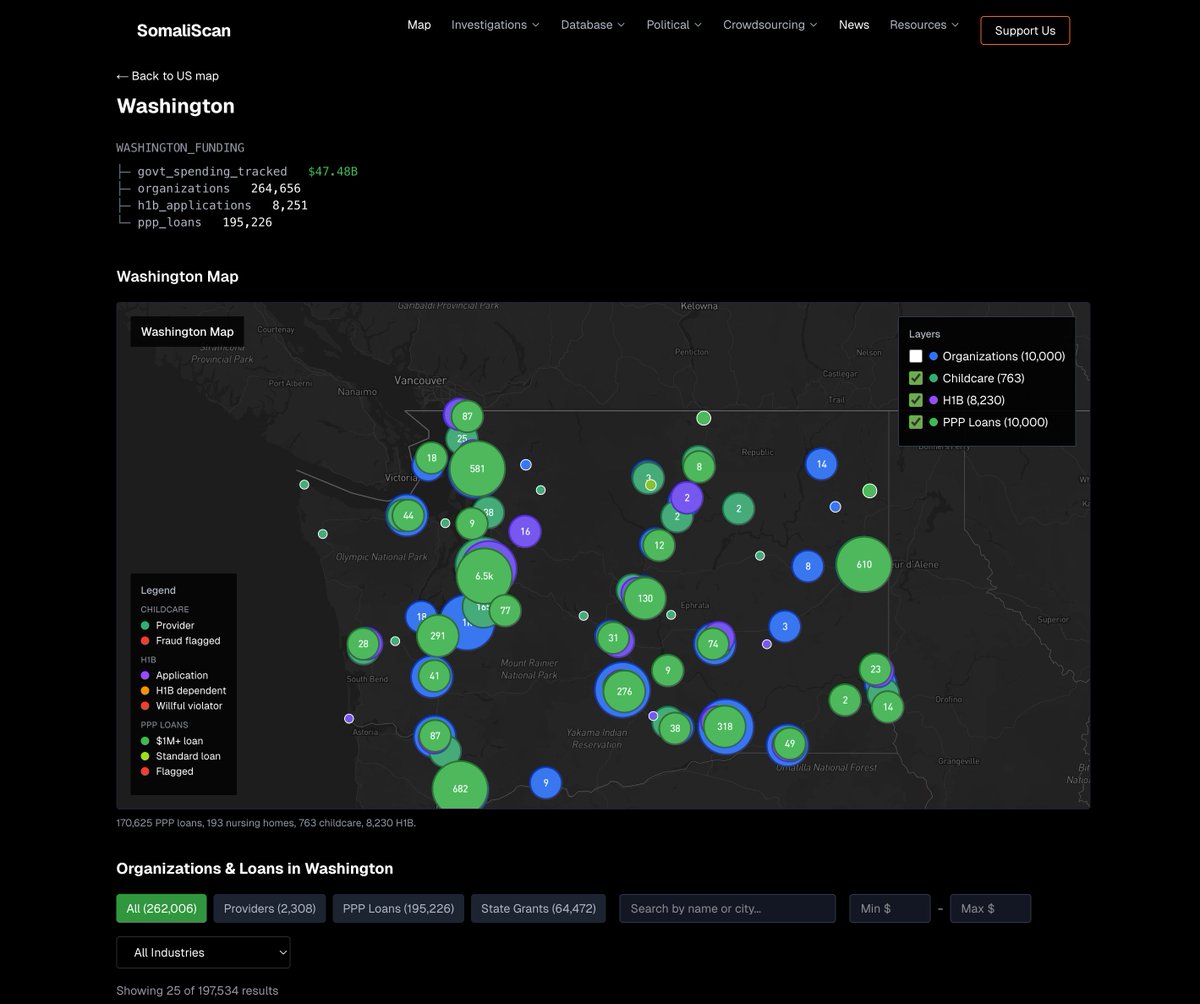

🚨 Here is the full 42 minutes of my crew and I exposing Minnesota fraud, this might be my most important work yet. We uncovered over $110,000,000 in ONE day. Like it and share it around like wildfire! Its time to hold these corrupt politicians and fraudsters accountable We ALL work way too hard and pay too much in taxes for this to be happening, the fraud must be stopped.

$OPEN now $65.3m ahead of revenue guidance QTD vs expected. Current as of today: $514.5m Expected this time in the QTR: $449.2m 206 homes to sell at current avg sale price of $376k 21 days left to go.

$OPEN + Accountable. Acquisitions tracking within 6% of High Plan. They are fighting tough seasonals as far as volume goes. Setting up for a big ramp in q1/q2.