@Zero2HeroStocks @preetkailon Korean market is helping. Samsung +6% and SK Hynix +8% right now.

English

Bitus Capital

26 posts

@bituscapital

Inversor amateur. Opinador profesional.

$MU Now Comes The Real Test Broke 700 support yesterday and today's first test at open was a big fail. Couldn't flip it. As I mentioned earlier, 650/630 is really the only zone with any real history on this chart. Big mover = not much volume traded across the range but THIS zone had consolidation. Price remembered it. Quick bounce right off 650. Now the question is simple can bulls flip 700–720 back to support? You need close above with momentum not wicks. That's the line. Above it, structure repairs. Below it, we're still in trouble. Also worth noting $NVDA earnings tomorrow. Could move the whole tape. Watching closely.

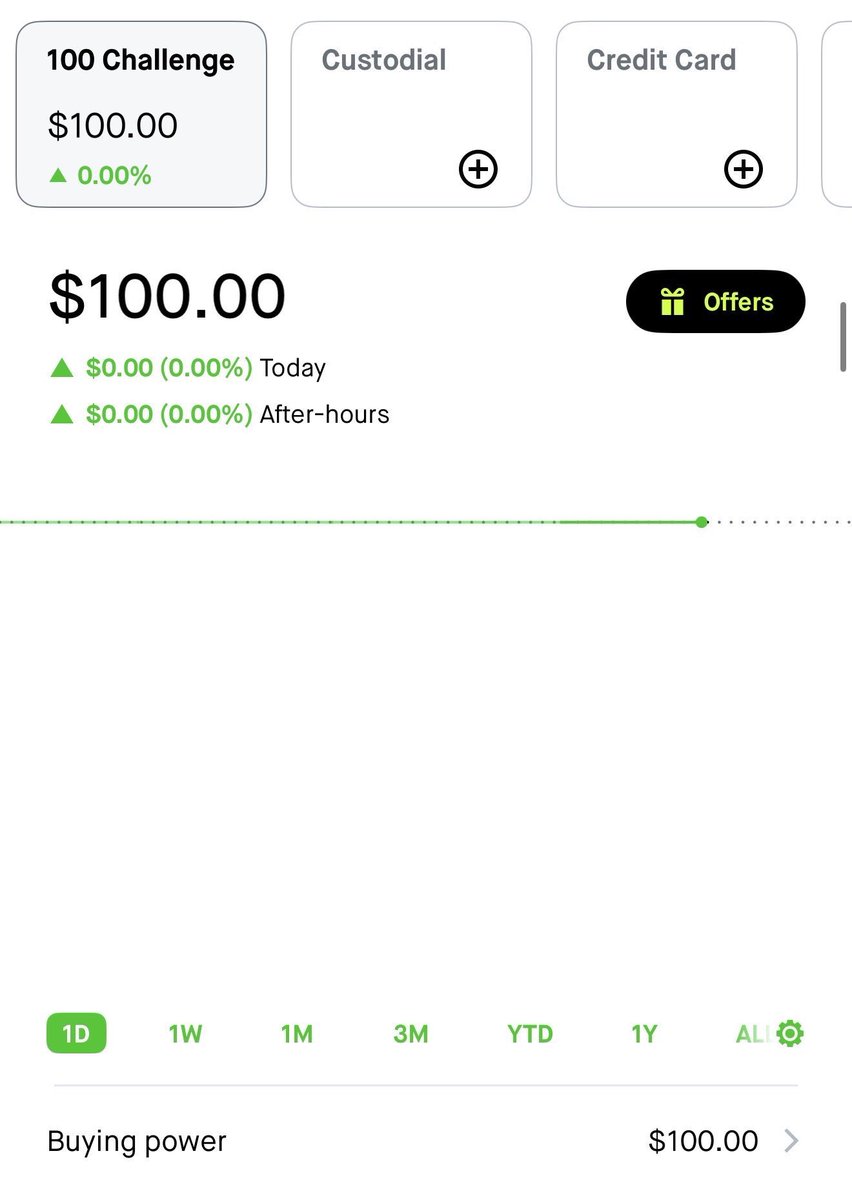

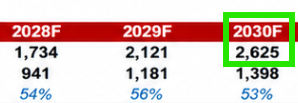

$1.4 trillion. That is Nomura's 2030 Data Center ONLY memory revenue estimate. Seems a little aggressive but I will take it. $MU $SNDK $DRAM

$MU Honestly, we are in living in a time where people think this is normal And FOMO'ing that they did not chase this. This is as parabolic as you'll see and this is a $817 BILLION MARKET CAP company Yes we are in a bubble, yes they will all collapse and yes this time IT IS NOT DIFFERENT.

$MU Honestly, we are in living in a time where people think this is normal And FOMO'ing that they did not chase this. This is as parabolic as you'll see and this is a $817 BILLION MARKET CAP company Yes we are in a bubble, yes they will all collapse and yes this time IT IS NOT DIFFERENT.

PEG RATIO SEMICONDUCTORES. PEG < 1 La acción podría estar subvaluada respecto a su crecimiento. PEG > 2 comienza la zona de peligro ⚠️ (sobre valuación). FÓRMULA PEG = P/E Ratio ÷ Tasa de crecimiento esperada de ganancias (por lo general 2-5 años).