From your lips to Jane Streets trading platform.

DYOptions@data168

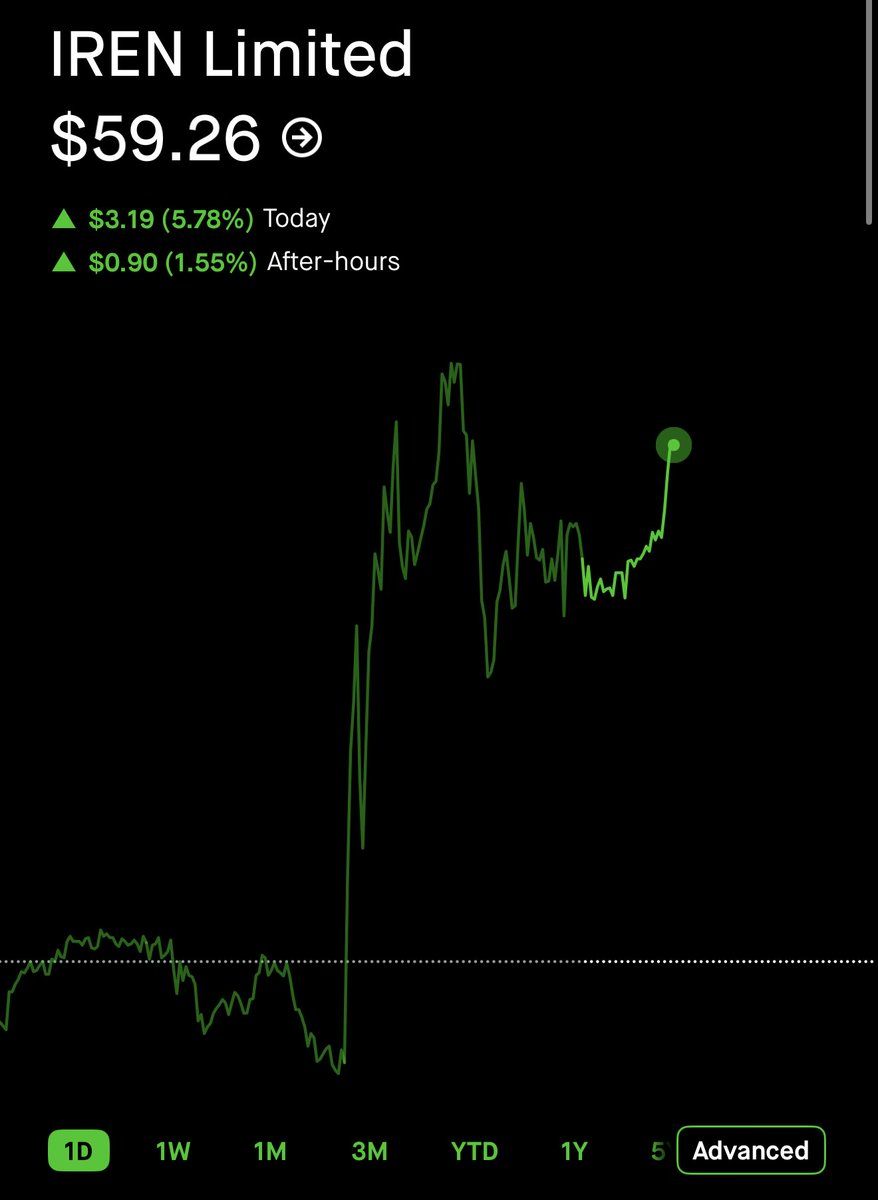

$IREN bond sale closed. The journey begins. 10% day tomorrow. Mark my word!

English

Curls

8.4K posts

@blcurley

https://t.co/4Hfzgsnnez $BTC $IREN #miningmafia

$IREN bond sale closed. The journey begins. 10% day tomorrow. Mark my word!

What’s that @IREN_Ltd 👀👀👀 $IREN

$IREN Partnering for the Long Term Growth Most people, including myself, woke up Monday morning caught off guard by the new convertible bond offering and asked why management decided to issue so close announcing $NVDA and not let the share price appreciate with the new outside interest. That my friends characterizes a short term mindset which I am constantly trying to recondition myself to avoid. @Umbisam helped me reconsider my perspective and come away with a greater appreciation and empathy for what Dan, Will and the team are trying to accomplish. @danroberts0101 @kentpdraper often speak to the the 3 Cs of $IREN to communicate how the company will grow: 1) Capacity 2) Customers 3) Capital The most underrated characteristic of these intertwined components remains their bias for a long term time preference. 1) Capacity - High quality data centers that can survive multiple generations of GPUs 2) Customers - Mixing hyperscalers with the ability to do multiple projects (maybe $MSFT 🇦🇺) with younger startups and enterprises with the high potential growth trajectory that will call $IREN home (think @FireworksAI_HQ ) 3) Capital - Finding investors that understand the long term vision and will contribute funding multiple rounds to build the 5+ GW of capacity Management purposely issued the convertible right after earnings for the long term benefit of $IREN. Issuing the notes at a lower price offers a 🥕to note investors. Negotiations went something like this: Dan: "Mates, we need $2.6B for our new DCs" Noteholders: "Dan, what's in it for us?" Dan: "Give me a low interest rate of 1% and I'll give you guys the right to convert your debt into equity at 32.5% higher than $55. You will have the right to convert at $73 which is higher than today's price, but wait until you see what we have coming to market in the next few months" Noteholders: "Great Dan, make it $3B. We cannot wait for you to sign Sweetwater and the remainder of Childress" This whole dance while inconvenient in the short term price action serves a greater purpose. Dan will need to go back to market for more money to fund his vision and needs repeat investors. I appreciate @Umbisam helping me change the lense in which I viewed the financing. The same reason I give discounts to some of my regulars on their 🥩is the same reason Dan executes in a particular manner. Repeat business. Long term infrastructure funded by long term capital providers to serve long term customers will provide us equity holders plenty of returns if we remain patient.

$IREN Prices Upsized $2.6 Billion 1% Convertible Senior Notes Due 2033 @IREN_Ltd announced the pricing of its upsized private offering of $2.6 billion in 1.00% convertible senior notes due 2033 (increased from the previously announced $2 billion). Key Terms: - Coupon: 1.00% (paid semi-annually) - Maturity: December 1, 2033 - Initial Conversion Price: ~$73.07 per share (32.5% premium to the $55.15 closing price on May 11, 2026) - Conversion Rate: 13.6848 ordinary shares per $1,000 principal - Capped Calls: Entered with a cap price of $110.30 (100% premium) to reduce dilution upon conversion Proceeds & Use: - Expected net proceeds: $2.57 billion ($2.96 billion if the $400 million option is fully exercised) - ~$174.5 million to fund capped call transactions - Remainder for general corporate purposes and working capital The notes settle on May 14, 2026. This move provides IREN with significant low-cost capital to support its AI cloud and data center growth.

$IREN being named the flagship deployment for NVIDIA's DSX architecture at the 2GW Sweetwater campus is a massive deal. This validates IREN's vertically integrated approach across power, land, data centers and GPU operations, exactly what NVIDIA needs in a partner to scale AI infrastructure globally. This gives IREN the credibility to unlock institutional financing, attract hyperscaler deals, and secure priority GPU allocation. It's in NVIDIA's own interest for IREN to succeed, because IREN SW1 site is now expected to be their flagship showcase for DSX architecture.