Benjamin retweetledi

The owner of the S&P 500 index is licensing the world’s most tracked stock index for the launch of a derivative contract that trades around the clock on the crypto exchange Hyperliquid on.wsj.com/4bezxK0

English

Benjamin

1K posts

@blockchain_benj

Calculated Dgen X is my Bloomberg Terminal Graduated airdrop farmer

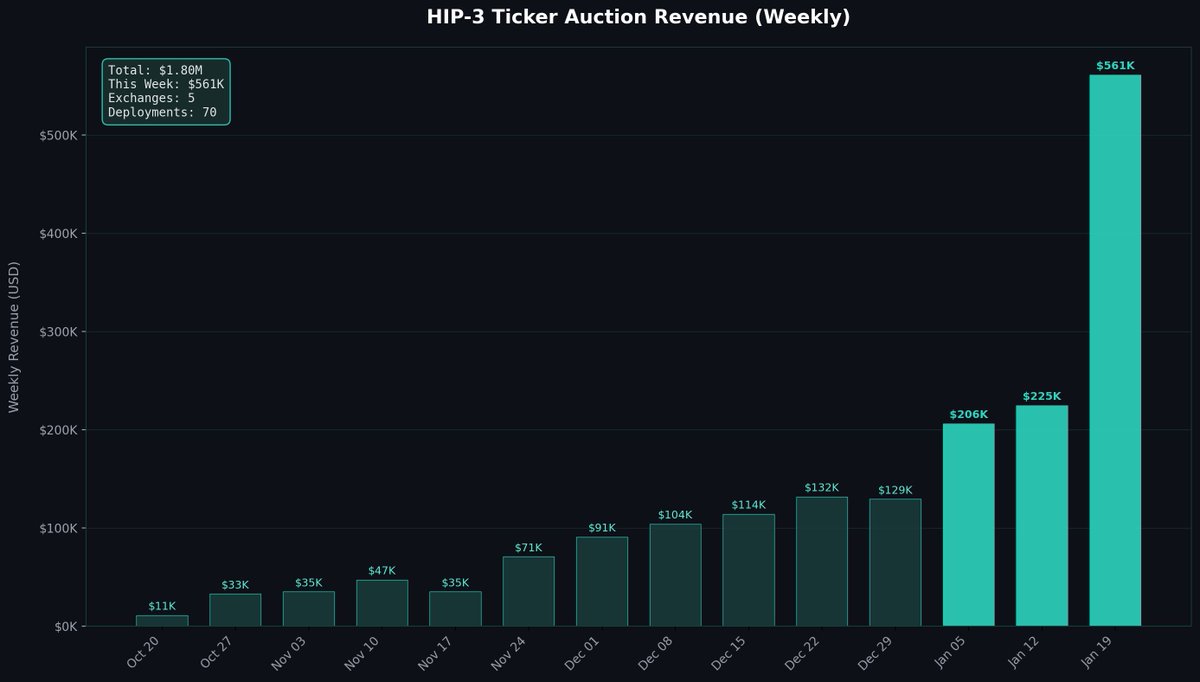

Introducing Byreal Perps: 24/7 RWA and crypto perpetuals, onchain. Go long or short on gold, silver, oil, stocks, and crypto, with up to 40x leverage. Deep liquidity powered by @HyperliquidX. Try now: byreal.io/en/perps

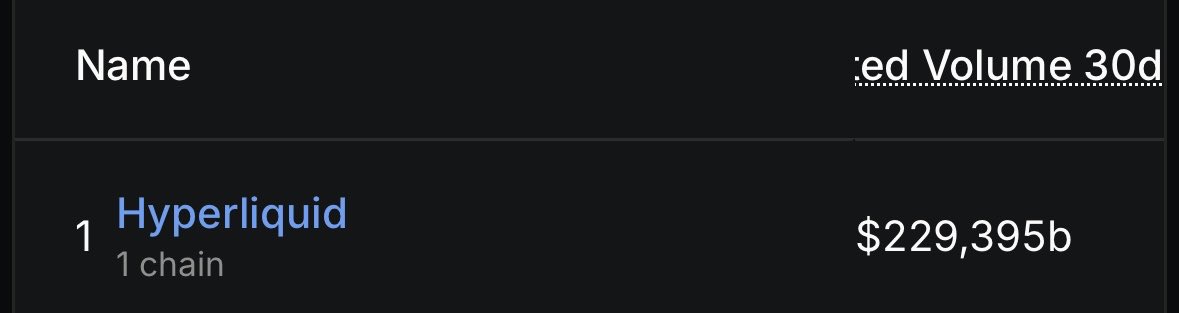

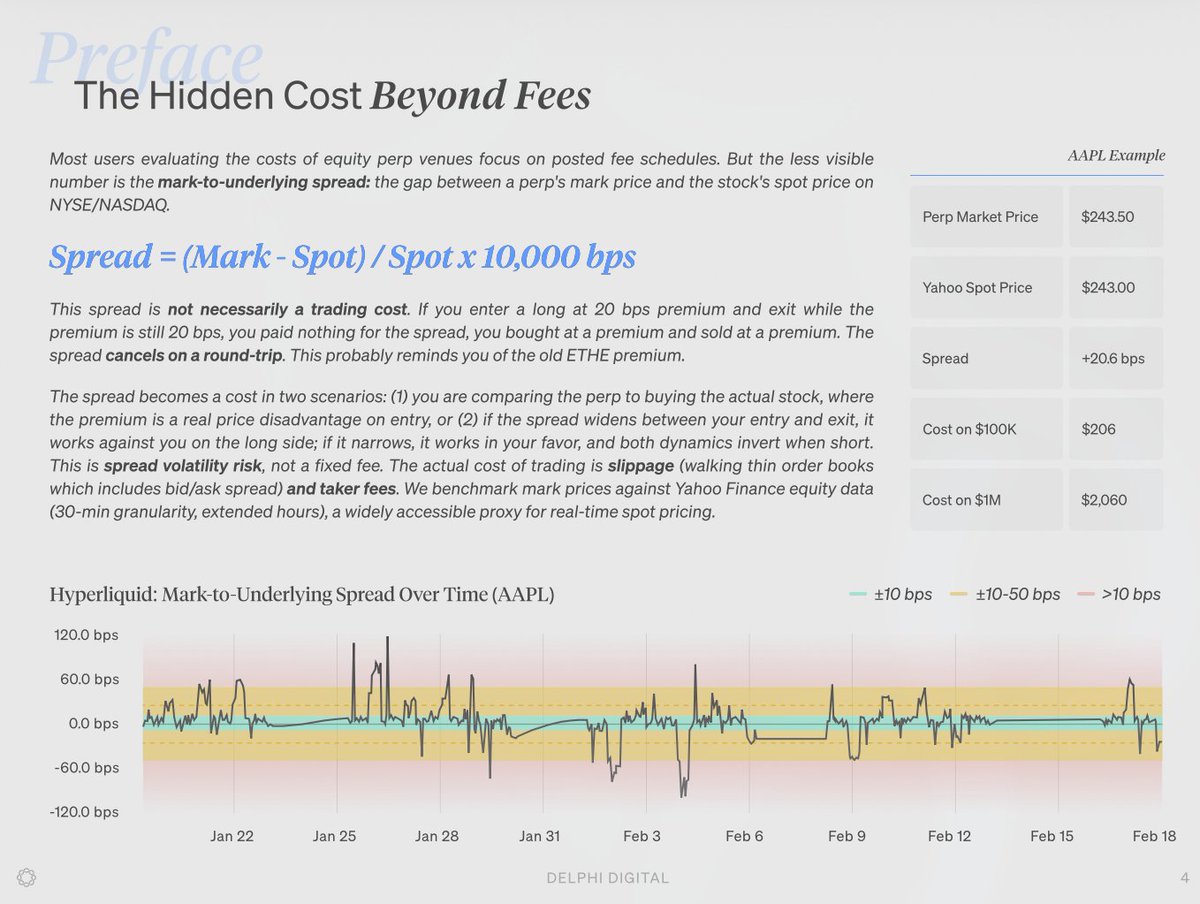

Equity perps continue to get a bad wrap by most people and the common critique is that funding is expensive, order book depth is bad, and the mark-to-underlying can be incredibly volatile at times. And I would have to say that all of these are largely true today. Equity perp funding runs 11-31% annualized while IBKR CFDs cost 6.5%. @HyperliquidX & @Lighter_xyz order books are 10-100x thinner. So yeah, if you froze markets today and assume no innovation, the picture is pretty dire but I think if this is the future you subscribe to you forget about what just happened last year with the crypto perp basis trade. The other hidden cost people fixate on is the mark-to-underlying spread. Initially I thought this was an incredibly high hidden cost but after digging into it more I don't think it really matters all that much. It is more akin to a closed-end fund premium, similar to what ETHE was for a period of time. For traders, assuming you enter and exit at a similar spread, it isn't a cost. It is just something to be mindful of, especially if you tend to be an emotional person who just apes. And despite all of this - the high funding, the thin books, the spread noise - for directional traders none of it really matters if you capture the move. So what will close these gaps and inefficiencies? I think it is quite obvious that it will be the same thing that closed the gap and inefficiencies for crypto perps, which was the basis trade. Before BTC spot launched on Hyperliquid, BTC funding averaged ~18% annualized, and within months it compressed to ~9%. ETH followed the same arc. Nearly 50% reduction in carry cost driven by one change that allowed arbitrageurs to collect interest rate-agnostic yield by going long spot and short the perp. This flow deepened the order book, anchored the price to the actual underlying assets, and compressed funding. Equity perps today look like crypto perps in 2024. Everyone had the same critiques that funding was too expensive, books too thin, and too much basis risk. And for funds this really did matter and kept many from using these product. And then spot launched and all these inefficiencies were quickly fixed. The same is likely to happen with equity perps. We have the NYSE moving towards 24/7 trading, which will help. We have US regulatory clarity coming this year, which will help. And we even now have the CFTC chief explicitly talking about clearing a path for U.S. perps.