@billgrass1 The real driver is proving demand and PMF through the sales pipeline, and better alignment with shareholder value would go a long way. Clear win-win that's being left on the table.

English

Brian Pemble

500 posts

@bpemble

Ex-FB eng leadership. Optimist. À chacun son goût.

Forum is executing on a clear roadmap to bring real-world assets on chain at institutional scale. We are initially focused four high-value vertical markets: auto loans, manufactured homes, aerospace equipment and commerical real estate. The Karus warehouse facility - fully secured first-lien auto loans originated through Automatic USA - is another step in generating yield Our business model runs on four economic engines: ✅Yield ✅Origination Fees ✅Asset Management Fees ✅Transaction Fees

🛫Eurus Aero Token I from ETHZilla Aerospace is live. Aviation meets Blockchain. Real jet engines. Real lease revenue. Real yield. ✈️CFM56 engines with Major U.S. Air Carrier 💵~11% target rate of return based on holding for full term of the lease 🇺🇸 Monthly USD payouts 🪙Initial price of $100/token (minimum 10 tokens) on liquidity.io for accredited investors

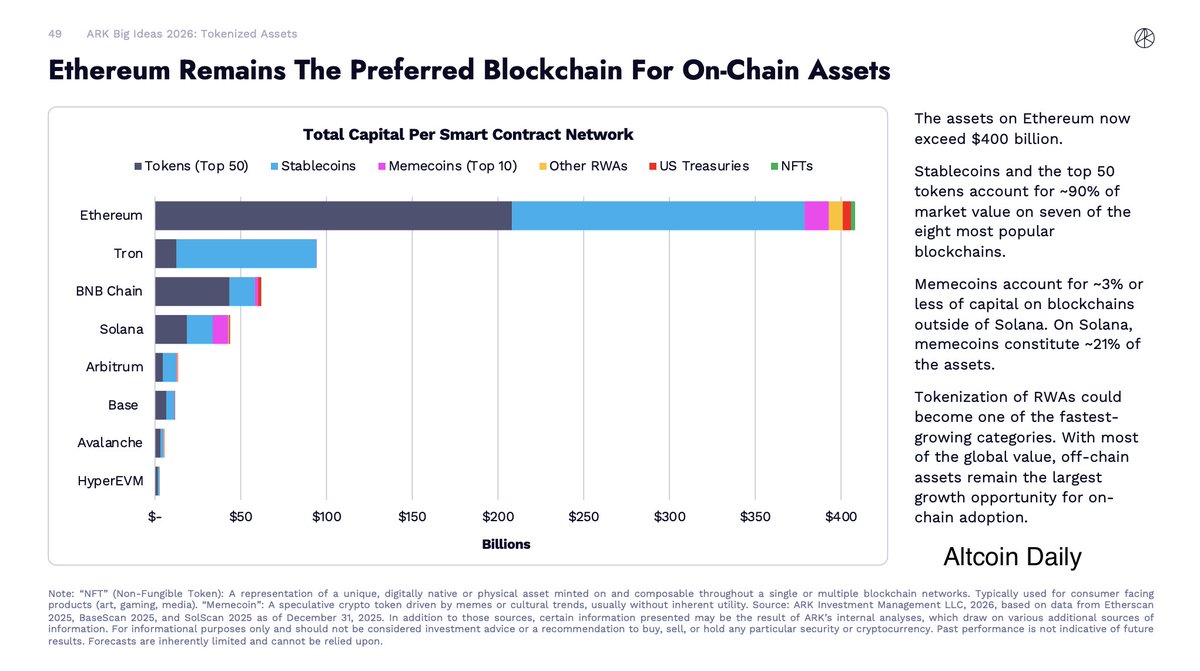

ETHEREUM SEEN OUTPERFORMING BITCOIN Standard Chartered says Ethereum’s outlook has improved and it is likely to outperform bitcoin. While weak bitcoin performance has weighed on the broader crypto market, rising institutional demand for ethereum and its dominance in stablecoins, real-world assets, and DeFi support a stronger outlook. Increased network throughput and potential U.S. regulatory clarity could provide further upside. The bank forecasts ethereum at $7,500 this year and $30,000 by 2029.

“Manufactured homes represent an affordable housing solution, a compelling yield opportunity, and an ideal fit for our on-chain securitization framework,” said McAndrew Rudisill, CEO. @NatMortgageNews by @Colinmcnamara05 nationalmortgagenews.com/news/ethzilla-…

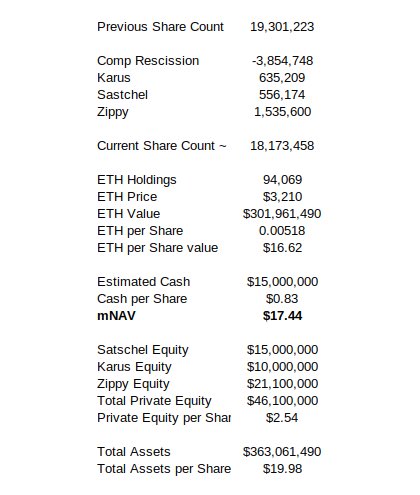

I think I’ve figured out what’s going at $ETHZ and why they are acting this way. Somewhere along the way of building their DAT, @ETHZilla_ETHZ made a deal with Hudson Bay. It seems HB spotted an inexperienced finance team and got them to sign a deal where they’d be guaranteed to make money in any scenario as Ethzilla was desperate to try and catch up in the DAT race. At some point, likely after they increased their convert position, HB started hedging their investment by being short, triggering a worst case scenario for ETHZilla which saw its mNAV disconnect. There were ways to fight back and clear this hurdle but Rudsill didn’t. At some point it became apparent to him that there would be a sharp payout to HB out of NAV. That’s when he decided to get the focus away from NAV and onto multiples as the DAT battle he deemed lost. Realising the DAT business failed, they began hastily piecing together a tokenization business around Liquidity IO and just preserving the ETH on their balance sheet. Ever since, Rudsill is essentially not telling a narrative around ETHZilla but around Liquidity IO. Every action he is taking is around building out Liquidity IO, not ETHZilla (I would be curious how the cap table looks there and who are other shareholders of Liquidity) Despite only owning 15% of Liquidity IO, ETHZilla is taking very agressive measures to develop that platform, going as far as to buy overpriced stakes in other businesses to get them to list tokens and talks up the future of tokenization. Whereas the real beneficiary will be Liquidity IO and not Ethzilla that owns only 15%. All companies being acquired by Ethzilla have a relationship to Saatchel (the owner of Liquidity Io). ETHZilla in fact is going as far as to say it will invest the actual money to get the assets needed on its books for Liquidity to later tokenise exclusively on its platform. In its latest interview, Rudsill said ETHZilla would take home loans and other RWAs on its books before it tokenised. He also said there would be a couple more deals similar to Zippy to add aerospace and real estate as tokens for Liquidity. So in reality, every possible action is being taken at great cost to build out the Liquidity platform whereas Ethzilla shareholders will only benefit in part if that works. So while everyone is busy thinking of Ethzilla’s balance sheet, Rudsill is busy trying to find ways to get Liquidity’s platform to scale at any cost. Why is another question worth looking for an answer. As selling ETH to make investments in auto loans or startups that will list on Liquidity would cause havoc. Rudsill found another way. He issues shares, which are essentially backed by real liquid assets to sellers as payment, so as to in theory hold the balance sheet but still « pay » by reducing nav/share. This way he can keep trying to grow the Liquidity platform and not have to sell ETH on paper but still do it in practice. It is likely the next step is to bring on the actual assets on the balance sheet in the same way by issuing stock for them. Of course this is absolutely not the business we invested in and there is a clear conflict of interest with Liquidity Io if this is accurate and a breach of fiduciary in any case. Regarding the comp plan, it’s likely they decided on this after they realised the loss on the HB case and wanted to both cash in before being removed and increase voting power. It is important to remember shareholders control a company not management. And extremely active and rapid steps are currently being taken to resolve this. It is likely the startup acquisitions can be pulled back as they are a breach of fiduciary. The HB settlement will be harder to renegotiate. However, they will now need to close their short ; which should close the discount to NAV to around 14-15. Rudsill and board just need to resign at this point. I’m ready to step in and help fix the ship if needed.