Sabitlenmiş Tweet

bitchute.com/video/AbwsyS3l…

Dublagem sobre as eleições brasileiras do programa na íntegra da foxnews #brazilianspring #brazilianelections

Português

c. alster

23.4K posts

@claalster

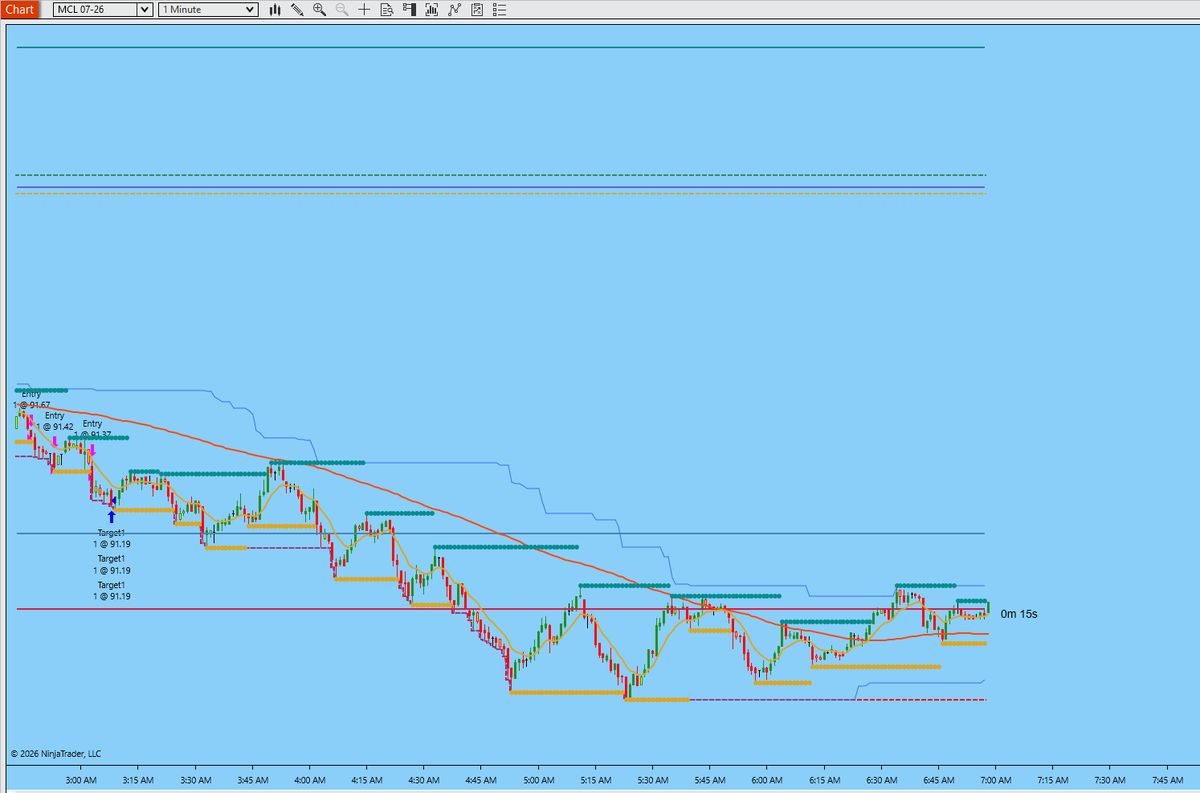

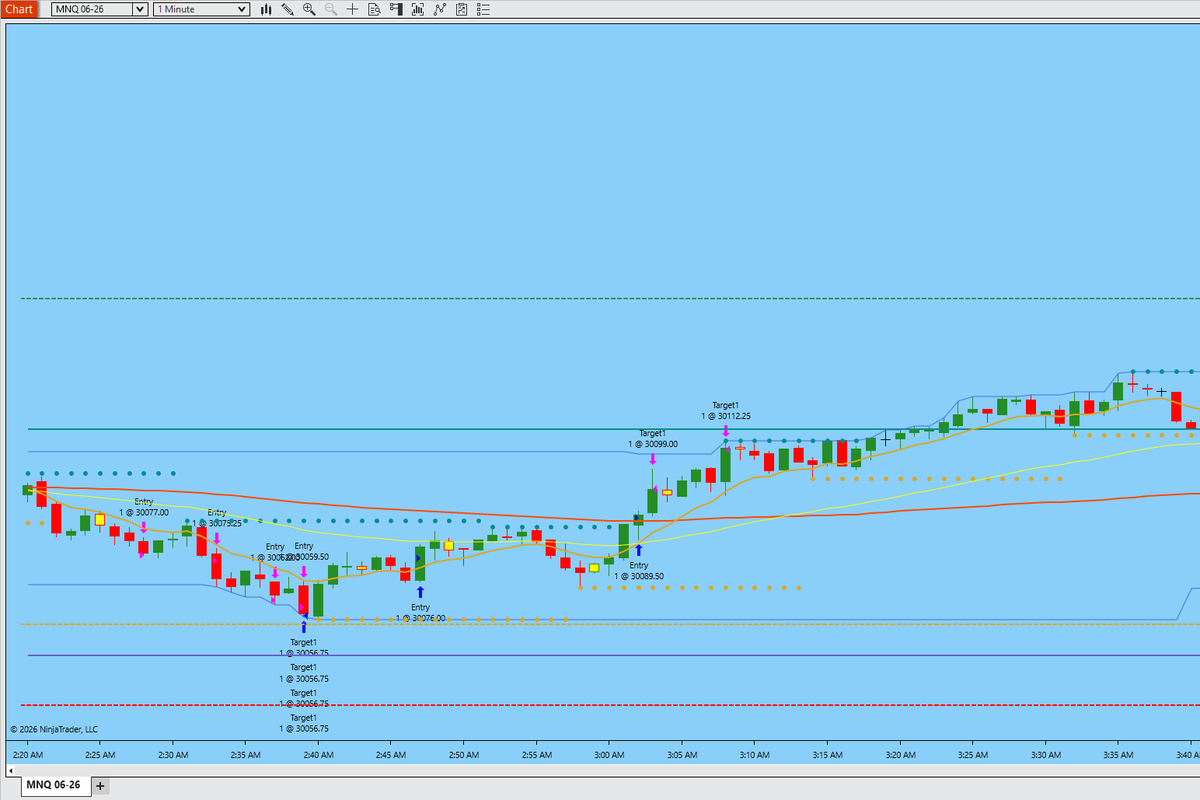

Indicators https://t.co/1mrCXao4gB Bankmath Newsletter available Bankmath videos https://t.co/FmNvlZSuAq

I’ve been grinding away trying to map out China’s recent crude plays, but after going through today's report, I have to hand it to OIES—they scripted the plumbing way better than me. Here is my quick breakdown after running through their print, alongside the Chinese refinery throughput chart to help connect the dots. - Three months into the Hormuz crunch, and Beijing is completely blindsiding the market with its crude playbook. A heavyweight that easily sucked in 11mb/d over the last five years just saw its import prints plunge to 9.3mb/d in April. Now, the forward data says May and June seaborne arrivals are about to crater straight into the gutter at 6.5mb/d. Instead of running its usual playbook of panic-dumping the SPR to backstop the market during a supply crisis, Beijing just completely cock-blocked refiners from touching the strategic vaults, only greenlighting commercial stock draws. To make it worse, refiners aren't even willing to bleed their own commercial inventories, while state traders are acting like total penny-pinchers—happily flipping premium WAF cargoes back into the market and hoarding dirt-cheap Russian barrels instead. This is a complete 180 from the 2021 power crunch, when Beijing panicked and ordered everyone to grab supply 'at any cost.' The heavyweights and policymakers in Beijing clearly think they can outmaneuver this supply shock and keep the economic damage locked down by playing a few smart, tactical micro-levers. China’s true red line for freezing out imports is hardwired to the scale of their run cuts. If they try to copy-paste their five-year average throughput of 14.1mb/d, the exact moment seaborne arrivals drop below 9.2mb/d, they’re trapped—they either have to open the strategic taps wide or start chasing expensive market barrels. Instead, chopping runs by 5% down to a 13.4mb/d baseline is hands-down their most realistic, long-term survival play. In this setup, if domestic crude extraction and pipeline taps keep humming, they can easily coast for a few months without taking a single economic hit, even with seaborne prints scraping a measly 7.9–8.5mb/d, because transportation fuels like gas and diesel will still be taken care of. However cranking run cuts to a nuclear 10% scenario means they could survive without chasing a single market barrel even if seaborne flows dry up to 7.2mb/d—but they'd have to throw petrochemical feedstocks like naphtha and LPG under the bus just to keep gas and diesel flowing, a desperate move that runs on borrowed time and stalls out after a few months unless the whole economy is in a total tailspin. To micromanage this whole run-rate circus, China's refining complex is pulling a highly responsive lever: the yield shift. Beijing explicitly told state majors like Sinopec and PetroChina to ditch chemical feedstocks and prioritize flooding the market with gas and diesel, and these plants immediately saluted by shifting their product yields by several percentage points on a dime. As a result, the real bloodbath isn't happening at the refining gate—it's completely decimating the downstream petrochemical chain. With Hormuz blocked, their seaborne naphtha inflows were already sliced in half, but a 5% run cut is about to bleed domestic naphtha and LPG supplies by tens of millions of tons a quarter, sending a compounding, fatal shock straight through the petchem feedstock backbone. They are keeping wheels turning by guaranteeing gas and diesel, but the squeeze on industrial chemical feedstocks is completely running on borrowed time. To paper over the massive raw material hole in the petchem chain, Beijing is shoving its massive 'Coal-to-Chemicals' complex into the spotlight, branding it as a strategic shield against volatile crude under the 15th Five-Year Plan. Thanks to dirt-cheap, stable domestic coal, inland plants churning out olefins and methanol are running hot to boost volumes, but this quick fix hits a hard ceiling when it comes to replacing lost barrels at scale due to structural bottlenecks. The core infrastructure is trapped deep in the northwestern sticks like Inner Mongolia, meaning slamming those products down to the massive manufacturing teeth on the southeastern coast comes with a punishing logistics and freight premium. Most importantly, coal gasification routes physically cannot clone key aromatics or specialized LPG chemical chains—the feedstock deficit is mathematically locked in. On top of that, the fact that Beijing is sitting on a massive 1.1-1.3 billion barrel pile without tapping it proves that institutional red tape is locking up the plumbing. The 100 million barrels buried deep in dark underground rock caverns—completely invisible to satellites—are almost entirely SPR, requiring endless red tape like complex auctions and market disclosures, so Beijing is hoarding it as a nuclear option. Even for the commercial barrels that are accessible, refiners are terrified to draw down because plotting out the repayment timeframe to replace that crude is a total mathematical nightmare in this chaotic macro environment. Beijing is pulling off a highly calculated micromanagement script here: they are completely freezing out the inventory draw requests from state-owned heavyweights like Sinopec, who are nakedly exposed to global benchmarks and were the first to aggressively slash throughput. Instead, they are using the Shandong teapots as a human shield—handing these independent refiners tax breaks and strict run-rate mandates because they have the flexibility to stomach toxic, illicit Iranian and Russian barrels to cushion the margin bleed. Bottom line, this entire web of macro levers—starving imports, shifting yields, hunting for distressed barrels, and burning through coal-to-chem assets—will keep the lights on and protect the economic skeleton through the peak of summer, but only under that tight 5% run cut baseline that keeps seaborne arrivals pinned at roughly 8mb/d. But with May and June seaborne prints already locked in at a subterranean 6.5mb/d, the expiration date on this makeshift band-aid play cannot stretch into autumn. Short of letting their entire national refining infrastructure suffer a catastrophic meltdown, Beijing is running straight into a hard physical wall. Before late summer wraps up, they will be forced to either open the strategic floodgates and dump their massive stockpiles or make a frantic U-turn right back into the international physical market, chasing heavy volumes aggressively at any price. #oott #iran

Heat oil, relative strength leader.