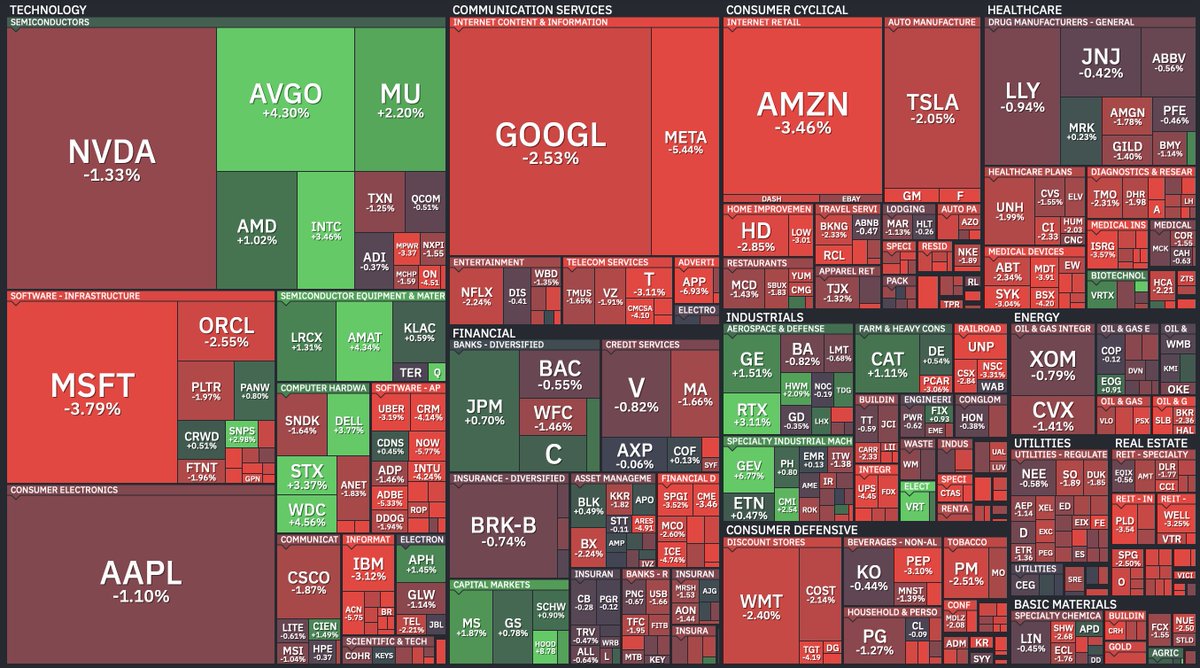

Sabitlenmiş Tweet

Week 1 Portfolio

As of June 9, 2026

Return: +153.2% (2.53×)

This is my record, not a flex. I post the full book every week so the timeline can check whether my principle actually holds over time.

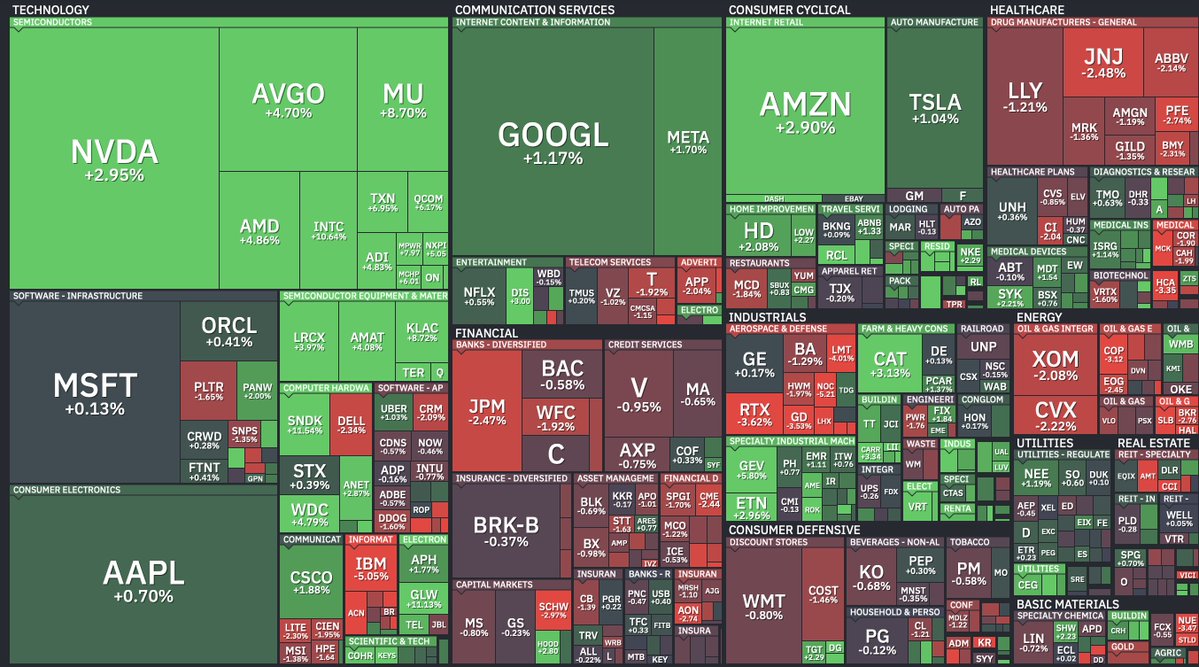

This week's buy plan

I'm looking to add two names, about 4% weight each:

· $ONTO , in the $260 to $270 range

· $FORM , in the $115 to $125 range

When I actually buy them, I'll publish a separate article laying out the full thesis on each, the upside case and where my stop sits. I don't want to add a position here without writing down why, so the reasoning is on record before the result is known.

No sells planned this week.

Current book stays as is.

As always, my analysis can be wrong. I'm just trying to keep buying under the same principle and let probability do its work.

#ClosingBellOrca #Portfolio

English