Cloud San

418 posts

Cloud San

@cloudsan1111

Private investor….

Singapore Katılım Ağustos 2010

294 Takip Edilen45 Takipçiler

What is the most undervalued stock in the market right now?

English

Memory stocks like SanDisk $SNDK are getting pummeled overnight right now…

Someone explain to me like I am a golden retriever why this is??

If they fall further the leveraged longs will get wiped causing them to fall more and the cycle will repeat.

English

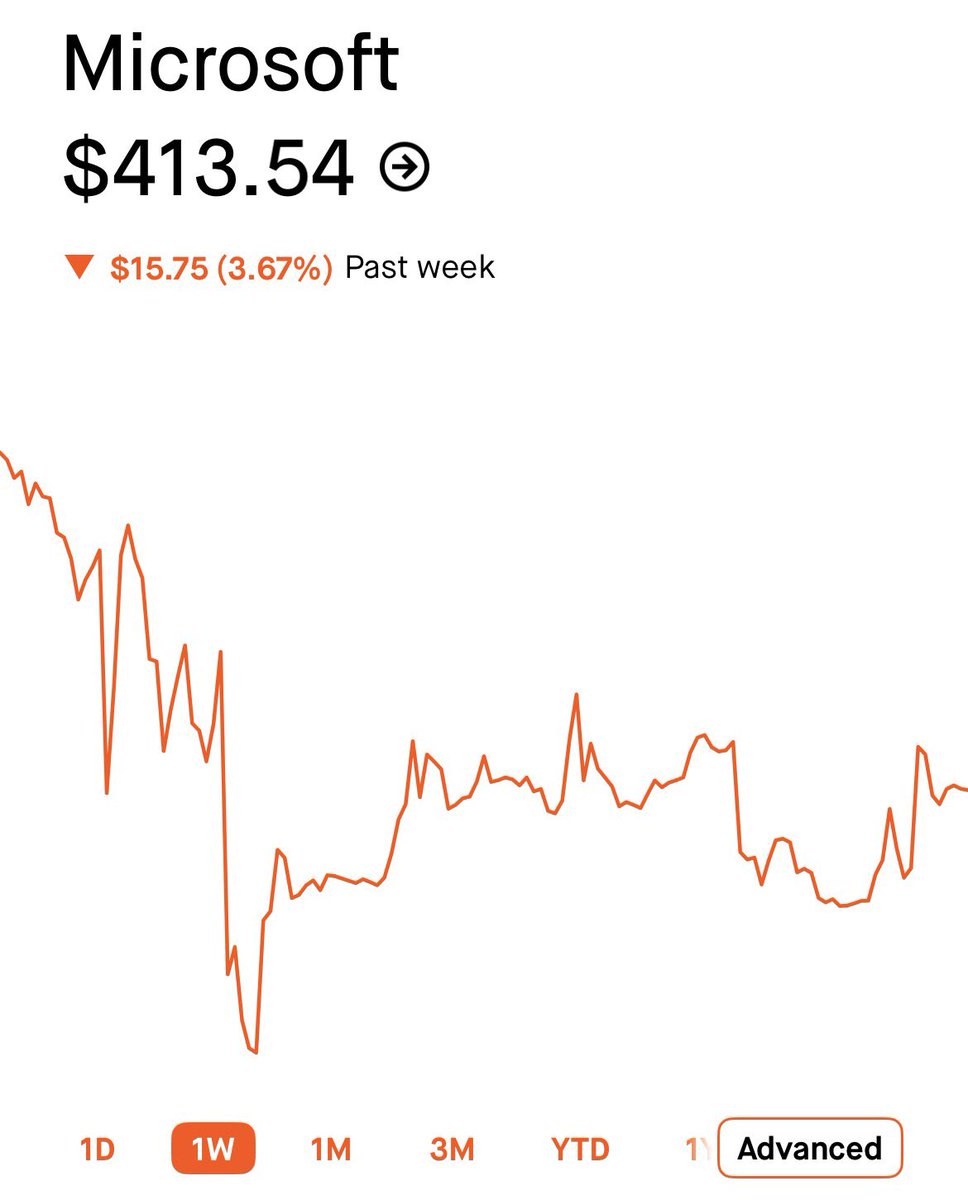

Did everyone just forget about $MSFT???

This company keeps executing, but the market doesn't seem to care.

- Revenue up 18% YoY

- EPS up 23% YoY

- $73 billion of FCF

- $78 billion in cash on the balance sheet

- $630 billion revenue backlog

- 20 million paid Copilot seats

All for only 24x earnings.

The risk reward on this company is undeniable.

English

The problem with chasing $MU and others here is the more something becomes a bottleneck, the more everyone figures out ways to need less of it and bring capacity online, leading to unavoidable excess supply

It's impossible to ignore cyclicality

A crash is inevitable, but where we do not know

English

You got $300,000 to invest right now

Which stock makes you a millionaire by 2030?

1. $AMD

2. $AAPL

3. $SNDK

4. $META

5. $PLTR

English

@DavidANicholas The should be hitting 1500 by end of 2027 before the new capacity comes in

English

Micron is trading at roughly 9x forward earnings while $AMD trades near 60x.

Micron generates about five times more profit, yet trades at roughly one-fifth the multiple.

I believe Wall Street has this wrong, and $MU reaching $1,000 within two years is not out of the question.

English

$AMD $NVDA $INTC $TSM

When HSBC said @intel has better supply chain management than TSMC

Mike@MikeLongTerm

$AMD $INTC $TSM 🥱 The fact that HSBC Concluded $INTC has better supply chain than $TSM is enough said. And they didnt even bother doing research that @AMD secured 30-40% of 2nm capacity. They are mixing up 2nm and 3nm customers together so they can downgrade the stock on people that didn't do research. Here are the facts: 1. Apple is reported to secure>50% of 2nm capacity for Iphone 18 lineup, M6-series Mac chips. Iphone 18 total revenue is expected to be flat at best or fall modestly by 2% vs Iphone 17, so the 50% capacity is unlikely to increase much. 2. AMD EPYC Venice and MI455x are on TSMC 2nm with at least share above 30% 3. $NVDA Rubins are on 3nm 4. $AVGO $QCOM MediaTek are on 3nm as well TSMC’s 2nm (N2) expansion is accelerating dramatically in 2026 . 2 primary 2nm fabs and scaling production to 60,000-65,000 WPM each by end of 2026 or early 2027. And 5 more 2nm fabs ramp in 2026. If Apple Iphone 18 is expected to be flat, so all the new expanding capacity is going to $AMD. Yet the stock is still down 6% because of this stupid downgrade. If $TSM has mad supply chain problem, u would see it on $AMZN $MSFT $GOOGL $AVGO $NVDA earning you stupid moron. That hasn't been the case u said since 2024-2025. Even $INTC is TSMC customer 😂 Not Financial Advice!

English

@DramaAlert He doesn’t have the star power. That aura. He is just someone who looks like MJ. That’s not enough. It’s not something that he can copy. You have to born with it

English

Fabio Jackson demonstrates what his 'Human Nature' performance would have been if he was Michael in the new film.

Is it beautiful? 😭

English

Michael Burry disclosed a new long position in $MSFT.

English

Cloud San retweetledi

China has said US Hormuz blockade is irresponsible.

English

According to a new POLITICO poll, more Europeans view the U.S. as a BIGGER THREAT than China.

TRUMP = MASTERCLASS IN HOW TO MAKE ENEMIES.

English

@amitisinvesting Is he trying to block Hormuz so that the vessels are paying him instead of to Iran ?

English

Trump says US to start blockading the Strait of Hormuz immediately bit.ly/4tedbyY

English