Bravo

2K posts

You literally have to be unemployed to keep up with AI rn

Claude@claudeai

You can now enable Claude to use your computer to complete tasks. It opens your apps, navigates your browser, fills in spreadsheets—anything you'd do sitting at your desk. Research preview in Claude Cowork and Claude Code, macOS only.

English

@HarryStebbings Struggling to use agents to make a difference in personal life, how are you using them?

English

Spoke to a CRO of a hot Series B startup yesterday:

“We don’t have the knowledge internally to implement AI and agents into our process.”

Toast. You are toast. That is unacceptable.

Everyone can learn. There is zero excuse for the above.

English

Here's a thought - software engineering used to be precise and deterministic. We knew that the things we typed would give a certain result.

Coding via prompt is obviously not a 1:1 mapping from prompt to code, and is also nondeterministic. Can code really be repeatedly generated to a high degree of {safety, security, correctness} when it is created at random? Even with guard rails, validators, automated code reviews, etc.

English

@jvisserlabs My Oura ring HRV consistently reads 20 lower than my polar heart strap… have you experienced this before?

English

In my latest HRV Substack, I write about why I purchased an Oura Ring six years ago. Just like the way I built a turbulence model for the market, I wanted a leading indicator to warn me something unexpected may be about to occur in my health. If you worry about the same thing, here is my latest post where you can learn more.

visserjhrv.substack.com/p/your-wearabl…

English

The amount of wealth that has been created by @Revolut and is now in the hands of early employees and investors wild:

>> 2000 Crowdcube investors are sitting on over 645x returns after their £2k investment turned in £1.3m

>> Over 200 employees own shares worth over $1m

>> 20 employees own shares worth over $10m

>> 1 employees own shares worth $80m

>> The company will pay $500m in corporation tax for 2025

And last year over $300m worth of shares were sold by employees

These are like changing sums of money in the hands of retails investors and operators.

Money that then gets re-invested into the economy.

This is tech having a GDP-level impact and why it's so important to have a thriving tech ecosystem here in Europe

English

@ownsomeshares Mexico ✅, India ✅ and Philippines ⏳… 3 of the 4 dominant remittance markets from the US

English

Revolut has secured a Mexican banking licence and is now applying for a US one. 🇲🇽🇺🇸

A fast path to a US licence would materially change the scale of the business.

Mexico/US remittances look like the natural entry point - large, fragmented, and underserved.

I think this is the key to unlocking a US IPO.

Piers@pierslomax1

The Trojan horse into the US market? Congratulations to @Revolut on their first fully licensed bank outside of Europe. The US/MEX remittance market is still by far the largest globally so this could well be a game changer and their main point of entry tinyurl.com/revolut-mexico…

English

English

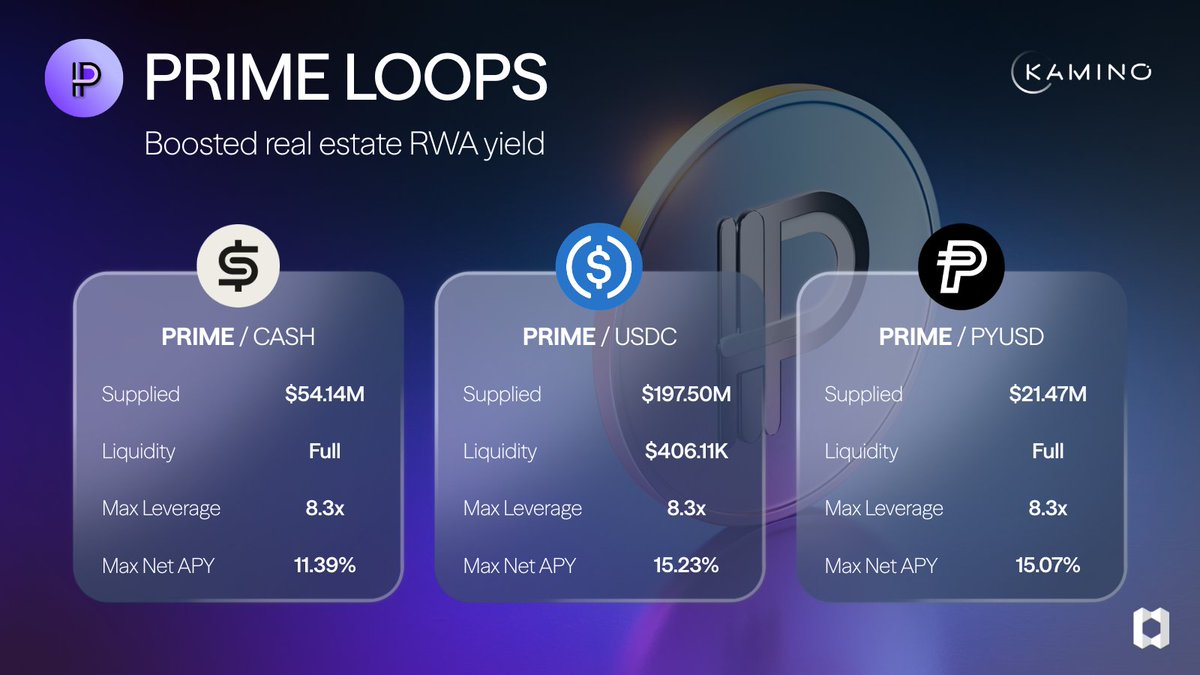

A direct response to user feedback!

Making RWAs easier to use one step at a time by eliminating high slippage USDG -> USDC swaps to mint ACRED.

Thanks to @Paxos @apolloglobal for making this possible with us at @Securitize.

Loopscale@Loopscale

English

Introducing the first Full-Stack Vibe Coding Platform powered by Claude Code.

Not only can you build a professional mobile app that accepts payments and ship it to the app store... As of today you can build a web app and deploy it to the internet with one click.

In celebration of 5000 vibe coded apps published to the app store, we're giving away a free month of vibe coding for those who reply to this post.

Reply and we'll DM you credits 👇

English

A follower in France has just sent me this - Revolut Globalhire (Revolut's Employer of Record service) looks like it's about to launch with a stand alone app. 🚀💻

Revolut is not just a bank.

Key Aspects of Revolut GlobalHire:

Employer of Record (EOR): Revolut will act as the legal employer for workers in other countries, handling payroll, benefits, and legal requirements.

Simplified International Hiring: The service aims to remove barriers like setting up local entities, making it easier for businesses to hire talent worldwide.

Built on Revolut People: It expands on Revolut's existing HR/performance management tools, integrating recruitment, performance, and payroll.

Focus on Compliance: GlobalHire will manage local tax laws and employment regulations across numerous markets.

English

@ownsomeshares @maxcashstacking If you’re smarter than 95% of the hedge fund community, then definitely quit and live off the income

English

@maxcashstacking I don't need to see a tweet to understand that 26.4% is totally unsustainable and basing your retirement plans off that would be financial suicide.

Be careful.

English

I’m 27 and based in London

My goal is to leave my 9-5 job by aged 30 and live off dividend income

Right now I’m generating ~£2,200/month from a ~£100k portfolio. The things I invest in are in the tweet below

It’s not perfect and I’m still learning but would you rather chase growth for 30 years working a job you hate or build income to escape the 9–5 sooner?

Wise Old Man - Dividend Investor £100k 🇬🇧@maxcashstacking

This is my current portfolio - circa £100k, netting roughly £2200 per month in income: $JEPQ £26,098 $FEPG £27,745 $MAGD £18,467 $YMAP £18,912 $TSLD £5186 $NVDD £1791 $COII £241 Built for income, not growth, however there is some growth Follow along to see the journey in 2026

English

@MENAUnleashed What % of china oil imports are from venezuela

English

Noticably, the US did not strike the oil producation facilities in Venezuela. It just bombed the port used to export it. Literally sticking it to China in the wide open.

English

@AndreasSteno Venezuelan oil makes up a pretty small amount of Chinese imports.. is it that important?

English

No, this makes it less likely that China takes Taiwan. This is about oil and Chinas access to Oil.

English

@GoingParabolic built in 2024, not 'under construction'

English

Under construction. Prototype. What do you think?

English

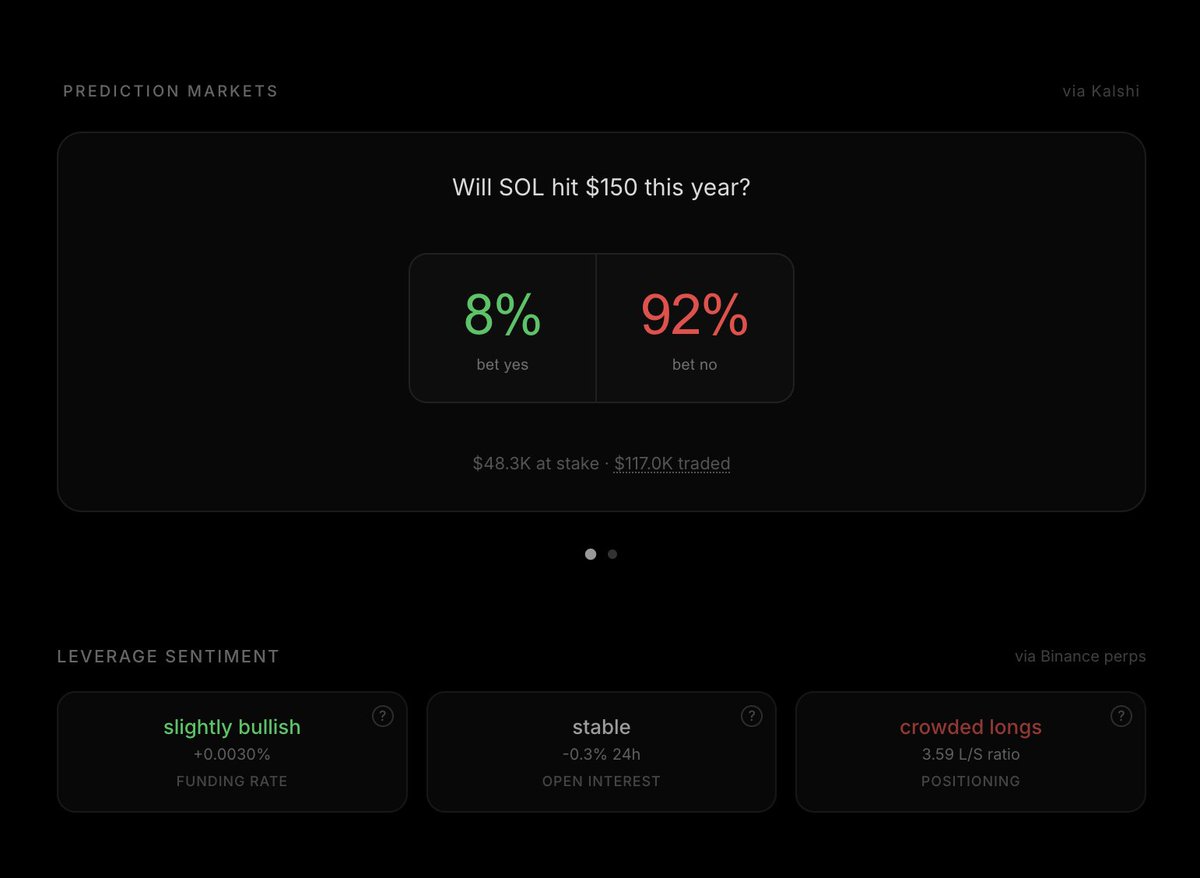

currently I'm surfacing funding rate, open interest and open interest % change, and long:short ratios

across binance, hyperliquid, bybit, and an aggregate of all exchanges

not perfect, but this combined with pred markets should give you a good idea on sentiment and positioning

English

@moothefarmer @solsticefi I know we want to be different and better than tradfi, but clear and concise disclaimers are what tradfi does well (regulators force them to). But it’s these standards which will encourage greater adoption.

English

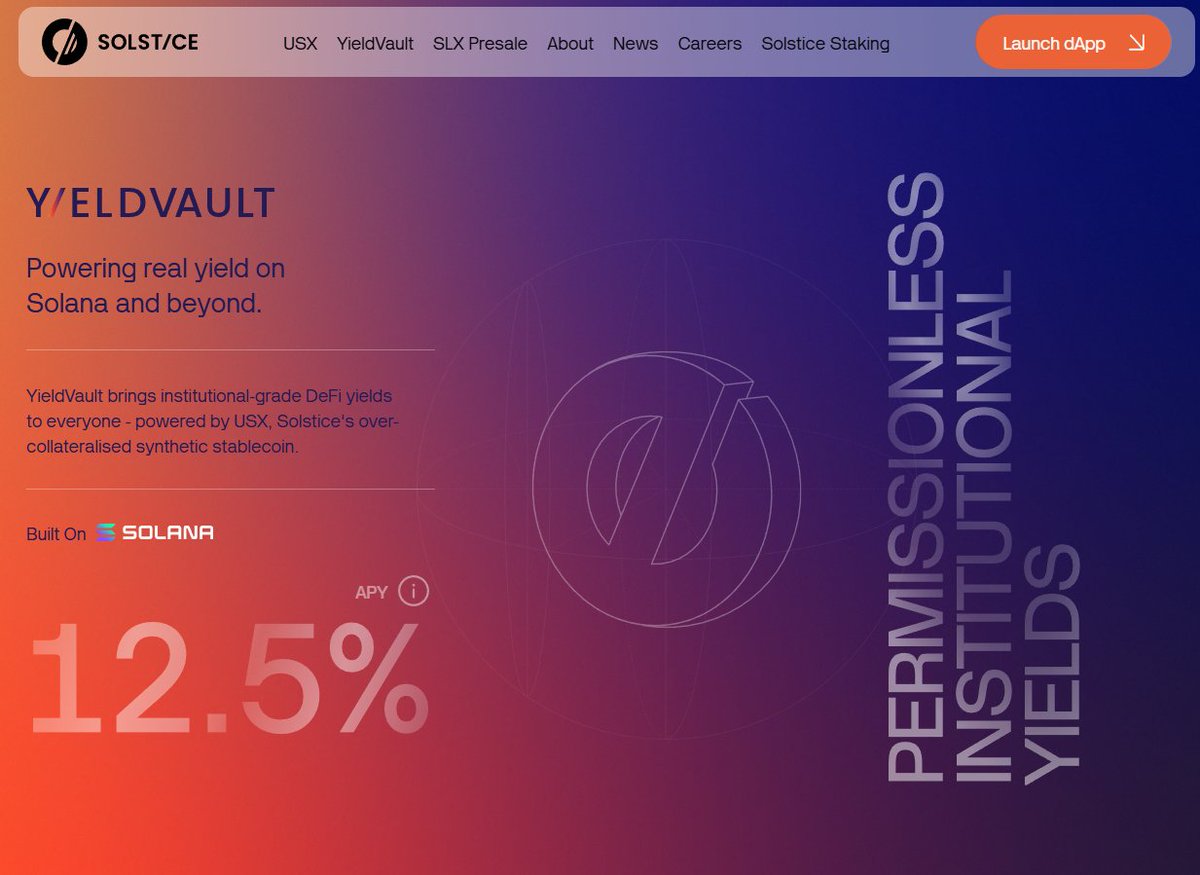

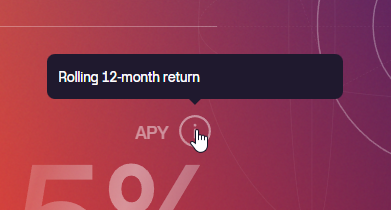

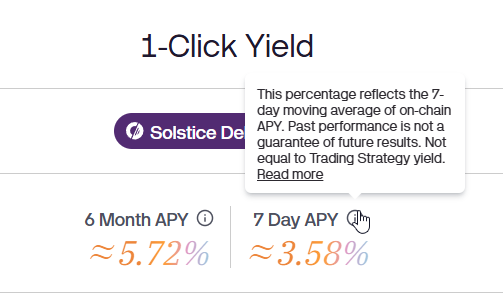

This sort of thing genuinely infuriates me, and it is exactly why DeFi still feels untrustworthy to so many people.

1) I visit the @solsticefi website to understand what all the noise is about.

2) Front and center, I am hit with a bold 12.5% APY.

3) Only after hovering do I discover this is actually a rolling 12-month return. Fine. I’ll suspend disbelief for a moment.

4) Then I open the dApp. Suddenly, reality sets in.

3.58% on a 7-day basis.

5.75% on a 6-month rolling basis.

Seriously?

Haters will argue that nothing here is technically wrong. From a legal standpoint, perhaps. But anyone with more than two brain cells know that splashing “12.5% APY” across a homepage is designed to bait users, not inform them.

There is absolutely nothing wrong with showcasing strong historical performance. But historicals belong on data pages, with context, timeframes, and proper breakdowns, not as headline marketing copy on a landing page.

If DeFi wants broader trust and adoption, this behaviour has to stop.

This is also precisely why platforms like @fundamental_fi matter. No marketing spin. No selective framing. Just clean, transparent data.

We can do better.

English