BFT_Edge

5.5K posts

BFT_Edge

@deepakdgy

Learner of Business/Financial/Technical Analysis, 1-3 strategies, Target: 25% CAGR (X to 10X in 10 yrs), Posts For Info, analysis can go wrong

Dubai Katılım Eylül 2011

46 Takip Edilen2.1K Takipçiler

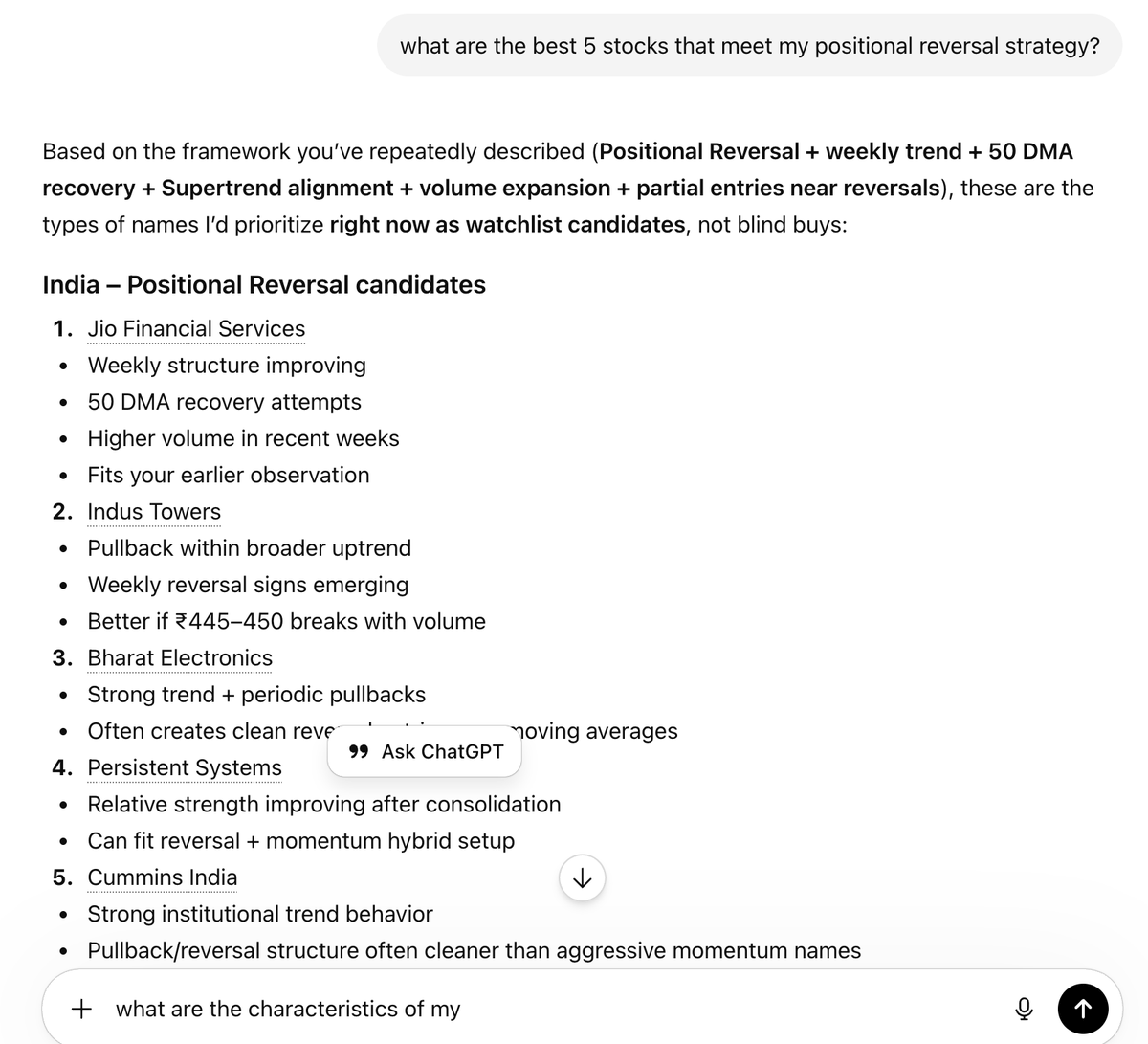

Today I just asked ChatGPT to name stocks based on my positional reversal strategy, but i had not given criteria of my strategy..

Somehow, it given the criteria at its own with list of probable stocks.

However i liked the remark which came at the end (highlighted in yellow).

AI very smart, its watching my PC, I guess.

English

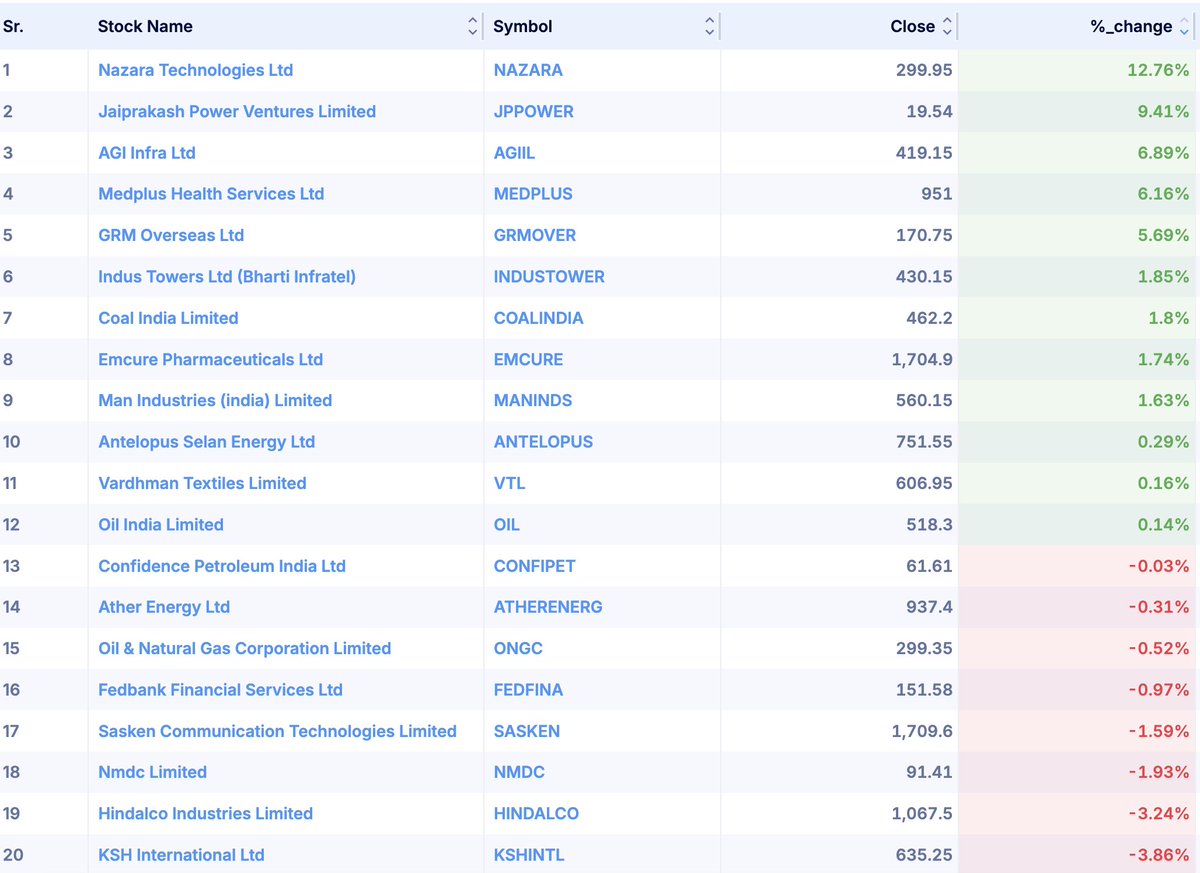

Momentum Screener

This simple screener can give stocks that are in momentum or in early stage of momentum

Use combination of 1/2/4 or 2/3/4

If run today, its giving list of 20 stocks.

then filter them with your own strategy for momentum criteria.

Below is my strategy link,

x.com/deepakdgy/stat…

channel link:

t.me/+8EHErYR8_c8zN…

English

If strategy alone determined trading success, more than 99% of traders would already be consistently profitable.

But reality says otherwise — the majority still struggle to make consistent returns.

So what’s missing?

Not another strategy.

It’s:

Stronger discipline

Better risk management, position sizing & stop losses

More patience to wait for quality setups

Consistency in following one proven process

Strategy is only one piece of the puzzle. Execution is what creates results.

English

RRKABEL at 1475

How is the stock, worth to buy?

It is meeting most of strategy criteria, check list below for observation:

1. Price was down by more than 50% from previous high - yes

2. Consolidation in last 1 year - yes, price moving in range for about 50 weeks

3. Super Trend indicator in green on weekly timeframe and price above trigger level - yes

4. higher volumes on up move, low volumes on down move - yes

5. weekly candle crossing 50 DMA - yes, indicating strength

6. Market support - yes, in upward move and if it remain strong in coming week.

7. Stop loss - 12% (swing low)

This is for educational purpose, not recommendation to buy / sell.

Refer below for strategy and back test.

x.com/deepakdgy/stat…

t.me/+ST3FrQWcCdwxZ…

English

@Akshat_World Tell us something which we don't know particularly if its coming as daily routine

English

Everyone is predicting that a "big stock" is coming. And, India needs to be prepared.

But, what exactly is this big shock? No one knows.

It can not be a few rupees of Petrol/Diesel hike. Or INR fall or FII withdrawals? That's been happening for a while.

It does not make much sense: why we would bring our economy to a standstill all of a sudden: work from home etc.

So what exactly are we missing?

My guess is we are lacking a direction. We don't know what areas to target vs not. We don't have a concrete plan to offer to investor/foreign players.

If we had, we would have already talked about this like we always do.

Another point is regarding ballooning debt, especially at state level. This creates panic because we can't fund freebies beyond a point (unless it gets offset by growth).

If people don't get freebies, it is a huge issue. Especially with rising costs due to energy shock.

Right now we are just simply waiting for global situation to improve. Till then, we simply conserve and survive. And, look for avenues to raise taxes further. This would let the freebie market survive for a while longer.

If we prepare people mentally--- the upcoming tax shocks become less brutal. And, these can be passed under the garb of "geopolitical issues".

English

@DenizTheTrader Here is my research on type of trading

I prefer positional swing trading for long term sustainability, less time, less stress,

x.com/deepakdgy/stat…

BFT_Edge@deepakdgy

What trading "TIMEFRAME" is suitable for you? Choose your trading / investing timeframe wisely, Mine is weekly timeframe as it is best suited for - Less time spent - Less screen time during market hours - Less stress, better emotional balance - Sustainable for life time - Scalable from few lakhs to 100s crore - High returns / lower drawdown What's your timeframe?

English

Swing Trading Is Easier Than Day Trading?

❝ YES ❞ or ❝ NO ❞

English

I think you meant term policy.

Endowments are money backk policies and are not low premium. They are worst.

BFT_Edge@deepakdgy

@Samudra3683 @Akshat_World Life insurance policies are most misselling products in India ..ULIP is the worst .. for life insurance, better to buy endowment policy with very low premium and invest otherwise for growth like in multicap and small cap funds, partly in US related funds.

English

AMD (at 449 on 15th May) stock had extra-ordinary move on up side

See weekly chart,

whenever a stock (any stock or commodity) go out of Faytterro Band, on lower side or higher side, it has tendency to reverse.

AMD is about 50% out of FB,

potential for some correction?

English

@Akshat_World Should we care about INR if we are earning, spending, saving in INR only, not spending in USD?

See below

x.com/deepakdgy/stat…

BFT_Edge@deepakdgy

With current INR depreciation, there is always a question, If someone’s earning, saving, and spending are entirely in INR, then USD/INR depreciation may not feel important immediately but it still affects them indirectly in many ways. Here’s why If: salary is in INR savings are in INR expenses are local INR expenses then: day-to-day life may not change immediately just because USD rises. You are not directly converting currency daily. But INR depreciation still affects indirectly 1. Imported inflation India imports: crude oil, electronics, machinery semiconductors When INR weakens: imports become expensive Result: fuel prices rise transport costs rise inflation rises Even local vegetables eventually get impacted through logistics. 2. Foreign travel & education become expensive US education Europe travel imported products all become costlier. 3. Asset prices may rise Currency depreciation often pushes: gold higher imported goods higher luxury products higher 4. Purchasing power erosion Suppose: salary increases 5% inflation due to weak INR = 7% Real purchasing power falls. 5. Global asset gap widens If INR weakens over long periods: global assets outperform in INR terms US stocks, gold etc. appear stronger Example: Even if S&P gives same returns in USD, Indian investor gains extra from INR depreciation. Currency fluctuations are NOT the biggest issue. More important are: income growth savings rate asset allocation inflation-adjusted returns Conclusion.. INR depreciation may not hurt immediately if your life is fully INR-based… but over time it silently affects inflation, purchasing power, and cost of living. That’s why better to diversify to protect long-term purchasing power, in equities gold global stocks (index atleast)

English

As INR hits 96, this is a good time to re-read this thread that I wrote 16 months ago.

And, explained why you should move to global assets.

And, prepare for an INR fall.

Akshat Shrivastava@Akshat_World

Are Indians getting richer or poorer? Is our economy headed in the right direction? On one hand: India is set to become the 4th largest Economy by GDP this year beating Japan.

English

@Samudra3683 @Akshat_World Life insurance policies are most misselling products in India ..ULIP is the worst ..

for life insurance, better to buy endowment policy with very low premium and invest otherwise for growth like in multicap and small cap funds, partly in US related funds.

English

An average NRI has a per capita income 7-8 times that of an average Indian.

India's #1 strength is its hard working, intelligent labour force. Especially NRIs.

They move countries & build a life from scratch in a foreign land. Dealing through numerous challenges along the way.

They are naturally inclined to invest in India.

Give them a sensible reason.

Don't give talks on high GDP growth, stop buying gold, stop using Petrol, stop traveling.

If this is an economic plan, then we better shut down a few ministries and save a few 100 crores.

On the one hand we ask them to fill 7 forms to withdraw their own money. On the other, we want their deposits by pushing nationalism.

See the problem?

Understand that we are dealing with decently educated savvy folks, who can see through the crap. Don't treat them like brain-washed fools.

Build a sensible plan, money will follow.

English

Over the last 14-15 months, I've beaten the Nifty 50 by over 95%, and the learning behind this has genuinely been one of the most valuable things I've picked up as an investor.

It all comes down to asset allocation and sector allocation - and while the idea sounds very simple, it is still incredibly effective when actually applied.

I've realised over the years that it is far more important to spend your time focusing on what assets and sectors will do well next than to focus on individual securities.

The main reason my alpha has been this high in the Indian markets over the last 1.5 years is because I could sense that earnings were slowing down and that the markets could become rangebound after being in a bull run since 2021.

At the same time, gold, silver, and copper were all looking very promising based on their fundamentals.

This was exactly when I made the decision to rotate my capital into commodities. I did this by executing multiple swing trades on gold, silver and copper as they kept rising.

Had I kept my equity positions instead, I would have not made more than 15-20% over the last two years, since Nifty has been flat for most of this time.

Over the last few weeks, I am splitting my capital across both Indian markets and commodities, given that our indices are down due to the war.

So if there is one thing worth taking away from this, it is to figure out where the money is flowing next and let that decide your allocation. Everything else is secondary.

Hope this helps you guys as much as it helped me when I finally figured out how important this was to generating portfolio alpha.

English

@RijhwaniSheetal this is what various styles of trading can do

FnO need high degree of decision making and risk management.

x.com/deepakdgy/stat…

BFT_Edge@deepakdgy

What trading "TIMEFRAME" is suitable for you? Choose your trading / investing timeframe wisely, Mine is weekly timeframe as it is best suited for - Less time spent - Less screen time during market hours - Less stress, better emotional balance - Sustainable for life time - Scalable from few lakhs to 100s crore - High returns / lower drawdown What's your timeframe?

English

One of my friends asked me about F&O trading and I told him the reality..it’s very tough. You have to give it a lot of time, build setups, follow rules, stay disciplined and it takes time to become profitable.

Cut to today…

He sent me a screenshot of profits in Sensex options. He bought calls at 70 and booked around 300 (1 lot).

Then he said - You were saying trading is very difficult. I just followed basic technicals and made this...thinking of increasing quantity from tomorrow.

I said - That’s great. All the best.

English

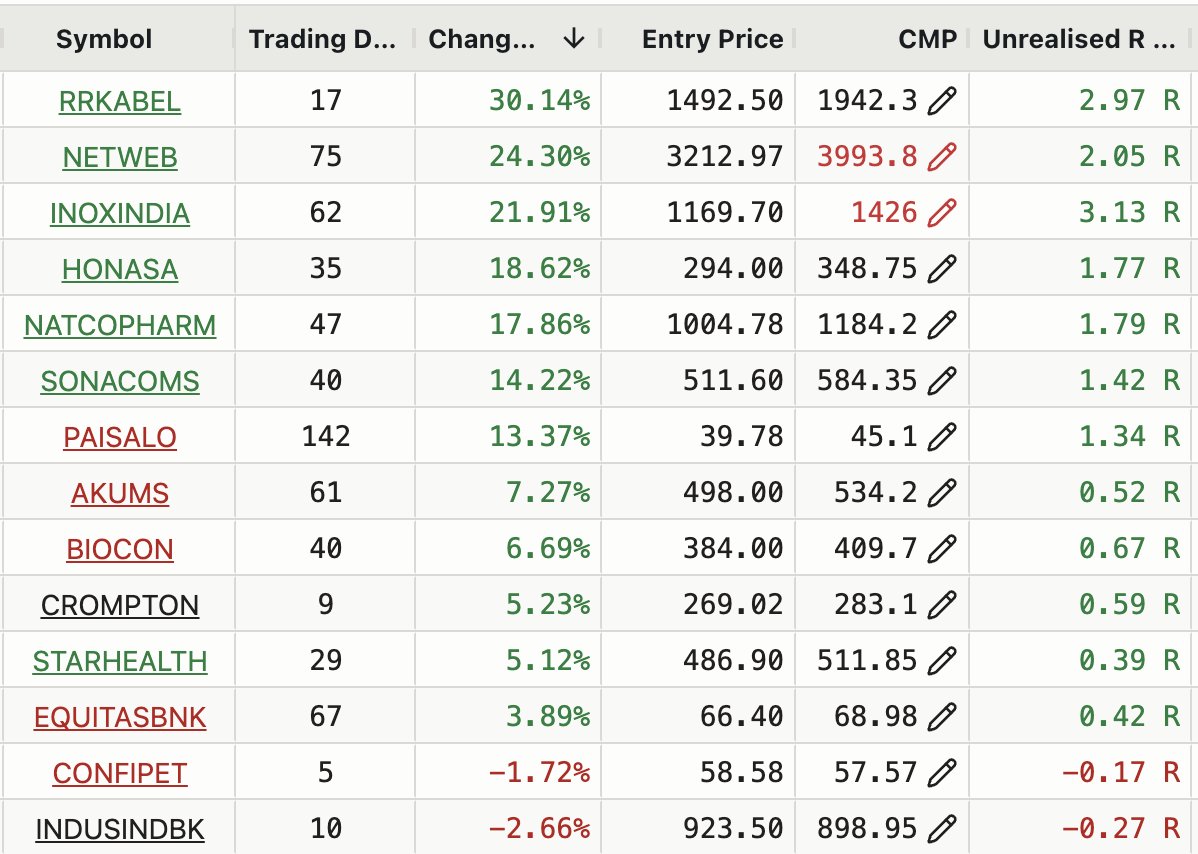

All the engines doesn't fire up at same time,

INOXINDIA, NETWEB, HONASA, already made up to 30-35% up and now correcting, coming back to mean reversion (50 DMA),

Other stocks RRKABEL, NATCOPHARM, BIOCON, CROMPTON are taking lead.

Rule based investing and process is important.

Positional Reversal Trades

This is not buy/sell recommendation, just for understanding the concept.

x.com/deepakdgy/stat…

English

With current INR depreciation,

there is always a question, If someone’s earning, saving, and spending are entirely in INR, then USD/INR depreciation may not feel important immediately

but it still affects them indirectly in many ways.

Here’s why

If:

salary is in INR

savings are in INR

expenses are local INR expenses

then:

day-to-day life may not change immediately just because USD rises.

You are not directly converting currency daily.

But INR depreciation still affects indirectly

1. Imported inflation

India imports: crude oil, electronics, machinery

semiconductors

When INR weakens:

imports become expensive

Result:

fuel prices rise

transport costs rise

inflation rises

Even local vegetables eventually get impacted through logistics.

2. Foreign travel & education become expensive

US education

Europe travel

imported products

all become costlier.

3. Asset prices may rise

Currency depreciation often pushes:

gold higher

imported goods higher

luxury products higher

4. Purchasing power erosion

Suppose:

salary increases 5%

inflation due to weak INR = 7%

Real purchasing power falls.

5. Global asset gap widens

If INR weakens over long periods:

global assets outperform in INR terms

US stocks, gold etc. appear stronger

Example:

Even if S&P gives same returns in USD,

Indian investor gains extra from INR depreciation.

Currency fluctuations are NOT the biggest issue.

More important are:

income growth

savings rate

asset allocation

inflation-adjusted returns

Conclusion..

INR depreciation may not hurt immediately if your life is fully INR-based…

but over time it silently affects inflation, purchasing power, and cost of living.

That’s why better to diversify to protect long-term purchasing power, in

equities

gold

global stocks (index atleast)

English

UAE Residents of Indian Origin Can Save Tax on Indian Mutual Funds, ETFs & BEEs

Understanding DTAA & TRC Benefits

Many UAE-based Indian investors are still unaware that they may legally optimise taxation on investments in India through the DTAA (Double Taxation Avoidance Agreement) between India and the UAE.

One of the most important requirements for claiming this benefit is the TRC (Tax Residency Certificate).

What is DTAA?

DTAA is an agreement between two countries to avoid double taxation on the same income.

For UAE residents:

✔ UAE has 0% personal income tax

✔ Under India-UAE DTAA, capital gains on certain Mutual Funds, ETFs and BEEs may become tax-efficient or tax-free, subject to eligibility and structure

✔ Dividend tax may reduce from 20% to 10% under DTAA provisions

What is TRC (Tax Residency Certificate)?

TRC is an official certificate issued by UAE authorities confirming that you are a UAE tax resident.

This certificate is important for claiming DTAA benefits in India.

Without TRC:

Investors may continue paying normal Indian tax rates

Typical tax rates in India without DTAA benefit:

• LTCG: 12.5% + surcharge = 15%

• STCG: 20% + surcharge = 25%

Benefits for UAE-based NRIs

With valid UAE residency and TRC, eligible investors may get:

✔ Tax-efficient or exempt capital gains on Mutual Funds / ETFs / BEEs

✔ Reduced dividend taxation under DTAA

✔ Additional advantage in ETFs/BEEs due to lower transaction costs and negligible brokerage/STT impact

Important Points

✔ Maintain valid UAE residency status

✔ Obtain updated TRC every year

✔ Ensure NRI status is correctly updated with banks/brokers

✔ Consult a qualified CA or tax advisor for applicability based on your investments

Common Mistake

Many UAE investors:

• Invest through NRE/NRO accounts

• But never apply for TRC or claim DTAA benefits

As a result, they may end up paying higher taxes than legally required.

(For educational purposes only. Please consult a qualified tax professional before taking any decision.)

English

Most traders search for a “holy grail” strategy, but profitable trading can actually be very simple on paper:

📊 Average Reward : Risk (ARR) = 2:1

📊 Win Rate = 50%

📊 Risk Per Trade = 1% of account

📊 Total Trades per Year = 120

Even with only a 50% win rate, this can potentially generate around 60% annual returns.

Sounds simple, right?

But the real challenge is maintaining the 2:1 Reward-to-Risk consistently.

Most traders fail because:

❌ They book profits too early

❌ They hold losing trades too long

As a result:

Reward becomes smaller than Risk (ARR below 1)

And once that happens, the math no longer works in your favour.

Successful trading is not about winning every trade.

It is about:

✔ Cutting losses quickly

✔ Letting winners run

✔ Maintaining discipline consistently

English

@RebellioMarket Can’t say without volumes trend

x.com/deepakdgy/stat…

BFT_Edge@deepakdgy

Many traders search for a “holy grail” strategy, but profitable trading can actually be very simple on paper: 📊 Average Reward : Risk (ARR) = 2:1 📊 Win Rate = 50% 📊 Risk Per Trade = 1% of account 📊 Total Trades per Year = 120 Even with only a 50% win rate, this can potentially generate around 60% annual returns. Sounds simple, right? But the real challenge is maintaining the 2:1 Reward-to-Risk consistently. Most traders fail because: ❌ They book profits too early ❌ They hold losing trades too long As a result: Reward becomes smaller than Risk (ARR below 1) And once that happens, the math no longer works in your favour. Successful trading is not about winning every trade. It is about: ✔ Cutting losses quickly ✔ Letting winners run ✔ Maintaining discipline consistently

English

@InvestorOfJAMMU Hmm

It’s possible with a strategy, risk management, discipline, consistency

x.com/deepakdgy/stat…

BFT_Edge@deepakdgy

Many traders search for a “holy grail” strategy, but profitable trading can actually be very simple on paper: 📊 Average Reward : Risk (ARR) = 2:1 📊 Win Rate = 50% 📊 Risk Per Trade = 1% of account 📊 Total Trades per Year = 120 Even with only a 50% win rate, this can potentially generate around 60% annual returns. Sounds simple, right? But the real challenge is maintaining the 2:1 Reward-to-Risk consistently. Most traders fail because: ❌ They book profits too early ❌ They hold losing trades too long As a result: Reward becomes smaller than Risk (ARR below 1) And once that happens, the math no longer works in your favour. Successful trading is not about winning every trade. It is about: ✔ Cutting losses quickly ✔ Letting winners run ✔ Maintaining discipline consistently

English

Impossible to make money in Stock Market with this combination.

English