de lavan

67 posts

🔴 Iran requires the transfer of highly enriched uranium to China - Senior sources to Al-Arabiya

x.com/AlArabiya_Brk/…

العربية عاجل@AlArabiya_Brk

مصادر رفيعة للعربية: إيران تشترط نقل اليورانيوم عالي التخصيب إلى الصين #العربية_عاجل

English

TRUMP: NEVER A DEADLINE FOR IRAN, THE DEAL WILL HAPPEN BUT NOT SET A DEADLINE

English

IRAN DEAL CLOSE: WAR PAUSE & NUCLEAR TALKS

The White House is nearing a one-page MOU with Iran to halt fighting and start nuclear talks. Iran is expected to respond within 48 hours; no deal is final.

Core terms:

Iran: Pause enrichment, no nukes, accept UN inspections, curb underground sites.

U.S.: Ease sanctions, release frozen assets.

Both: Loosen Strait of Hormuz restrictions.

The plan would trigger a 30-day negotiation window (likely Geneva or Islamabad). Trump has paused escalation; officials caution talks remain uncertain.

English

de lavan retweetledi

Gas prices in the US have moved up to $4.30 per gallon, their highest level since July 2022. The 44% spike over the last 9 weeks ($2.98/gallon to $4.30/gallon) is the biggest we've seen in the past 30 years.

English

de lavan retweetledi

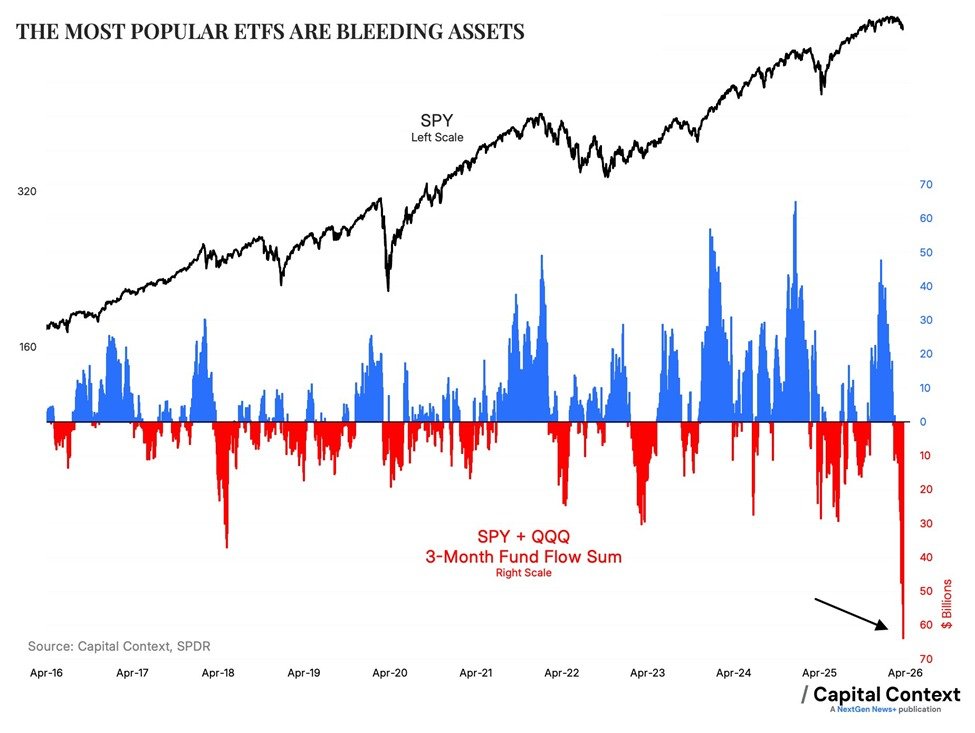

BREAKING: The S&P 500 ETF, $SPY, and the Nasdaq 100 ETF, $QQQ, have seen combined outflows of -$64 billion over the last 3 months, the most on record.

This marks a sharp reversal from +$50 billion in 3-month inflows posted in November.

This is also almost DOUBLE the previous decade high set in 2018.

Not even the 2020 pandemic and the March-April 2025 sell-off saw such significant outflows.

As a % of assets under management, the 3-month outflow is up to -5%, the biggest since Q1 2023.

By comparison, the largest percentage outflow over the last decade was -8% in April 2018.

Investors are have rushed to the sidelines.

English

@quarktalksss 台灣那邊有說錯 自用房屋稅率全國3戶內1.2%僅1戶為1% 超過第4戶在2%以上 除非出租(成為公益出租人)稅率按自用算 所以有個問題 造成之前屯房的人頭戶很多

中文

@DrClownPhD Taiwan's baseball team. Fubonguardians cheerleading instagram.com/fubon_angels_o…

English

I don’t understand what’s happening… but where do I sign up? 😅

English

de lavan retweetledi

10 days in - Operation Epic Fury delivering RESOUNDING success.🦅

1. Destroy the Iranian regime's missiles

2. Annihilate their navy

3. Ensure terrorist proxies can no longer destabilize the world

4. Ensure Iran can NEVER obtain a nuclear weapon

AMERICAN DOMINANCE. 🇺🇸

English

IRAN'S REVOLUTIONARY GUARDS SAY THEY ARE READY TO FOLLOW NEW SUPREME LEADER MOJTABA -STATEMENT

English

de lavan retweetledi

This is insane to me.

Palantir just fell 30% and people are calling it cheap.

It's trading at 50 times REVENUES.

Not earnings. Revenues.

Let me tell you something:

Before the dot-com bubble burst, Cisco, Microsoft, and Amazon peaked at price-to-sales ratios between 30 and 50. Palantir blew past 100x at the top and people are calling a pullback to 50x a buying opportunity.

In what universe is 50 times revenues a bargain?

This one, apparently. Because an entire generation of investors has been conditioned to confuse price with value.

They're TWO DIFFERENT things.

Price is what you see on the screen. It tells you nothing about what you're actually buying.

A stock falling 30% doesn't make it cheap. It might still be wildly expensive.

And a stock going up doesn't make it a good investment. It might just mean someone is willing to pay more for trading sardines.

You know the story.

Big bidding war at the Tokyo fish market. Sardines keep changing hands at higher and higher prices.

Last guy opens the can, tastes one, spits it out. Wants his money back.

Seller looks at him like he's crazy.

"Those sardines aren't for eating. They're for trading."

That's what happened with a lot of this merchandise the last few years.

Palantir. ServiceNow, still trading at 60+ times earnings AFTER the selloff. The whole Mag 7 complex.

It all worked when liquidity was abundant and everyone was running the same playbook:

Buy the narrative. Ignore valuation. Let momentum do the work.

It worked the last 5 times. Then one day it doesn't.

I think that day is here. And I don't think this is a dip. I think it's a REGIME CHANGE.

Tech outperformed the market for over a decade. The US outperformed the rest of the world.

Large caps crushed everything. Much of it was justified. Relative price follows relative earnings. Credit where it's due.

But we went through a 40 year cycle of falling interest rates. And that's OVER.

The things most sensitive to liquidity, like high-multiple tech and Bitcoin, are struggling. The things sensitive to inflation and real growth are working.

Energy over tech. Commodities over crypto. Small cap value over mega cap growth.

They're all planets orbiting around the same sun.

The buy-the-dip crowd thinks this is just another pullback before regular scheduled programming resumes.

Palantir goes back to 125 times revenues. ServiceNow back to 20 times sales. The Mag 7 rips to new highs.

Maybe. But ask yourself this:

If the tide has actually turned, and you're still holding these names at these valuations, what's your margin of safety? Where's the floor?

There isn't one. Because when you pay 50 times revenues for a company, you're not investing. You're speculating that someone will pay 60x after you.

Meanwhile the Russell isn't the answer either...

40% of those companies don't make money. Small cap growth is still absurdly expensive.

The only segment that looks genuinely interesting is small cap value, and even there you have to do the work.

My playbook hasn't changed:

Own things where valuations make sense, earnings are growing, and the macro tailwind is at your back.

Energy. Commodities. Select small and mid-caps where the PE starts with a 1, not a 7.

The last shall be first. The first shall be last.

POSITION ACCORDINGLY

English

de lavan retweetledi

de lavan retweetledi

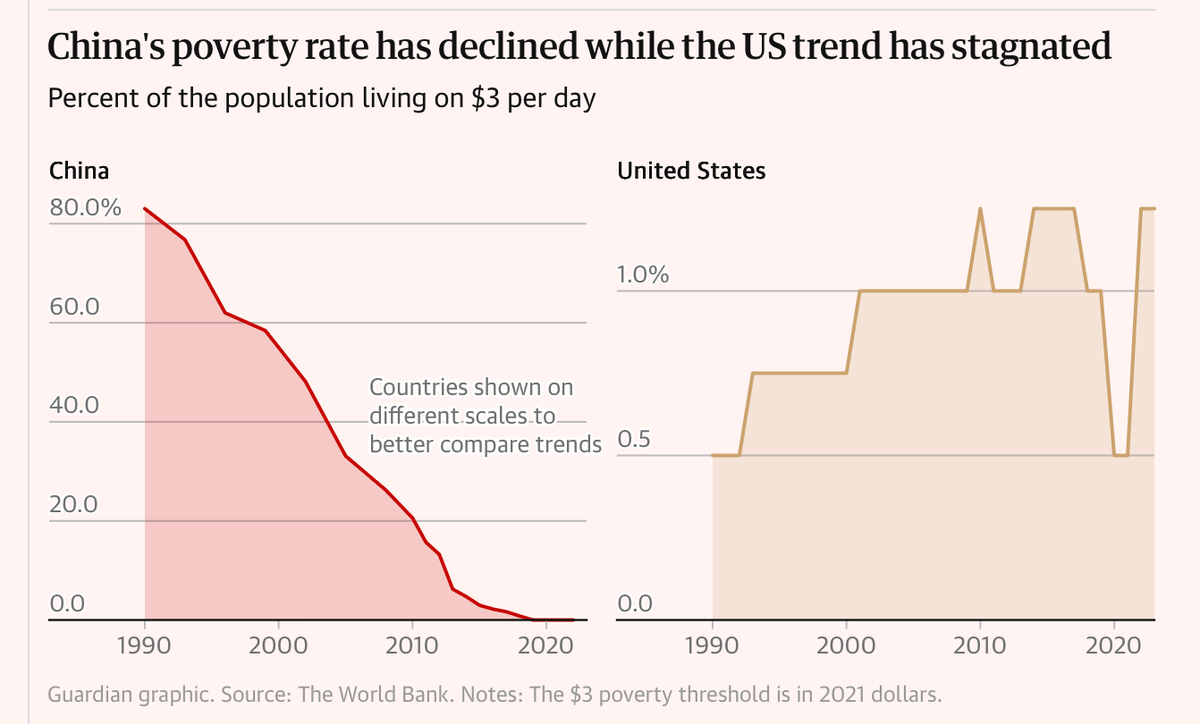

It's hard to imagine a more dishonest graph than this one by the Guardian claiming China is bringing people out of poverty while the US is not.

The US poverty rate has been so low for >30 years that it wouldn't even show up on the China graph if it had been plotted to scale!

English